With the state- and individual-level July employment data now in hand, we estimate the impact of the early expiration of enhanced federal unemployment insurance (UI) benefits in 25 states on employment, participation, and wages.

The state-level July payrolls figures do not show a statistically meaningful difference in job growth between states that ended UI benefits early and states that didn’t. But the more detailed individual-level data from the household survey of the employment report show clear evidence that benefit expiration increased the rate at which unemployed workers became employed.

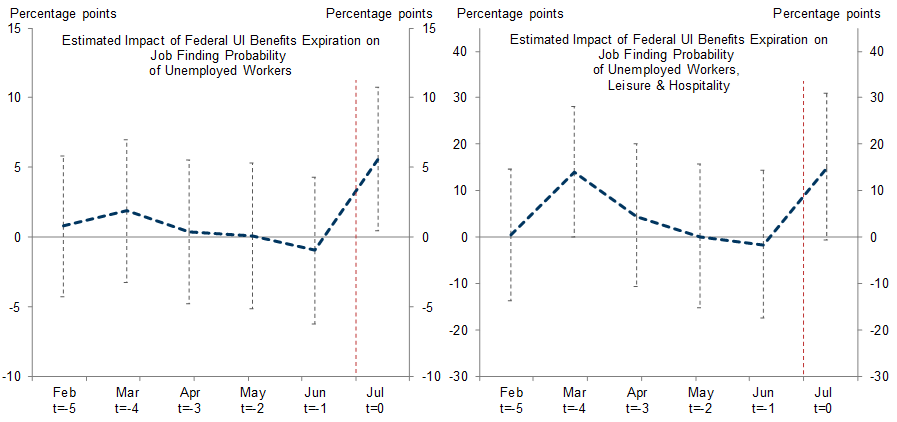

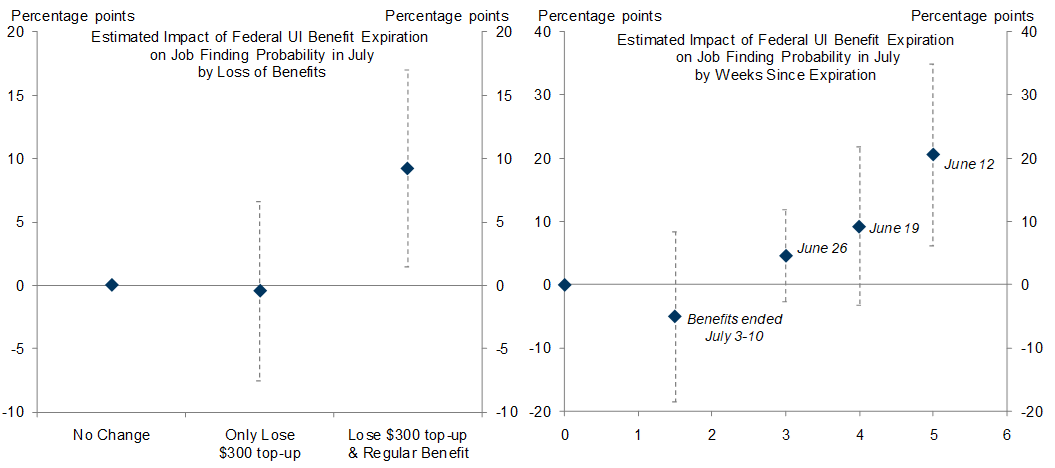

We make four key findings. First, UI benefit expiration increased unemployed workers’ job finding probability by 6pp (vs. an average job finding probability of 27%) in July. Second, the effect is larger for low-paid leisure and hospitality workers (+15pp). Third the effect is entirely driven by workers who lost all benefits (+9pp), while workers who just lost the $300 top-up were unaffected. Fourth, the effect increases over time and was only +5pp in states where benefits expired on June 26 but +21pp in states where benefits expired on June 12. New academic research supports our findings.

