- Intro

- 5 key points from the Goldman Sachs Hedge Fund Trend Monitor

- Performance, leverage, and short interest

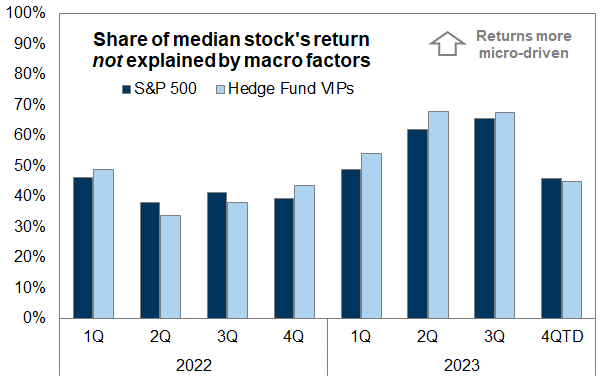

- Macro vs. micro returns

- Thematic and factor rotations: Momentum, Magnificent 7, and small-caps

- Concentration, crowding, and turnover

- Sector positions

- The Hedge Fund VIP List: "The stocks that matter most"

- The most concentrated hedge fund positions

- Rising and falling stars

- ETF ownership

- The Very Important Short Position List

- Appendix A: Hedge fund data tables

- Change in popularity: Largest increase and decrease in number of hedge fund owners

- Concentrated shorts: Highest short interest outstanding as a percentage of market cap

- Appendix B: 100 largest hedge funds in our analysis ranked by equity assets

- Appendix C: Drawbacks of our hedge fund holding analysis

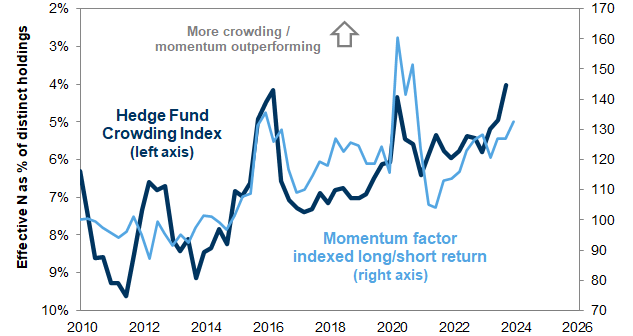

Exhibit 1: Hedge fund crowding has risen as popular positions have gained momentum

5 key points from the Goldman Sachs Hedge Fund Trend Monitor

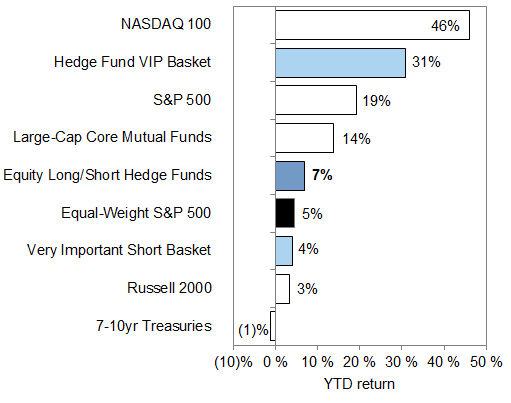

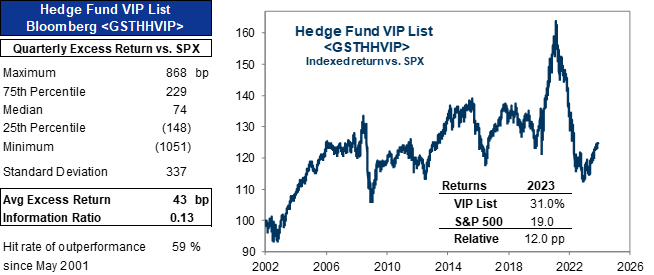

PERFORMANCE: The most popular hedge fund long and short positions have supported returns despite a deteriorating stock-picking environment Our Hedge Fund VIP list of the most popular long positions (ticker: GSTHHVIP) has returned +31% YTD, handily outperforming the S&P 500 (+19%), the equal-weight S&P 500 (+5%) and the most shorted stocks (GSCBMSAL, +0%). This outperformance has persisted despite the market volatility in recent months, with popular long positions outperforming concentrated shorts in most sectors. However, the improvement in the alpha-generation backdrop that took place earlier in 2023 has reversed, with the "micro" share of stock returns declining in 4QTD.

