Global manufacturing supplier delays have intensified further to extreme levels, especially in the US and Europe. Supply chain issues have substantially contributed to the downgrades to our 2021Q2 and 2021Q3 US growth forecasts, and have led to major global upside inflation surprises. What lies behind these supply chain stresses and how will their evolution affect global growth and inflation?

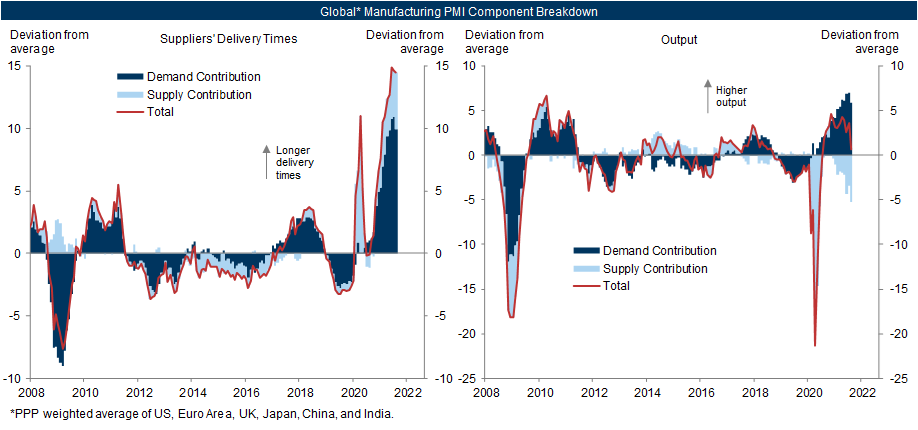

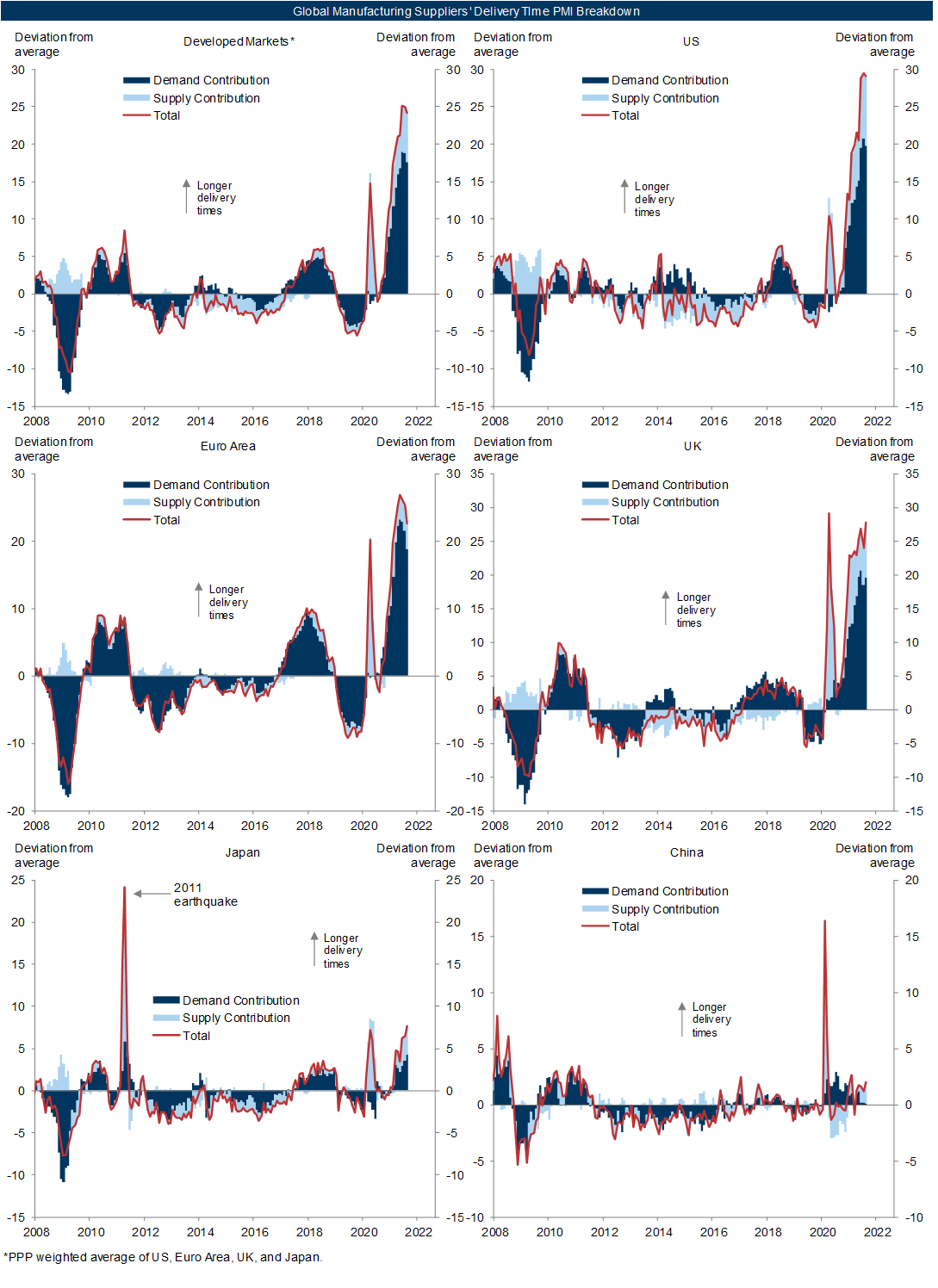

We estimate that strong goods demand currently accounts for about two-thirds of the global manufacturing delays. While weak supply led to delays and depressed output last spring, the global manufacturing PMI output index remains firm now, indicating an overwhelming role for the demand side. The exception is Asia, where weakness in supply, partly related to virus disruptions, plays a larger role.

A moderation in goods demand over the next year should sharply reduce manufacturing delays, although a decline in virus-related disruptions to global and especially Asian goods supply should help too. We expect goods demand to moderate as the global fiscal impulse turns negative, and as spending gradually rotates back from goods to services assuming the virus situation improves. That being said, structurally strong tech demand and the slow speed at which semiconductor production capacity can be increased suggest that the easing of shortages for chips (and therefore cars) will take longer than for other constrained goods.

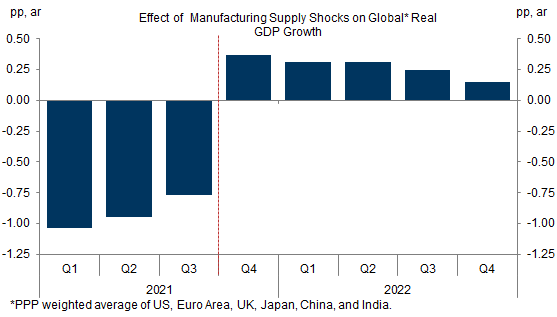

Assuming a gradual normalization in our GS effective lockdown index, we estimate a swing in the manufacturing supply impulse to global growth from roughly -1pp so far this year into slightly positive territory in coming quarters.

