We continue to expect persistent pandemic-driven efficiency gains, for three reasons: 1) Strong cumulative productivity gains in 2020-21 in both official and alternative metrics, 2) The incidence of these gains within digitizing industries, particularly those where Work-from-Home is effective, and 3) The sheer scale of the changes to the workforce and to company business models since 2019.

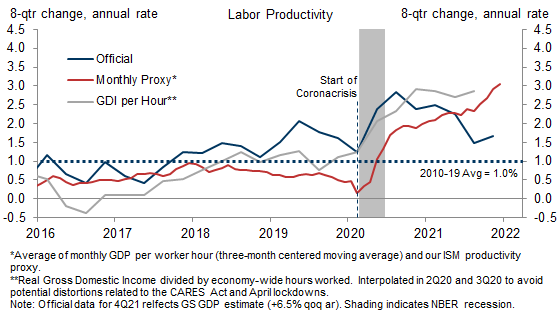

Productivity in the nonfarm business sector has increased at a 1.7% annualized pace over the last two years—compared to the +1.0% trend pre-pandemic. GDP data are often revised around recessions, and both our ISM productivity proxy and Gross Domestic Income per hour suggest an annualized pace closer to +3% over this period.

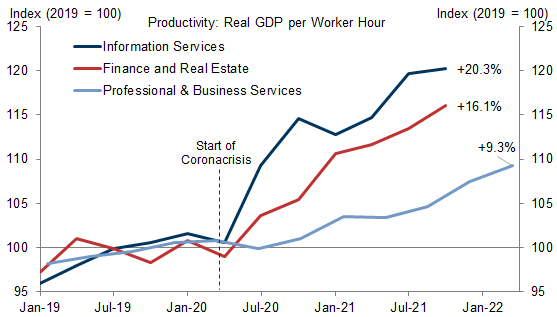

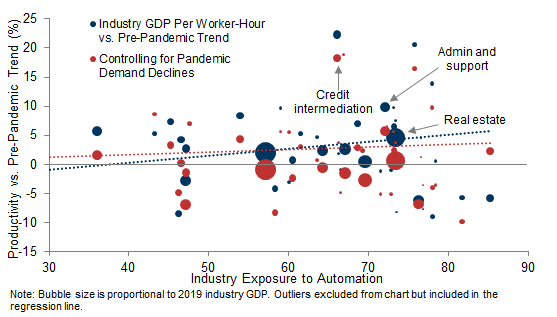

We also find that the incidence of productivity gains is skewed towards industries ripe for digitization, such as IT services (+11.9% annualized productivity growth since 4Q19) and professional services (+5.5%). Additionally, we find that Work-from-Home adoption and the scope for labor automation correlate positively with productivity acceleration across 54 subindustries—even after controlling for negative pandemic demand shocks.

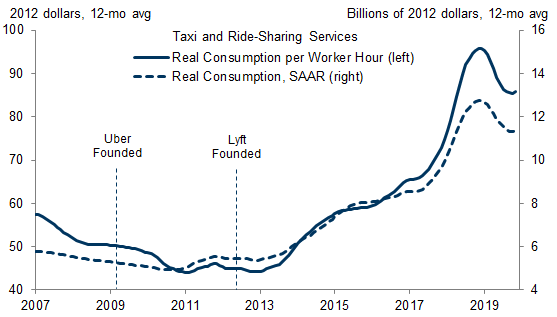

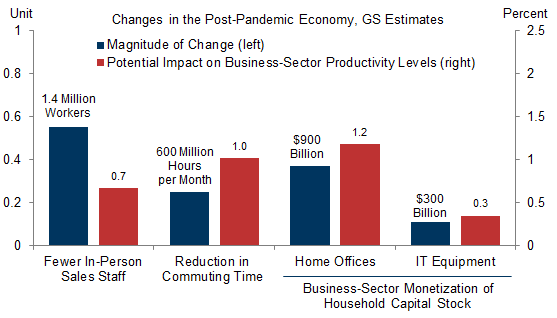

The sheer scale of pandemic-driven changes to the workforce and to company business models also argues for a large and long-lasting productivity inflection. These changes include 600 million fewer hours spent commuting every month, as well as possibly 1.4 million fewer cashiers, in-person salespeople, and office maintenance staff. Many of these workers and hours will be reallocated to more productive uses—especially at a time of labor shortages and near-record job vacancies. We also estimate around $900bn worth of home offices and $300bn of consumer IT equipment is now available for business-sector use. This echoes the output and productivity boom in the ride-sharing industry during the 2010s, when Uber and Lyft successfully monetized the household capital stock of cars.