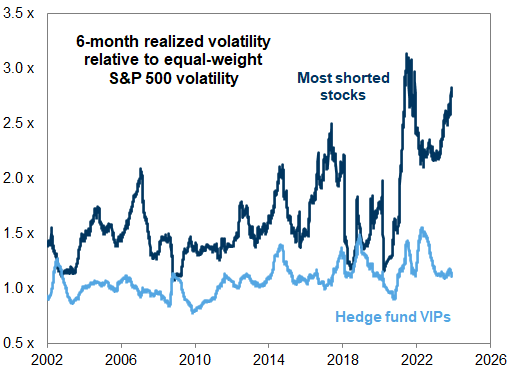

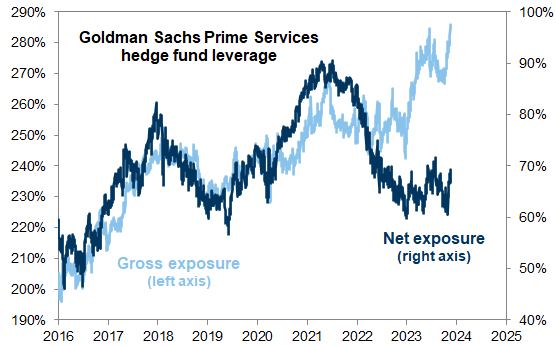

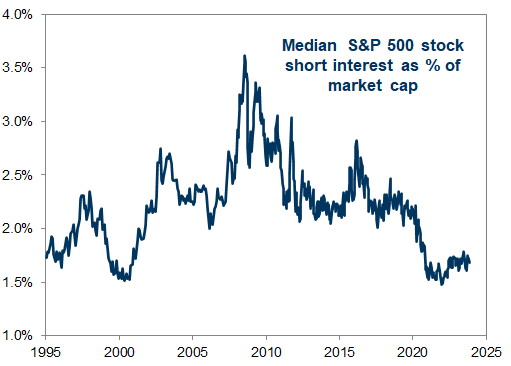

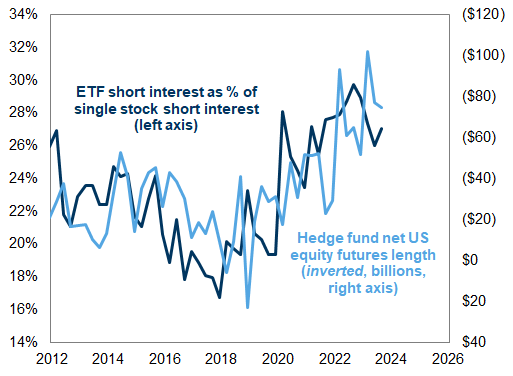

LEVERAGE AND SHORT INTEREST: Hedge funds have lifted net exposures modestly while maintaining record gross leverage. Elevated gross exposures help explain the extreme recent volatility of heavily shorted stocks. However, short interest in the typical stock remains low as funds have increasingly hedged using macro products like ETFs and futures rather than single stock shorts.

