We wish our readers a happy and healthy new year. In our first Asia Economics Analyst of the year, we offer our answers to ten economic and market questions for the Asia-Pacific region and individual countries in 2023. We also review our questions and answers from one year ago.

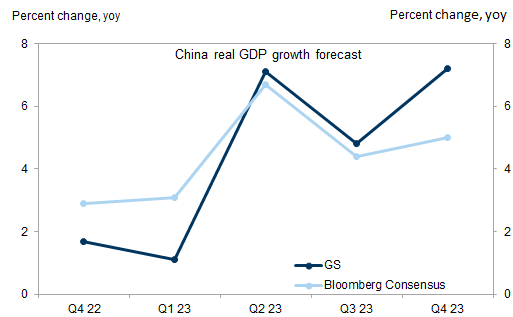

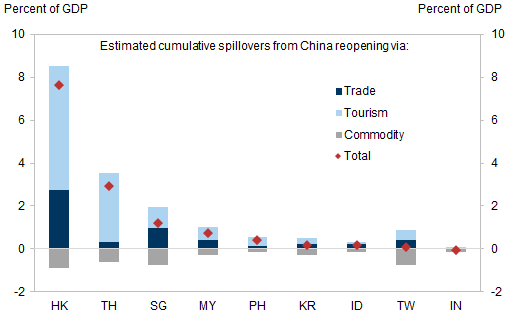

China's reopening should result in a burst of growth over the coming year (we estimate 7.2% GDP growth on a Q4/Q4 basis) and benefit regional economies, with Hong Kong and Thailand likely to see significant boosts from mainland tourists. While domestic inflation pressures are likely to increase, we do not think they will constrain the PBOC significantly this year.

Asia-Pacific manufacturing and trade should bottom out in early- to mid-2023; along with China's reopening this should help regional growth in the back half of the year.

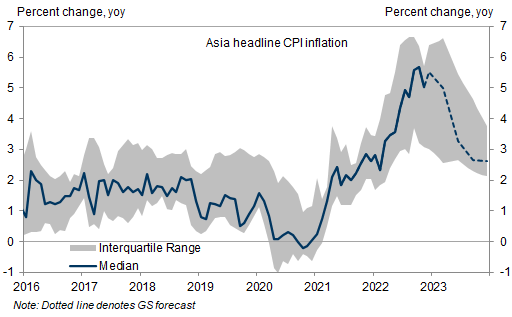

Inflation is peaking, in our view, though it will remain high in many economies (particularly smaller open economies) through mid-2023. Strong growth and resilient core inflation in India could push the central bank to tighten more than markets expect in H1. Very late in the year, with pressures having eased, we think the Bank of Korea could be among the first to cut rates. The Bank of Japan may tweak policy further, but we think yield curve control could stay in place this year.

With our global view of Fed hikes ending in H1 and the US narrowly avoiding recession, and regional growth improving later in the year, we think many regional currencies—including the CNY and JPY—could rally further against the USD.

While the majority of our 2022 answers worked out broadly as anticipated, we underestimated the inflationary pressure that would hit the region—exacerbated by Russia's invasion of Ukraine in late February—and the extent of the policy tightening that would result in some countries. We also were surprised by the extent of CNY weakness—reflecting an even worse economic outcome in China than our below-consensus view to start the year, as well as rapid USD appreciation on the back of the fastest pace of Fed hikes in decades.

Questions for 2023

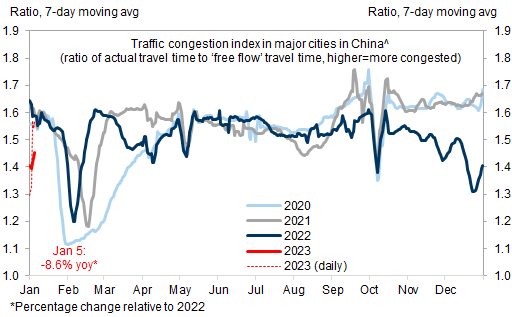

Exhibit 1: In China, mobility appears to be increasing again from low levels

Exhibit 2: Our 2023 China GDP forecast features a weak Q1 but a strong Q2-Q4 compared to market consensus