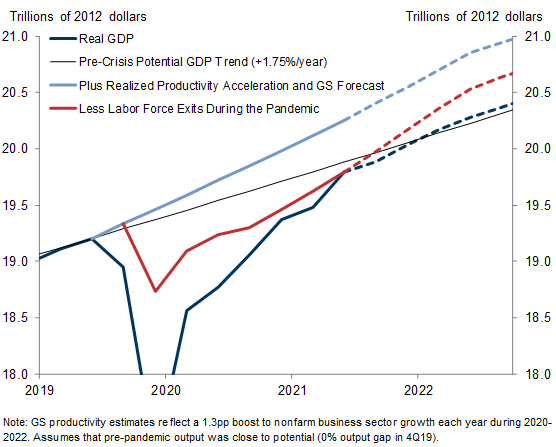

Incorporating these four baseline estimates into a top-down production function of the economy, we estimate a persistent boost to the level of private-sector productivity of 3-4% (or 1.0-1.3pp per year during 2020-22). We expect these efficiency gains to offset the decline in labor supply caused by the pandemic, in turn implying a longer runway for expansion. They also support our forecast of a more normal inflation environment in the medium-term once pandemic dislocations begin to recede.

Productivity Gains Will Outlast the Pandemic

Crisis-to-Date Productivity Trends

Exhibit 1: The Productivity Trend Has Accelerated by Around 1pp vs. Pre-Pandemic

Industry Composition of the Productivity Pickup

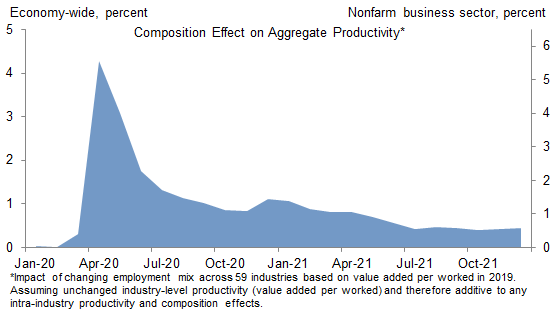

Exhibit 2: The Composition Boost from Fewer Hospitality and Retail Workers Has Mostly Unwound

Exhibit 3: The 2020 Productivity Surge in Non-Virus-Sensitive Services Continued During 2021

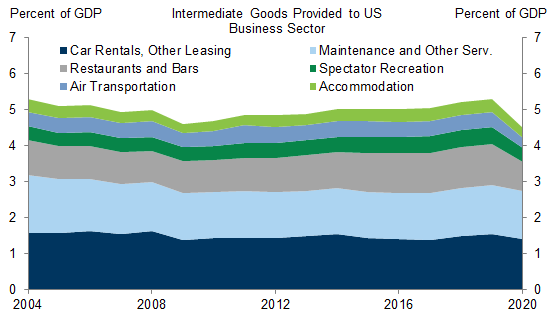

Exhibit 4: If Sustained, Reduced Business-to-Business Spending Productivity-Enhancing in the Medium Term

Exhibit 5: Productivity Gains Skewed Towards Industries Ripe for Digitization; Scope for Post-Pandemic Rebound in Virus-Sensitive Categories

The Post-Pandemic Workforce

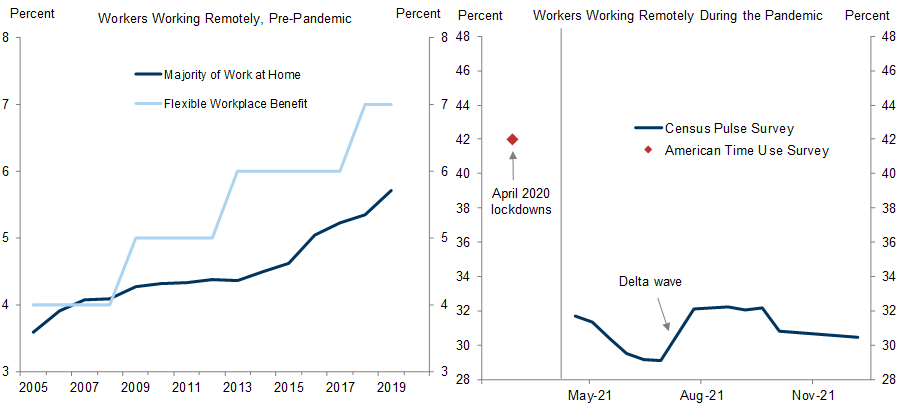

Exhibit 6: Employees Increasingly Worked from Home Prior to the Pandemic; Since Then, the Share of Remote Workers Surged During the Pandemic and Remains Elevated

Exhibit 7: Work-from-Home Associated with Accelerating Productivity Across Subindustries—Even After Controlling for Pandemic Demand Declines

Exhibit 8: Industries More Conducive to Automation Also Exhibit a Pickup in Productivity Growth, On Average

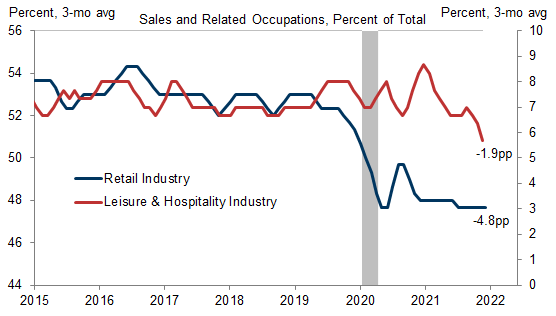

Exhibit 9: Digitization of the Consumer Experience Means Fewer In-Person Sales Staff After the Pandemic