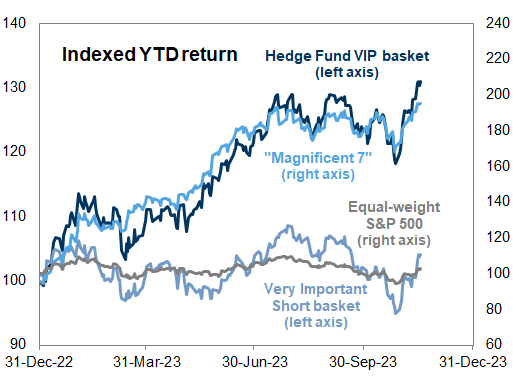

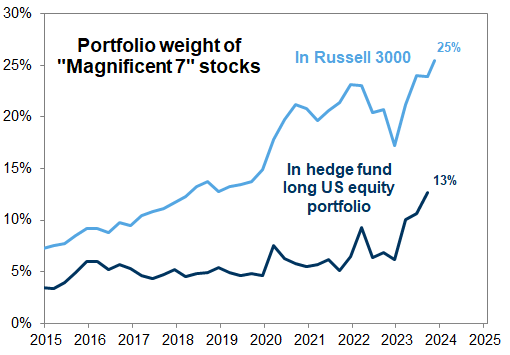

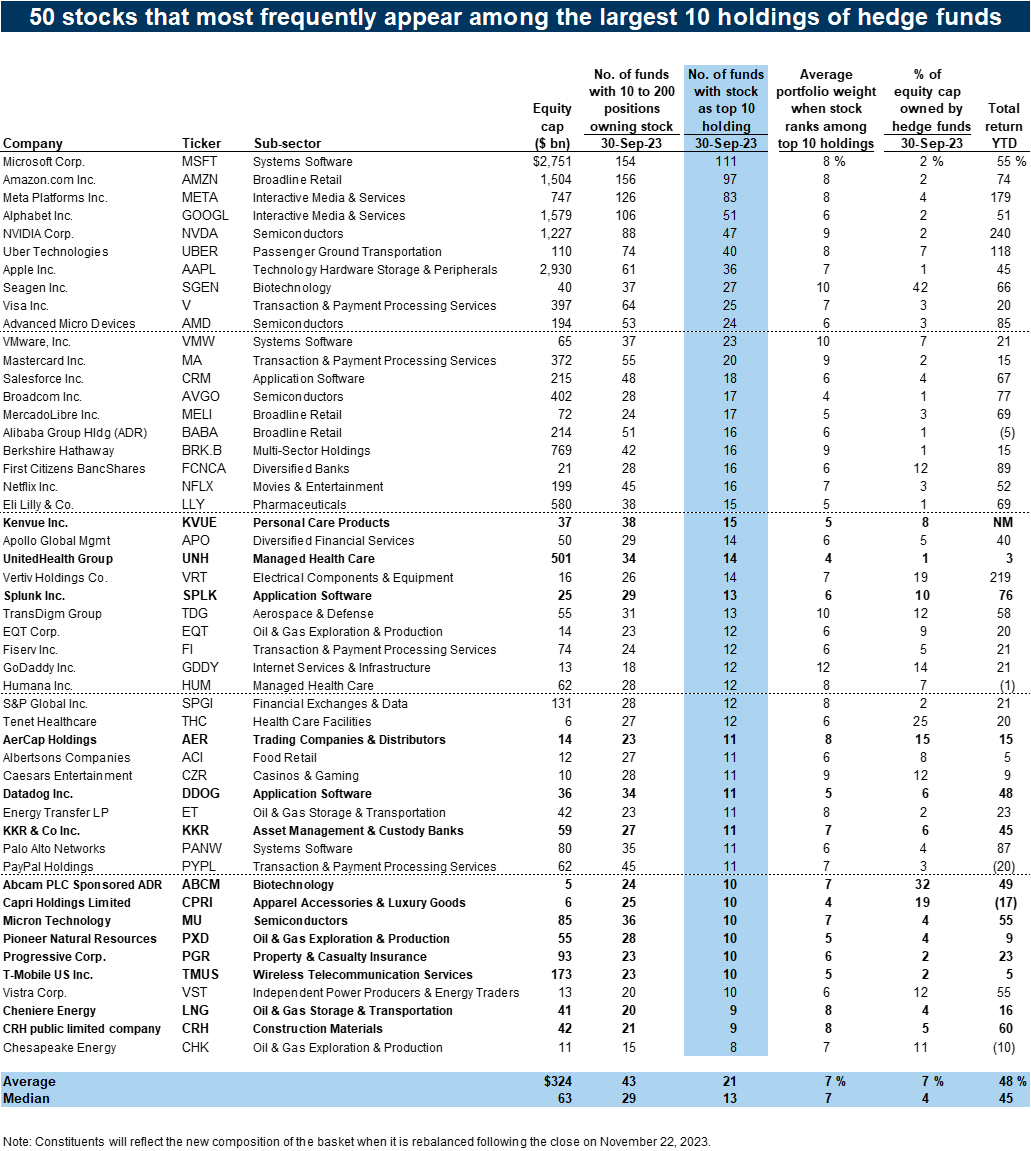

MAGNIFICENT 7: Funds bought mega-cap tech during 3Q, lifting their exposures to the "Magnificent 7" to a new high. The mega-cap tech stocks account for 13% of the aggregate hedge fund long portfolio, twice their weight at the start of 2023 but only half the stocks' weight in the Russell 3000. Except for TSLA, each of the seven rank among the top 10 members of our Hedge Fund VIP list. MSFT and AMZN have been the top two VIPs for nine consecutive quarters.

HEDGE FUND VIPS: The mega-caps remain the most popular hedge fund long positions. The top 6 stocks this quarter (MSFT, AMZN, META, GOOGL, NVDA, UBER) also ranked as the top 6 last quarter. The VIP list contains the 50 stocks that appear most often among the top 10 holdings of fundamental hedge funds. The basket has outperformed the S&P 500 in 59% of quarters since 2001 with an average quarterly excess return of 43 bp. 14 new constituents: ABCM, AER, CPRI, CRH, DDOG, KKR, KVUE, LNG, MU, PGR, PXD, SPLK, TMUS, and UNH.

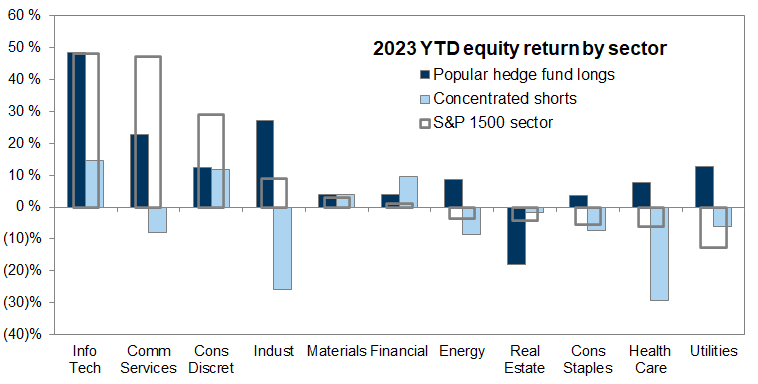

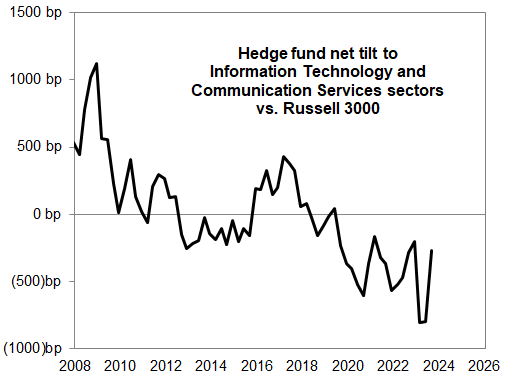

SECTORS: Hedge funds added heavily to Tech last quarter, with broad-based increases across industries. Funds sold Health Care, but it remains the largest sector overweight relative to the Russell 3000. Funds also sold Energy, where tilts are close to the lowest since before the GFC. The consumer remains a point of debate, with consumer firms heavily represented on our list of "controversial" stocks with high ownership and high short interest (Exhibit 15). CZR, DLTR, HLT, SYF, and WYNN joined our High Hedge Fund Concentration basket (Exhibit 39). Similarly, funds remained underweight Financials and JPM and C fell out of our VIP list, but CMA, JEF, MKTX, WAL, and ZION ranked among the stocks with the largest decrease in short interest during the last few months.

Performance, leverage, and short interest

Exhibit 2: GS Prime Services estimates a 7% YTD return for US long/short equity hedge funds

Exhibit 3: The most popular hedge fund positions have fared well YTD

Exhibit 4: The most popular hedge fund long positions have outperformed the most concentrated shorts in most sectors YTD