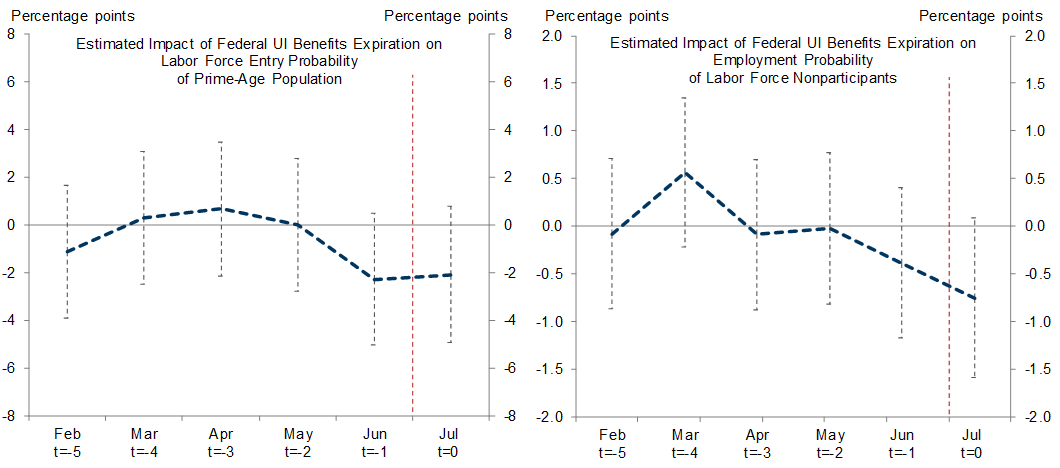

We find no evidence of a boost to labor force participation—in fact, the estimated effect is negative, but statistically insignificant. This suggests that many workers are staying out for non-financial reasons such as concern about Covid and may be slow to return to the labor force even after UI benefits end.

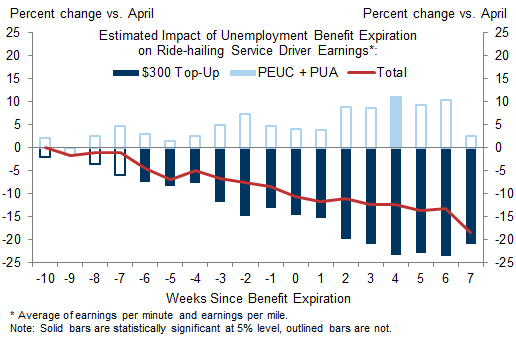

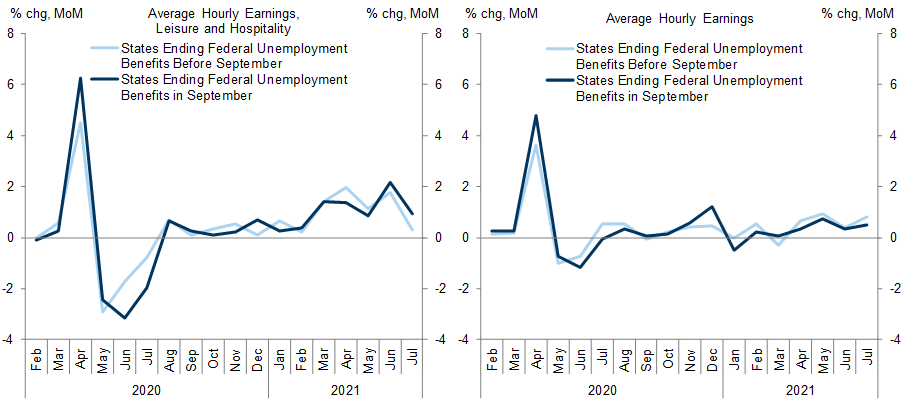

The impact of benefit expiration on wage growth remains inconclusive. We previously showed that wages for ride-hailing service drivers—where wages change dynamically in real time in response to increases in labor supply—have declined more in states that ended benefits early. Average hourly earnings growth in the leisure and hospitality sector was also softer in these states in July, although the difference is not statistically significant.