Exhibit 10: Business-Sector Monetization of Household Automotive Capital Stock Boosted Output and Productivity in the 2010s—Presaging Similar Gains Today from Home Offices and Consumer IT Equipment

Room to Run

Exhibit 11: Scale of Pandemic-Driven Workforce Changes Argues for One-Time Productivity Gains of at Least 3%

Exhibit 12: Pandemic-Driven Productivity Gains Imply a Longer Runway for Expansion—and Less Inflation Pressure Once the Pandemic Ends

Spencer Hill

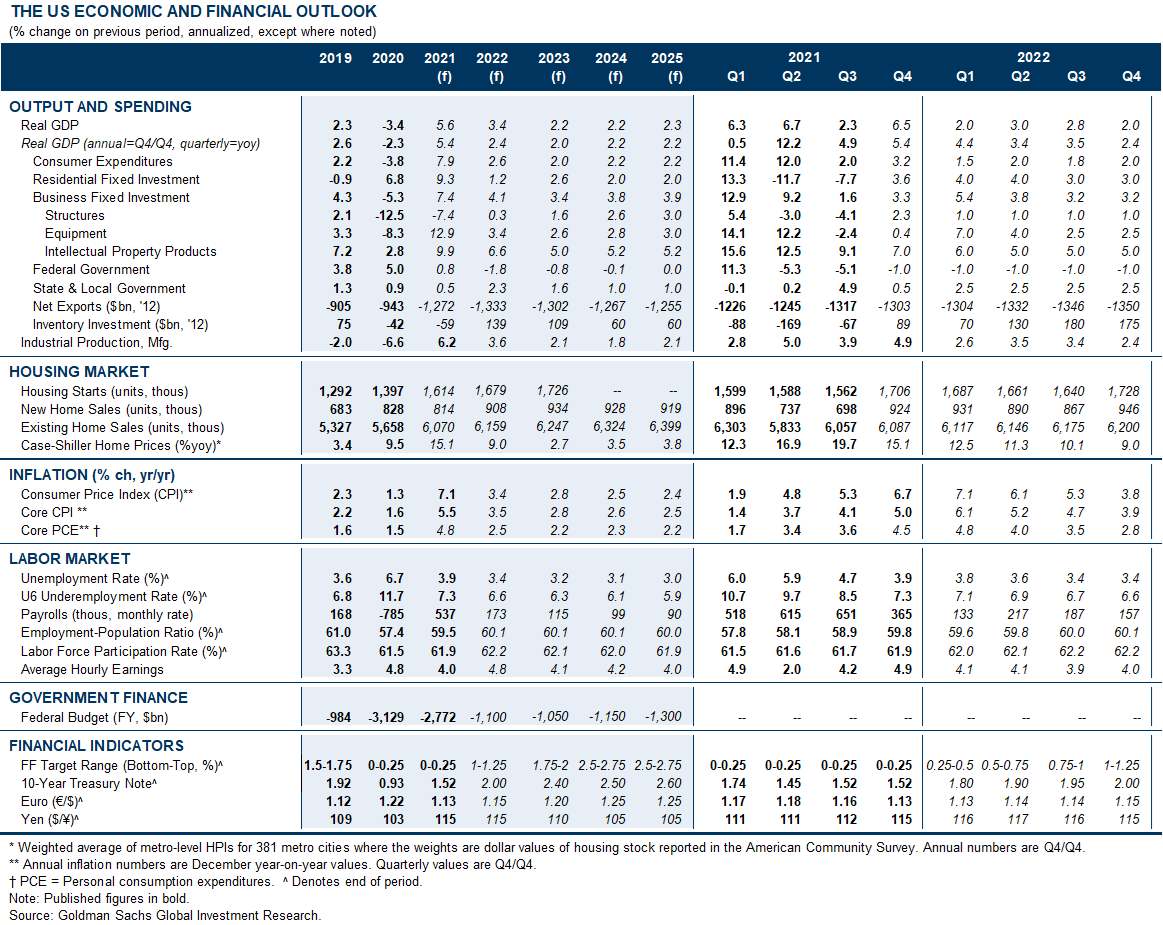

The US Economic and Financial Outlook

Economic Releases

- 1 ^ Commercial real estate is one key exception whose use as an intermediate input has not yet declined (as a share of GDP). To the extent that offices downsize or adopt shared workspaces after the pandemic, this offers a significant opportunity for additional productivity gains—specifically as the floor space is sold to other businesses or reallocated to residential or retail uses.

- 2 ^ Some of the transportation weakness may also be virus-related—reflecting weaker consumer demand or supply inefficiencies caused by the pandemic.

- 3 ^ Many of these workers and hours will be reallocated to more productive uses—especially at a time of labor shortages and near-record job vacancies.

- 4 ^ The net exit of unprofitable or inefficient businesses that occurs during and in the wake of recession.

Investors should consider this report as only a single factor in making their investment decision. For Reg AC certification and other important disclosures, see the Disclosure Appendix, or go to www.gs.com/research/hedge.html.