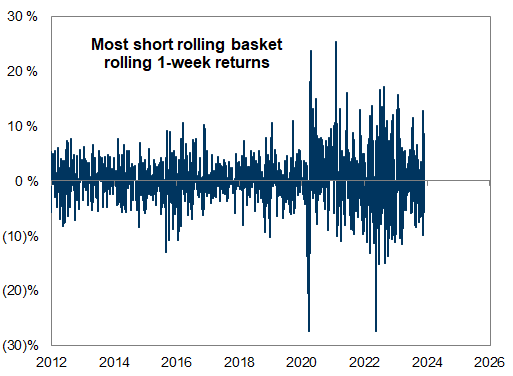

Exhibit 5: Short positions have been particularly volatile in recent years

Exhibit 6: Highly shorted stocks have recently been highly volatile

Exhibit 7: Hedge fund gross and net leverage

Exhibit 8: Short interest for the typical stock remains low vs. history

Exhibit 9: Funds have increasingly used macro products as shorts

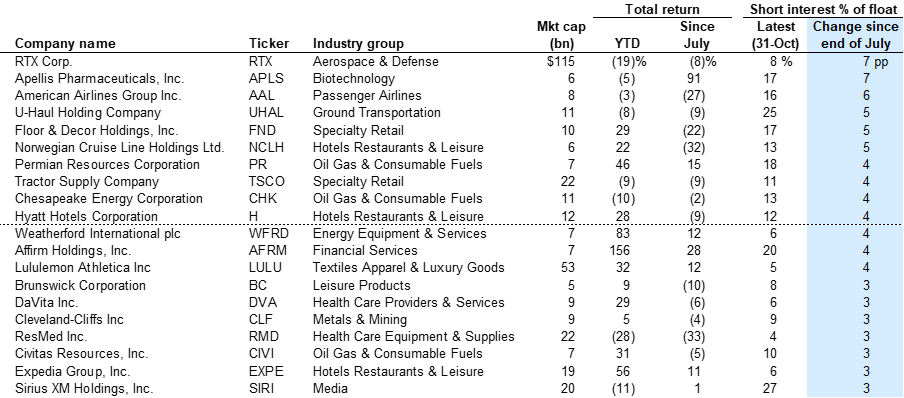

Exhibit 10: Stocks with largest increases in short interest since end of July

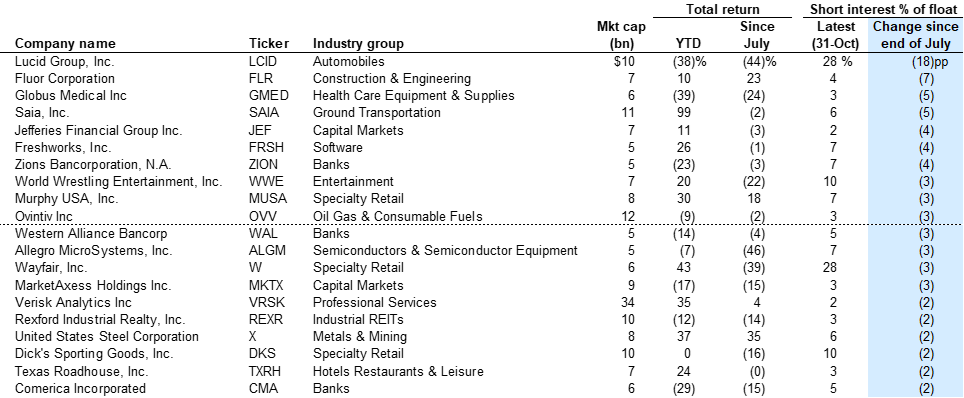

Exhibit 11: Stocks with largest decreases in short interest since end of July

Macro vs. micro returns

Exhibit 12: The trend toward increasingly micro-driven stock returns has reversed QTD

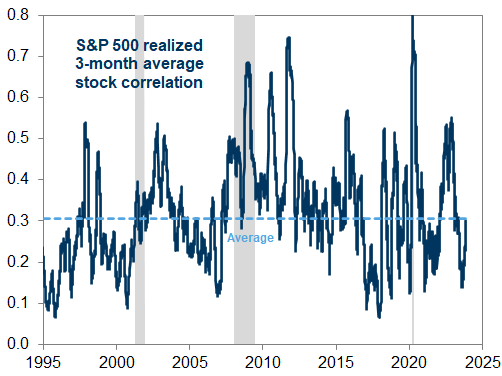

Exhibit 13: S&P 500 average realized stock correlation has recently risen

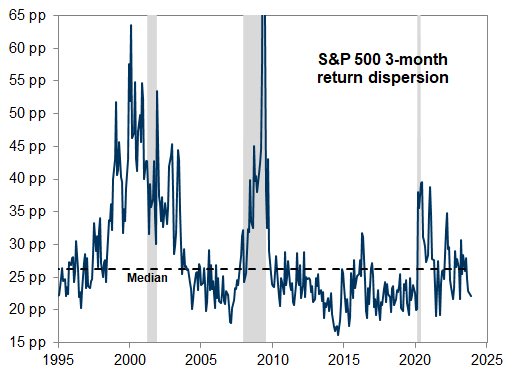

Exhibit 14: Falling dispersion narrows the alpha opportunity for stock-pickers

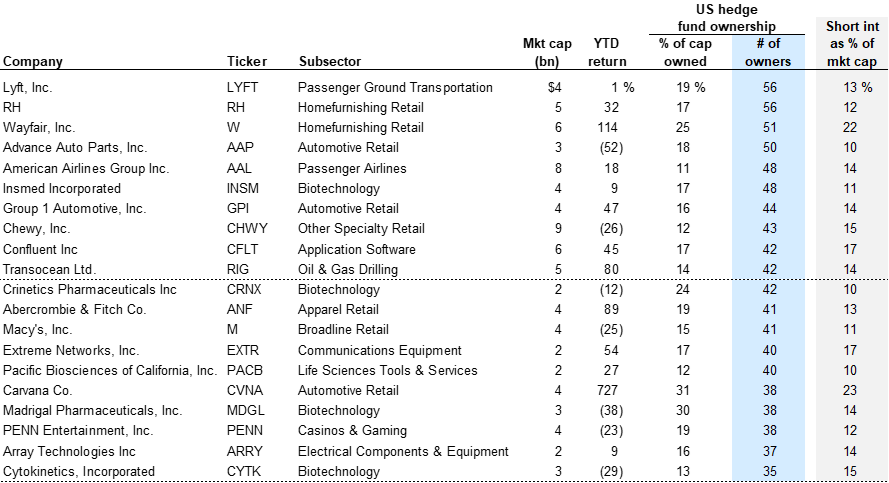

Exhibit 15: Stocks with market caps > $2 billion that rank highly on both hedge fund popularity and short interest