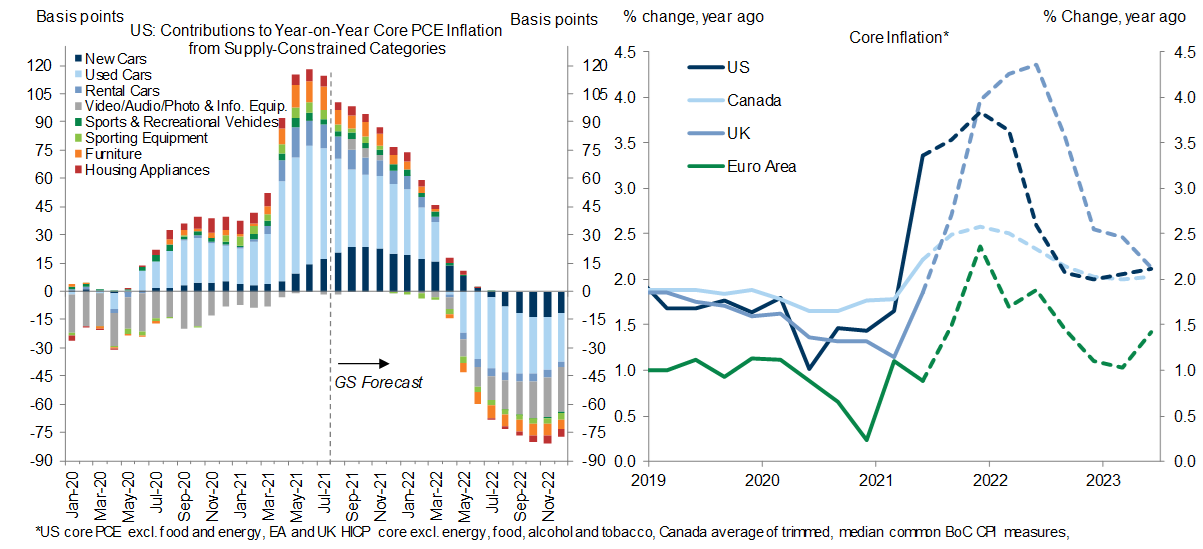

The expected moderation in global goods demand and the virus-driven improvement in goods supply help bring down inflation to more normal levels. We expect core inflation to fall back by 2022Q4 to 2.5% in the UK, 2.0% in the US and Canada, and 1.1% in the Euro Area.

Supply Chains, Global Growth, and Inflation[1]

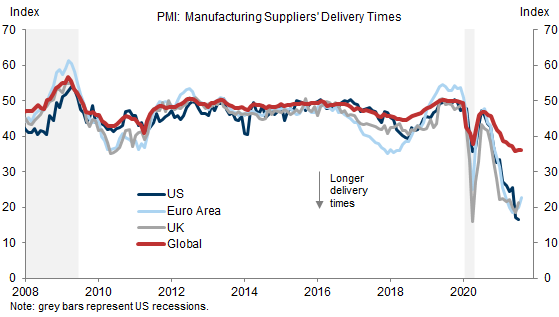

Exhibit 1: Manufacturing Supplier Delays Have Intensified Further

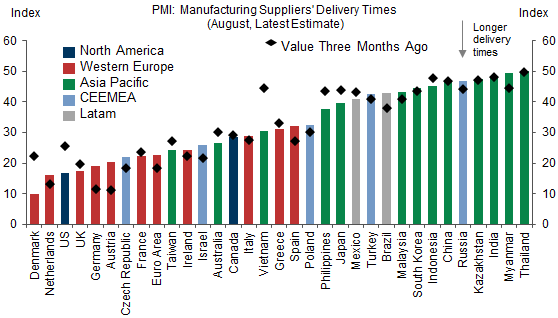

Exhibit 2: Delivery Delays Are Particularly Extreme in Europe and the US

It’s Mostly Demand

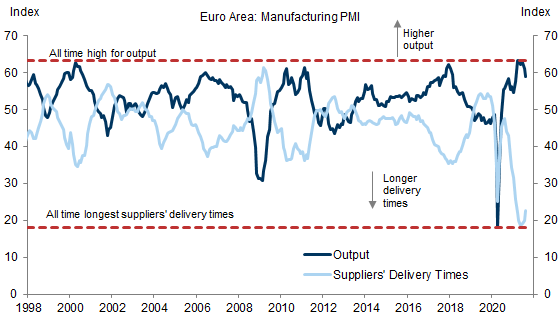

Exhibit 3: Elevated Manufacturing Output Suggests that Delays Are Mostly Caused by Strong Demand Rather than Weak Supply

Exhibit 4: We Estimate that Strong Demand Is Currently Driving About Two-Thirds of the Rise in Global Manufacturing Supplier Delays

Exhibit 5: The Delivery Delays Largely Reflect Strong Demand in Western DMs; Weak Supply Plays a Larger Role in Asia