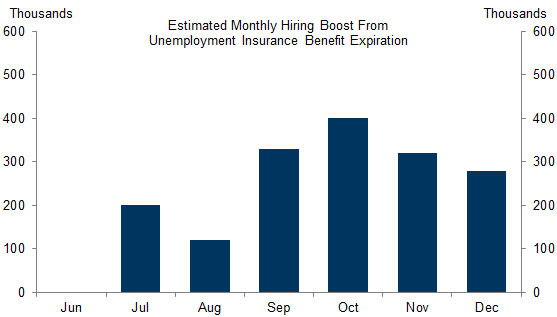

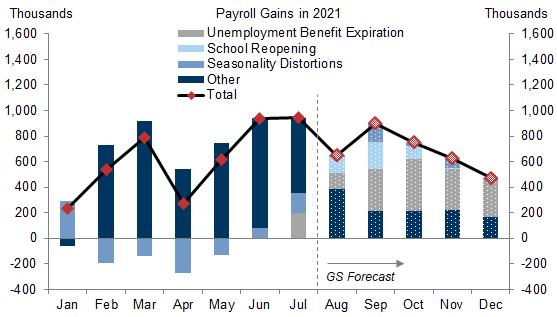

Our findings reinforce our confidence that national UI benefit expiration on September 6 will boost job growth by another 1.5mn through year-end. But they also suggest that it might take longer for the participation rate to recover. We continue to expect the unemployment rate to reach 4.1% by the end of 2021, but now expect the participation rate to only reach 62.2%.

Back to Work When Benefits End

Early Unemployment Benefit Expiration Increased the Incentive to Work

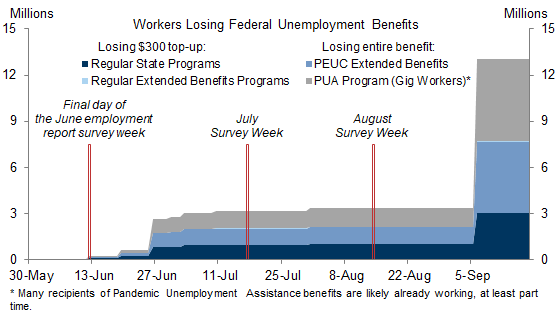

Exhibit 1: 3 Million Workers Lost Some or All Unemployment Benefits in June and July

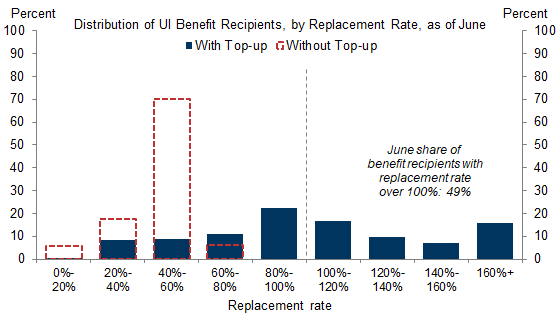

Exhibit 2: Half of Unemployment Benefit Recipients as of June Made More from Benefits Than from Their Former Wages, but None Will Without the $300 Top-Up

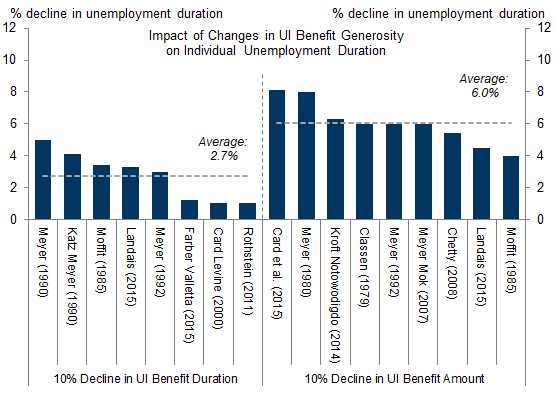

Exhibit 3: Academic Studies Suggest Generous Unemployment Insurance Benefits Are Usually a Meaningful Drag on Employment