Thematic and factor rotations: Momentum, Magnificent 7, and small-caps

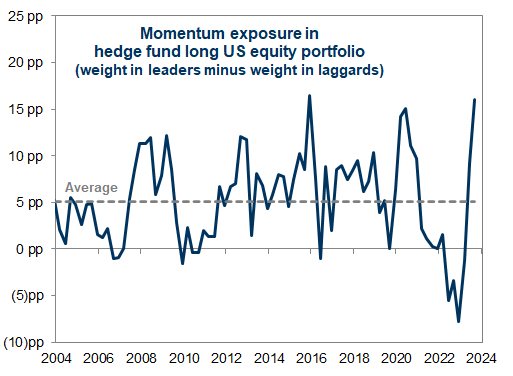

Exhibit 16: Fund portfolios have rarely been more tilted toward Momentum

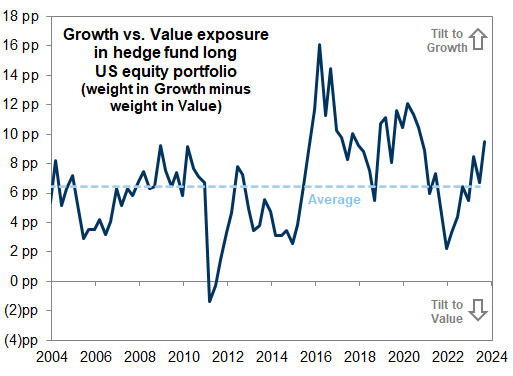

Exhibit 17: Hedge fund portfolios continued to rotate toward Growth during 3Q

Exhibit 18: The weight of mega-cap tech stocks in hedge fund long portfolios has doubled YTD

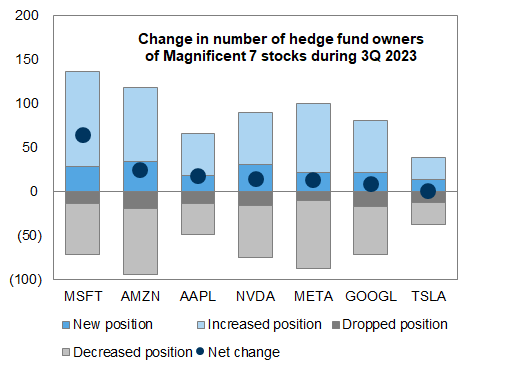

Exhibit 19: Hedge funds added to positions in mega-cap tech stocks during 3Q

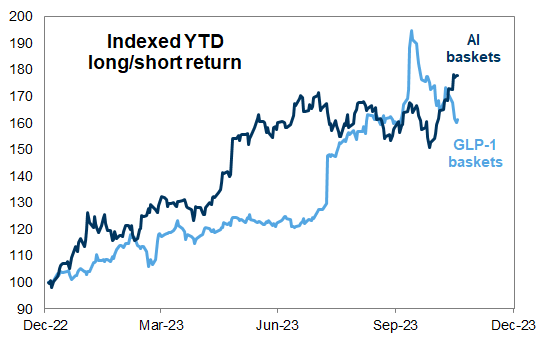

Exhibit 20: AI and GLP-1 themes have captured market focus this year

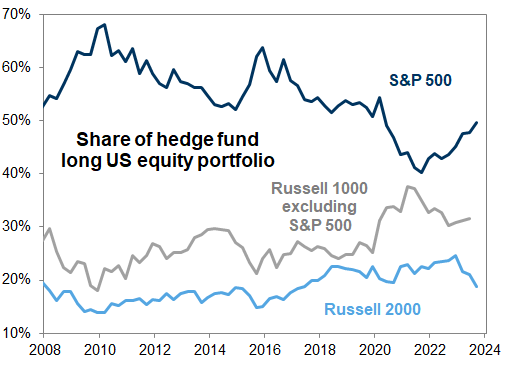

Exhibit 21: Small-cap weight in hedge fund portfolios has declined as large stocks have outperformed

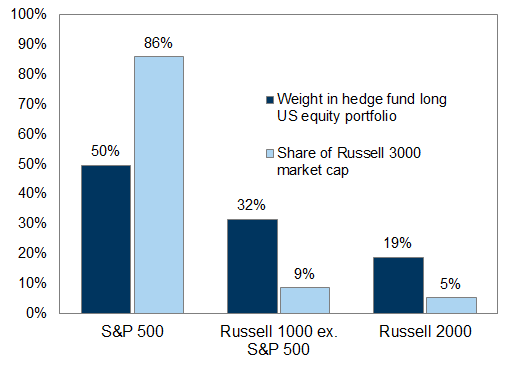

Exhibit 22: Hedge funds remain concentrated in small stocks compared to the market