Exhibit 3: We estimate a significant potential boost should Chinese tourism return to pre-Covid levels

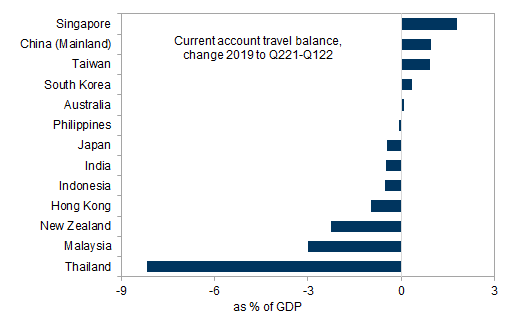

Exhibit 4: Thailand took the largest current account hit during the pandemic

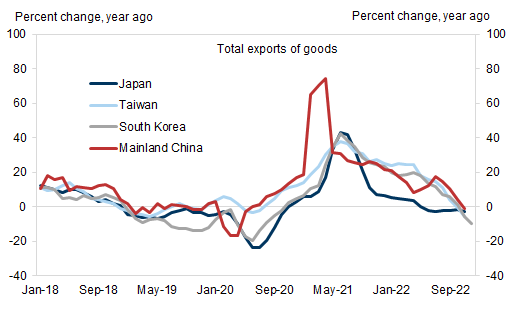

Exhibit 5: North Asia export growth has decelerated

Exhibit 6: Regional inflation appears to be peaking

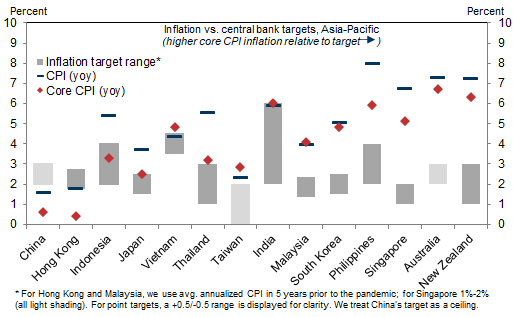

Exhibit 7: Underlying inflation remains above targets across the region (ex-China/HK)