The Employment Effects of UI Benefit Expiration

Exhibit 4: State-Level Data Do Not Show Any Impact of Early UI Benefit Expiration on Aggregate Employment

Exhibit 5: Unemployment Benefit Expiration Increased the Job Finding Rate of Unemployed Workers, Especially Leisure and Hospitality Workers

Exhibit 6: The Impact of Benefit Expiration on Job Finding Rates Is Larger for Workers Who Lost Their Entire Benefit and Grows Over Time

Exhibit 7: Early Unemployment Benefit Expiration Did Not Increase Labor Force Participation

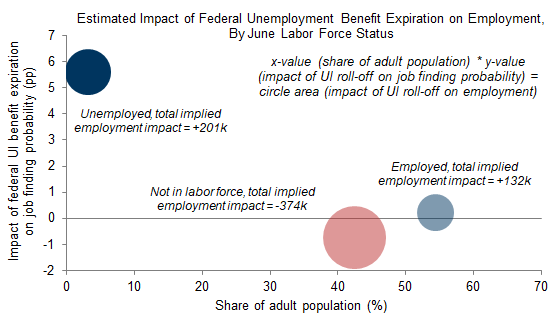

Exhibit 8: The Small, Statistically Insignificant Decline in the Job-Finding Rate of Nonparticipants Offset the Large Boost from Unemployed Workers Because Nonparticipants Are a Larger Share of the Population

The Effect of Benefit Expiration on Wage Growth

Exhibit 9: We Find a Large and Statistically Significant Decline in Ride-Share Driver Earnings in States Where Benefits Ended Early

Exhibit 10: Average Hourly Earnings for Leisure and Hospitality Workers Were Slightly Softer in States That Ended Benefits Early Than in States That Did Not

Updating Our Employment Forecast

Exhibit 11: We Expect UI Benefit Expiration to Boost Payrolls Gains by Another 1.5mn This Fall

Exhibit 12: We Expect Payroll Gains to Jump Again in September and Remain Strong Through Year-End