Concentration, crowding, and turnover

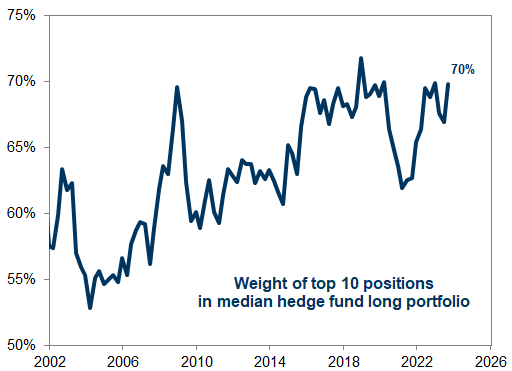

Exhibit 23: Hedge fund portfolio density increased

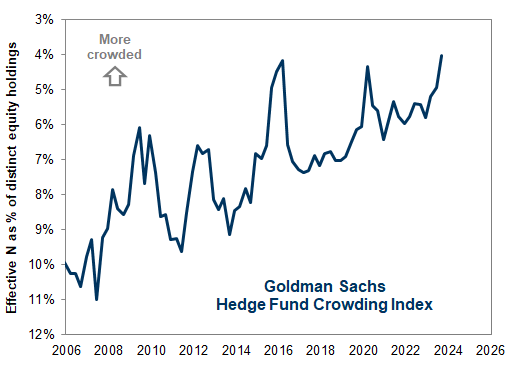

Exhibit 24: Crowding across hedge funds increased in 3Q

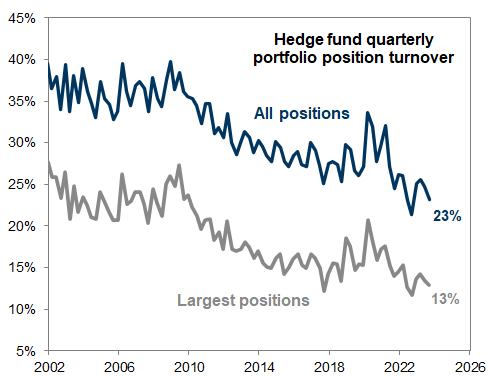

Exhibit 25: Portfolio turnover decreased in 3Q

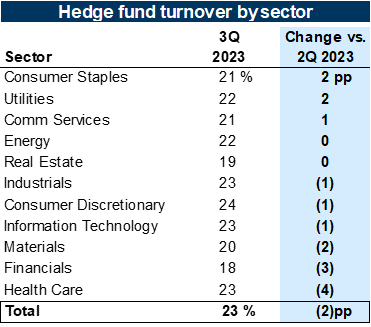

Exhibit 26: Portfolio position turnover varied across sectors

Sector positions

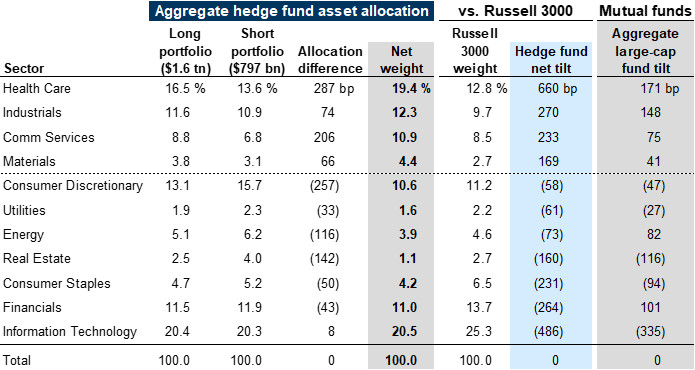

Exhibit 27: Hedge fund sector allocations relative to the Russell 3000 and large-cap mutual funds

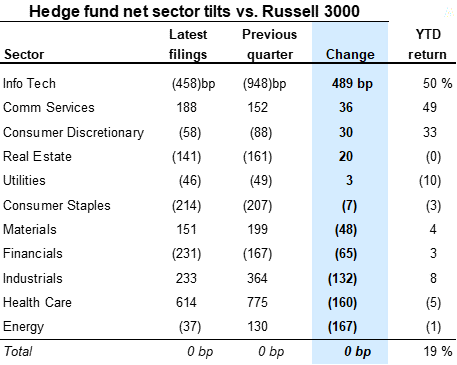

Exhibit 28: Changes in hedge fund sector tilts during 3Q

Exhibit 29: Funds added to tech during 3Q

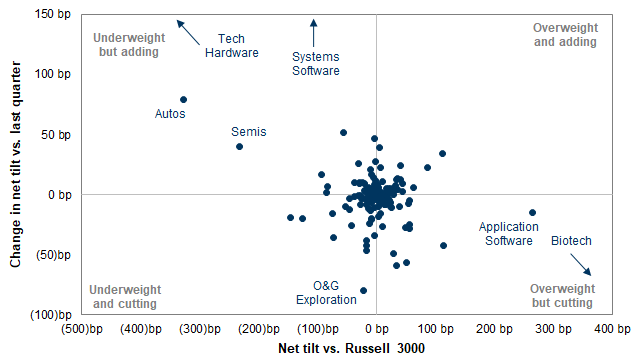

Exhibit 30: Subsector tilts and changes in tilts

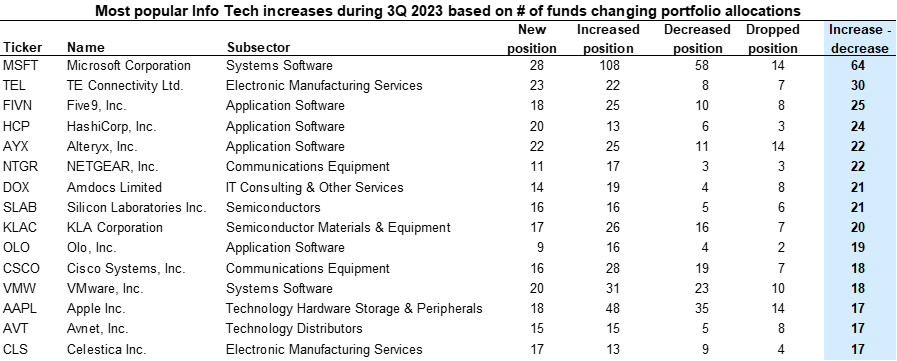

Exhibit 31: Info Tech stocks with the largest net increase in hedge fund popularity last quarter