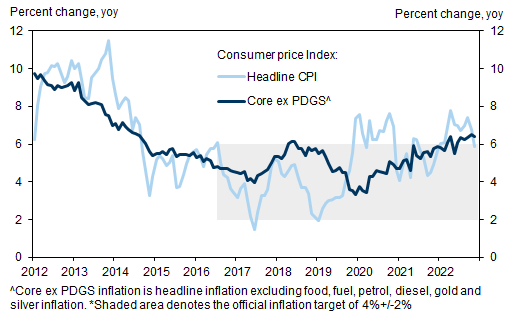

Exhibit 8: Underlying inflation continues to grind higher in India

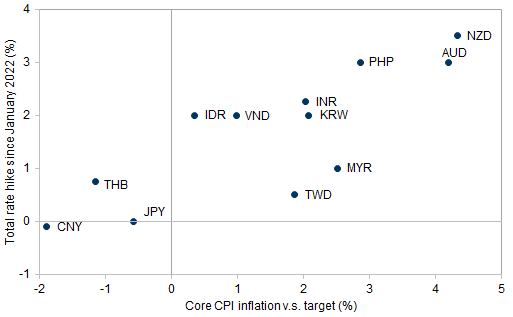

Exhibit 9: Rate hikes have been broadly correlated with inflation overshoots

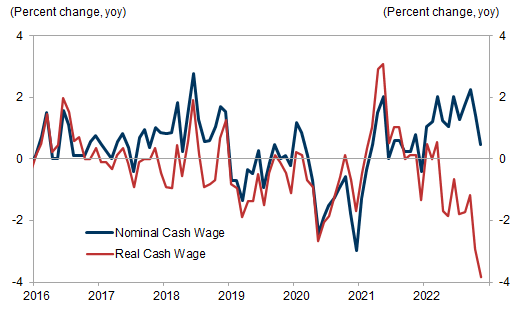

Exhibit 10: Real wage growth remains very weak in Japan

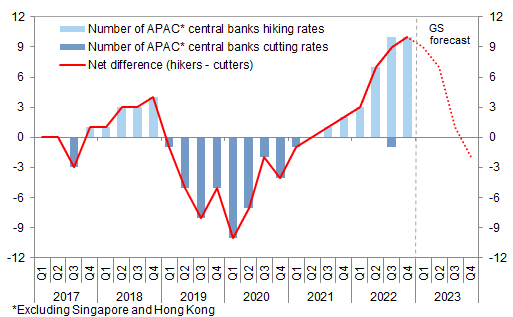

Exhibit 11: Very few APAC central banks are likely to cut in 2023

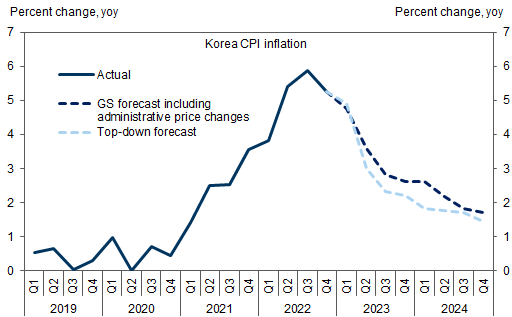

Exhibit 12: Korean inflation should fall significantly in 2023

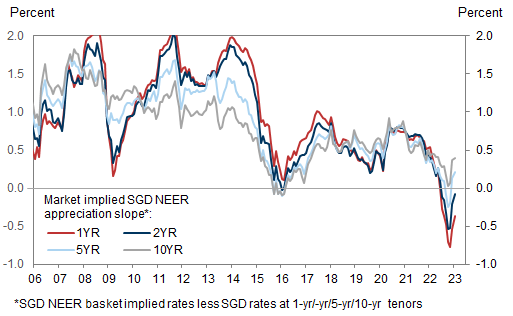

Exhibit 13: Singapore rates look mispriced

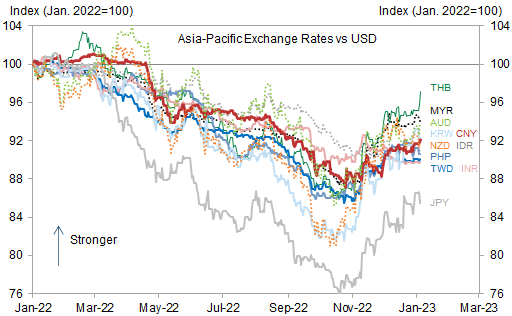

Exhibit 14: Regional currencies have rallied against the USD over the past two months

A brief recap of our questions and answers from 2022

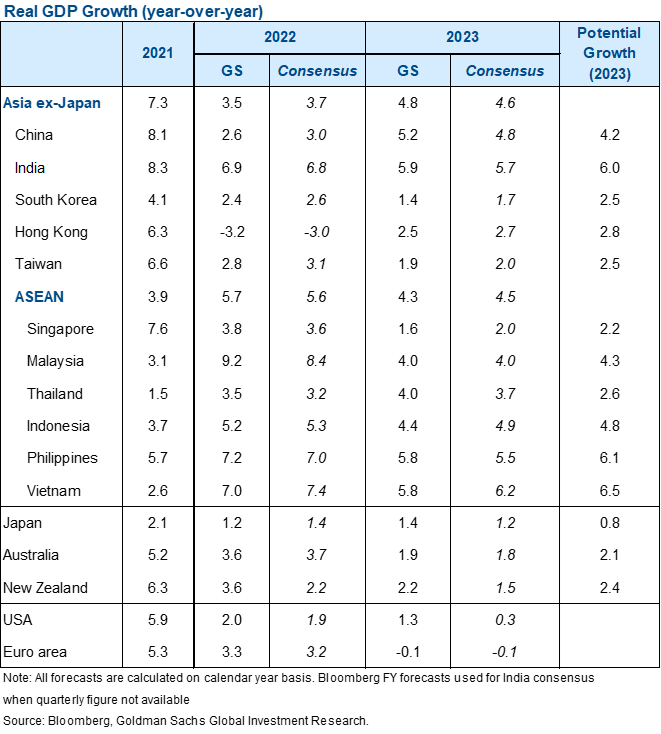

Exhibit 15: Our 2023 growth forecasts are above consensus in China, Japan, and the US