Joseph Briggs

Ronnie Walker

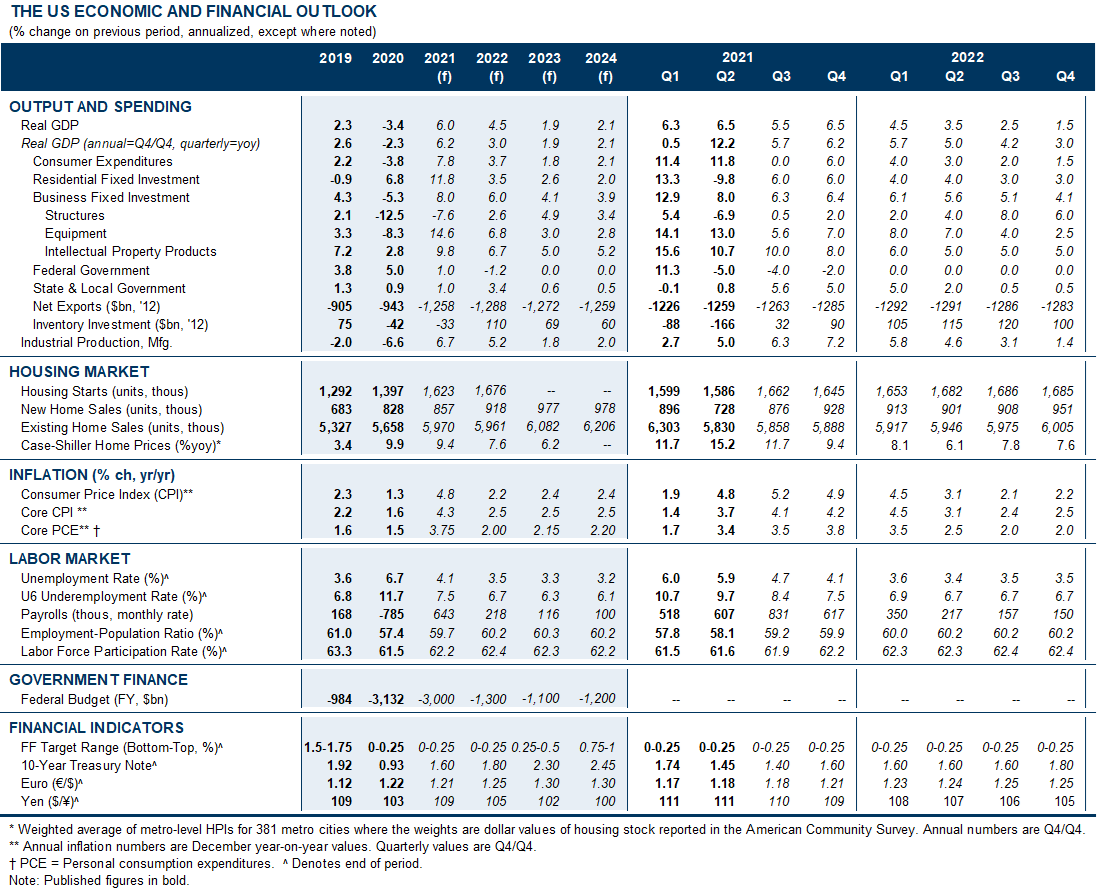

The US Economic and Financial Outlook

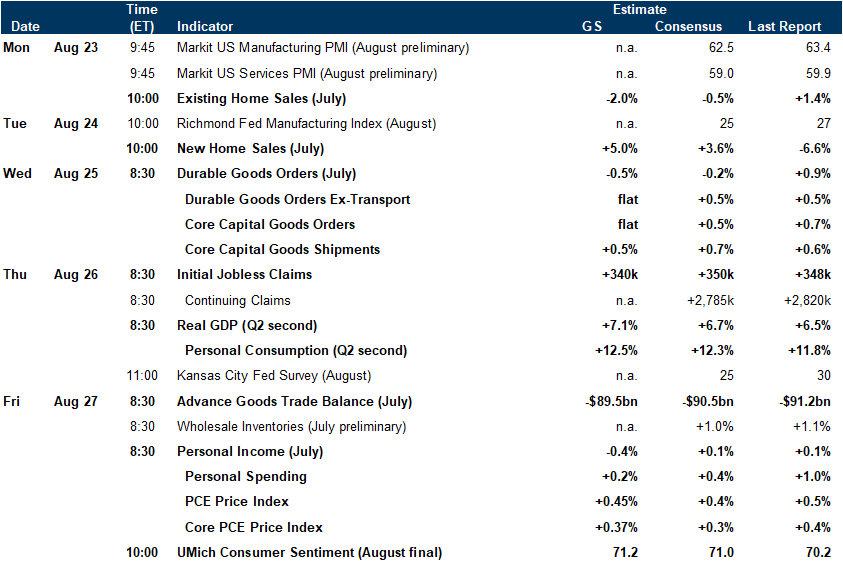

Economic Releases

- 1 ^ Kyle Coombs, Arindrajit Dube, Calvin Jahnke, Raymond Kluender, Suresh Naidu, and Michael Stepner, “Early Withdrawal of Pandemic Unemployment Insurance: Effects on Earnings, Employment and Consumption,” 2021.

Investors should consider this report as only a single factor in making their investment decision. For Reg AC certification and other important disclosures, see the Disclosure Appendix, or go to www.gs.com/research/hedge.html.