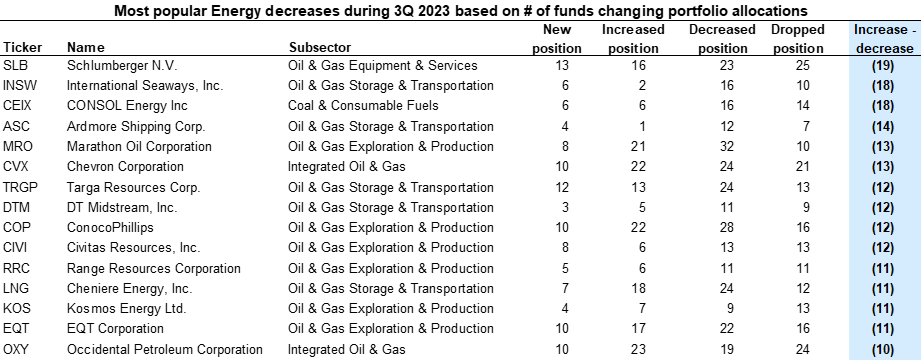

Exhibit 32: Energy stocks with the largest net decrease in hedge fund popularity last quarter

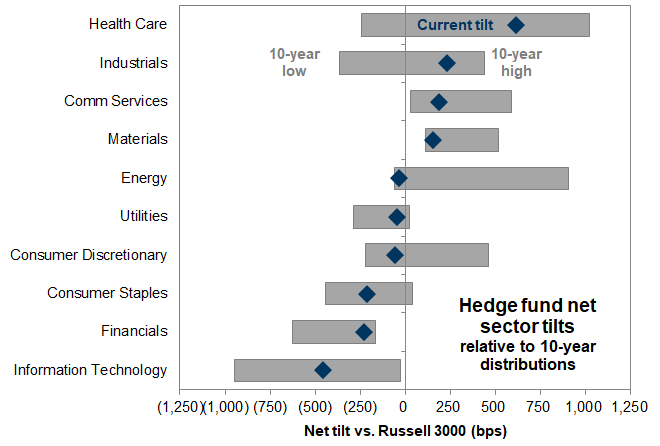

Exhibit 33: Hedge fund net sector tilts relative to past decade

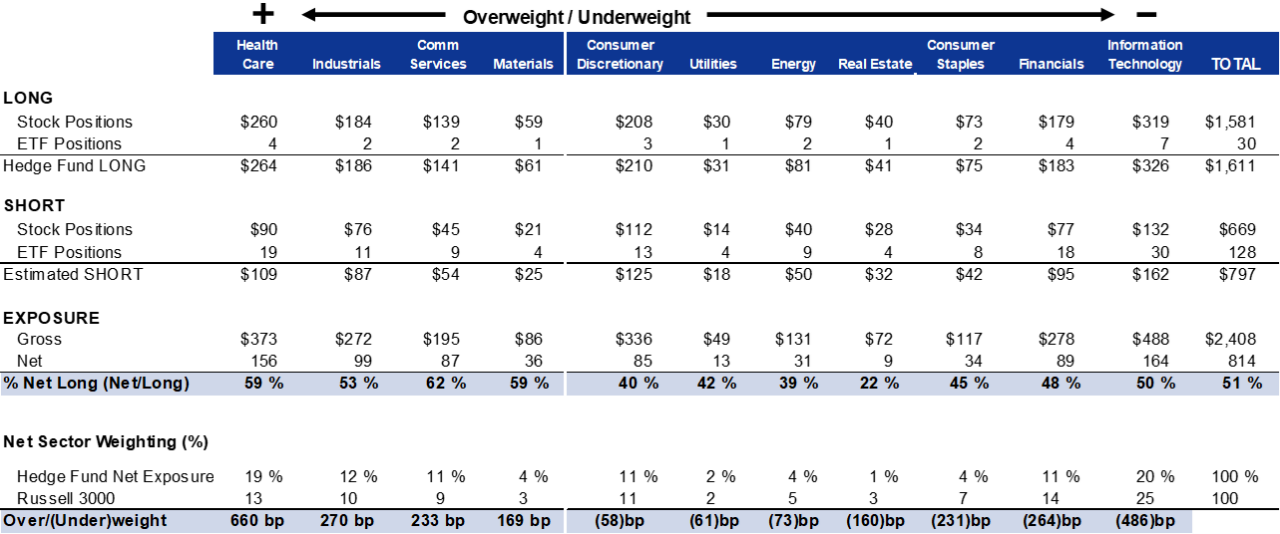

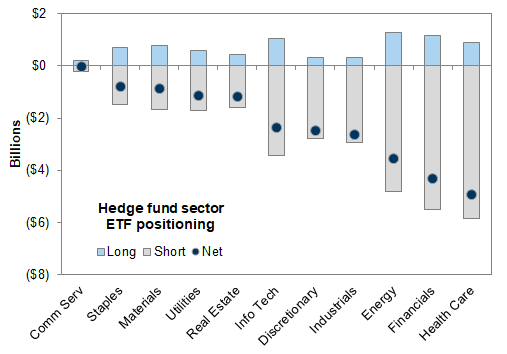

Exhibit 34: Estimated hedge fund long, short, and net exposure, by sector ($ in billions)

The Hedge Fund VIP List: "The stocks that matter most"