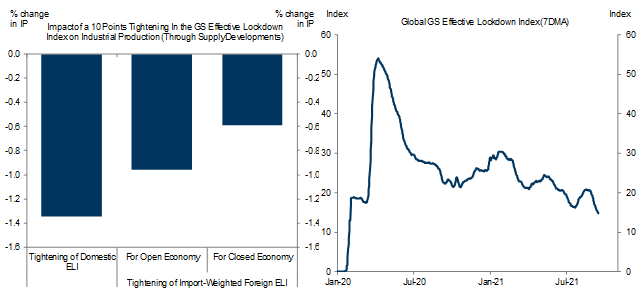

Less Virus, More Manufacturing Supply

Exhibit 6: The Expected Easing of Our ELI at Home or Among Trade Partners Should Boost IP Through Improvements to Goods Supply

Less Virus, Moderating Goods Demand

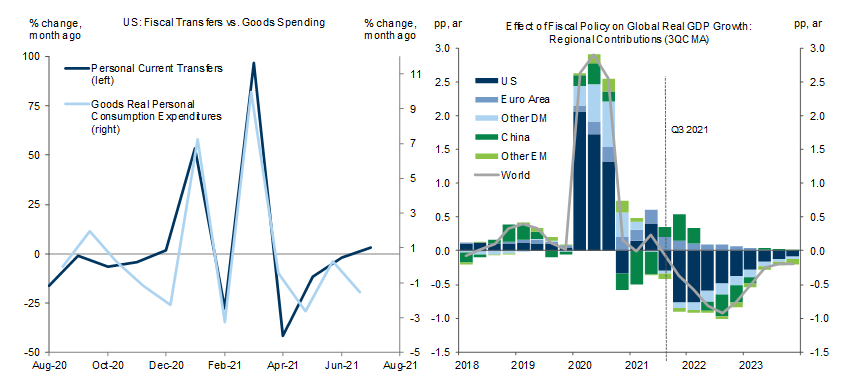

Factor 1: Global Fiscal Impulse Turns Negative

Exhibit 7: Fiscal Policy Has Contributed to Strong Goods Demand but Will Tighten

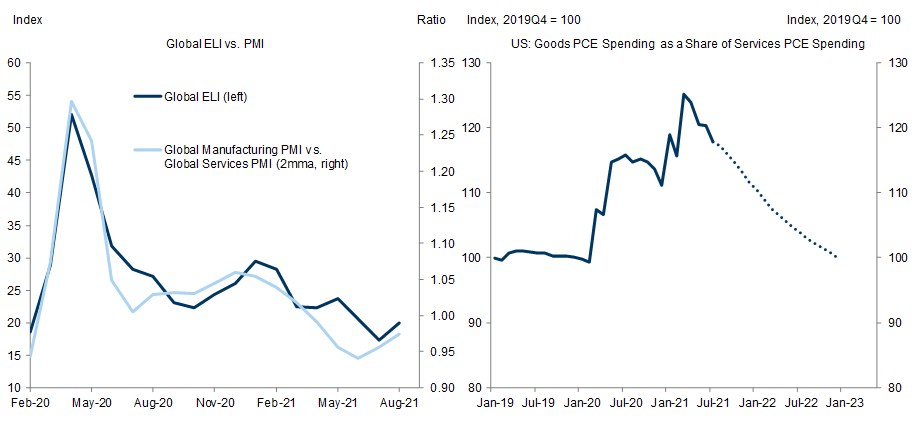

Factor 2: A Shift Back to Services

Exhibit 8: We Expect Spending to Gradually Rotate Back from Goods to Services as the Virus Fades

Caveat: A Semi-Persistent Tech Boom

Exhibit 9: The Pandemic Has Further Strengthened Demand for Taiwanese Semiconductors

Supply Shocks, Growth, and Inflation

Exhibit 10: Assuming Gradual Virus Improvements, We Expect a +1pp Swing in the Manufacturing Supply Impulse to Global Growth