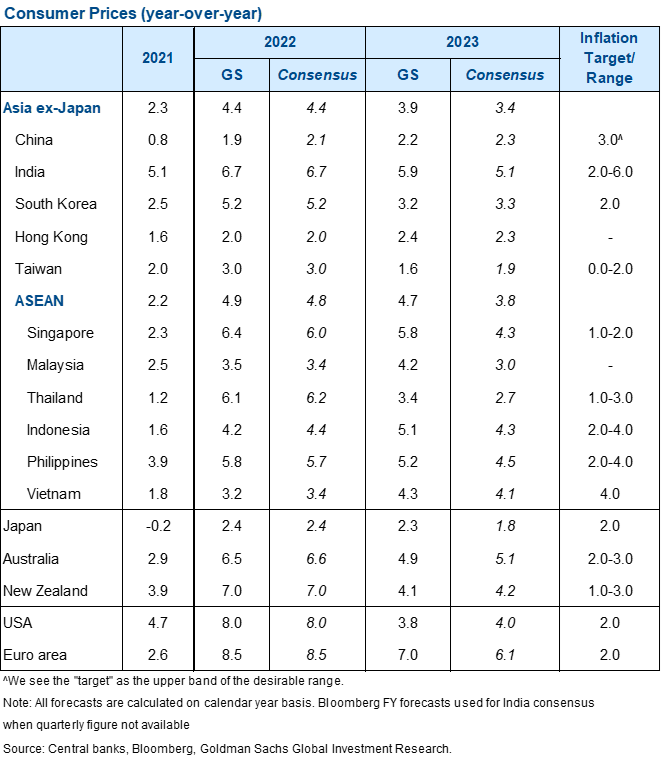

Exhibit 16: We expect CPI inflation to decline in 2023 but remain relatively high in many economies

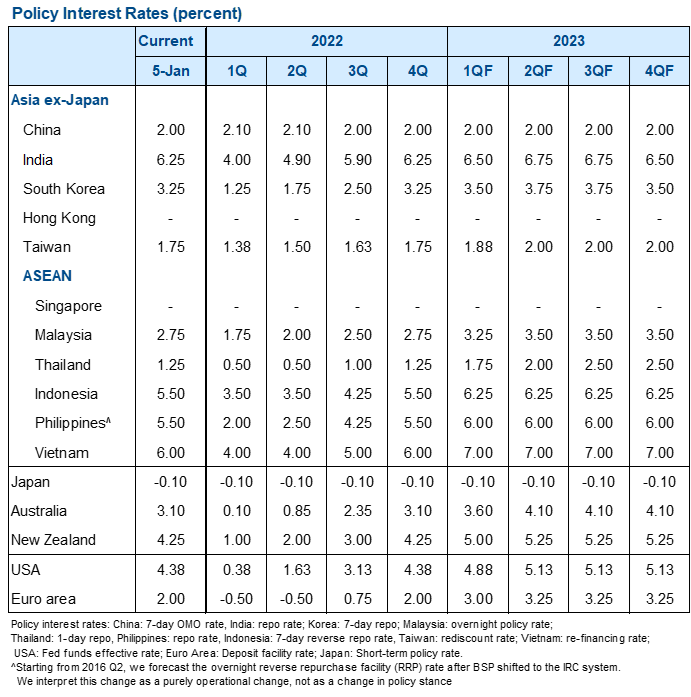

Exhibit 17: We expect most regional central banks to hike further in the first half of 2023

Investors should consider this report as only a single factor in making their investment decision. For Reg AC certification and other important disclosures, see the Disclosure Appendix, or go to www.gs.com/research/hedge.html.