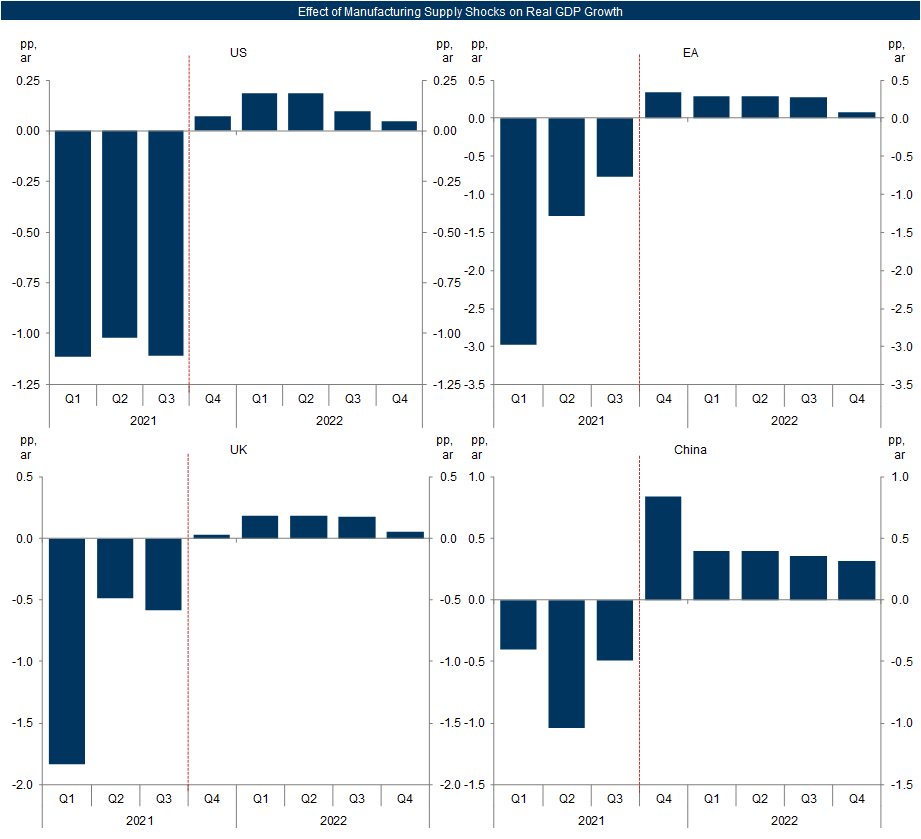

Exhibit 11: Assuming Gradual Virus Improvements, We Estimate a Rise in the Manufacturing Supply Impulse to Growth, Especially in the Manufacturing-Oriented Chinese Economy

Exhibit 12: A Sharp Drop in the Contribution From Supply-Constrained Categories to US Core PCE Inflation; We Expect Core Inflation to Moderate Across DMs in 2022H2

Sid Bhushan

Daan Struyven

- 1 ^ The authors would like to thank Nikola Dacic for his contributions.

- 2 ^ For instance, disappointing inventory formation, in turn largely reflecting supply chain issues, has contributed 2.0pp of the 3.9pp downgrade to our US 2021Q2 annualized GDP growth estimate since the last week of May.

- 3 ^ See Nikola Dacic, "The Cost of Supply Chain Disruption", European Daily, 12 March 2020.

- 4 ^ See Andrew Tilton, "Supply chain stresses", Asia in Focus, 15 September 2021.

- 5 ^ Specifically, we assume that countries in the high risk aversion group (see Exhibit 6 here) reach an ELI of 5 by the end of 2022Q4, countries in the middle risk aversion group reach an ELI of 3.75 by the end of 2022Q3, and countries in the low risk aversion group reach an ELI of 2.5 by the end of 2022Q2. We interpolate linearly between current ELI levels and the end point.

- 6 ^ The estimated improvement in the manufacturing supply impulse to Chinese growth reflects the assumed improvement in the global virus situation and does not capture the current stress in Chinese supply chains related to raw materials, driven by its more persistent decarbonization push.

Investors should consider this report as only a single factor in making their investment decision. For Reg AC certification and other important disclosures, see the Disclosure Appendix, or go to www.gs.com/research/hedge.html.