Exhibit 35: Hedge fund VIPs have outperformed by 43 bp on average each quarter since 2001 (90 quarters)

GSTHHVIP: The 50 stocks that matter most to hedge funds

Exhibit 36: Very Important Positions (VIP) for hedge funds

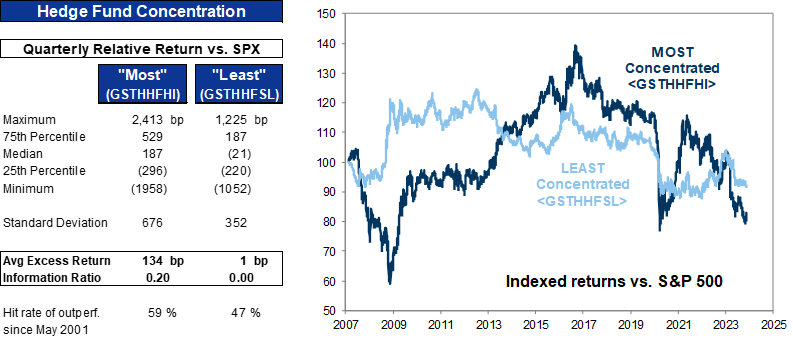

The most concentrated hedge fund positions

Exhibit 37: Hedge fund concentration baskets versus the S&P 500

Exhibit 38: The most concentrated stocks have underperformed the S&P 500 by 19 pp YTD

Goldman Sachs S&P 500 hedge fund concentration baskets

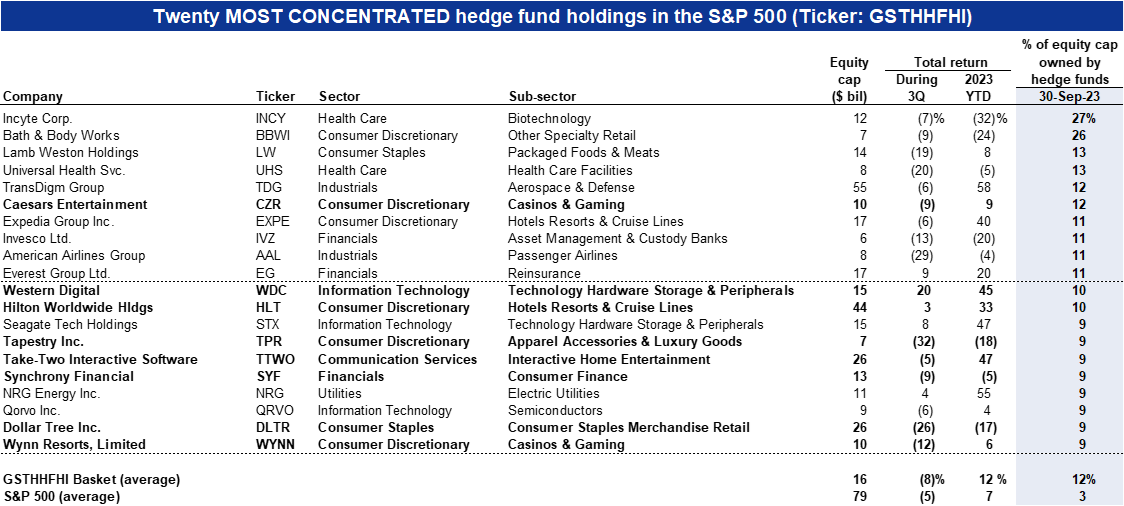

Exhibit 39: The 20 S&P 500 stocks with the most concentrated hedge fund ownership <ticker: GSTHHFHI>

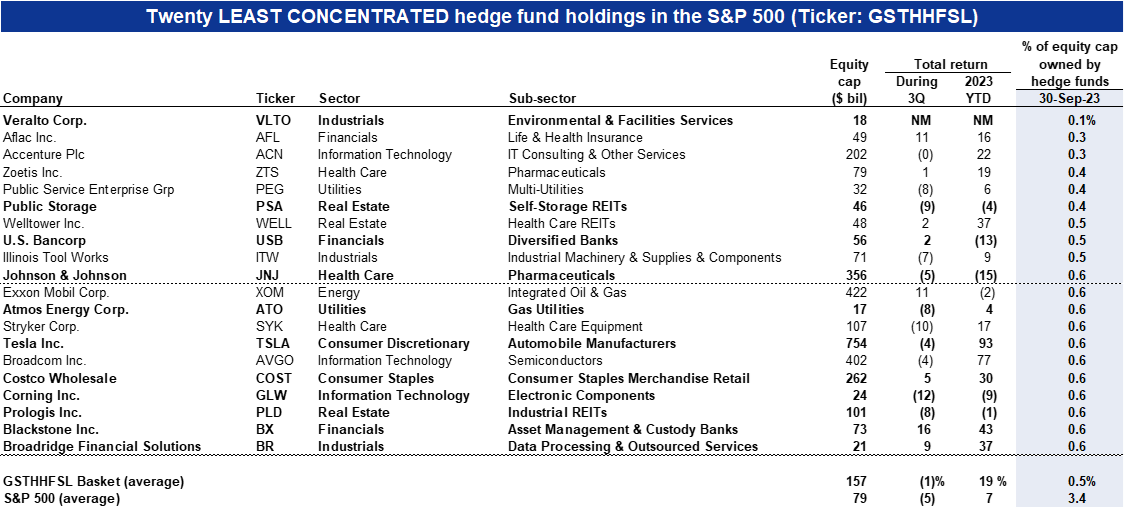

Exhibit 40: The 20 S&P 500 stocks with the least hedge fund concentration <ticker: GSTHHFSL>

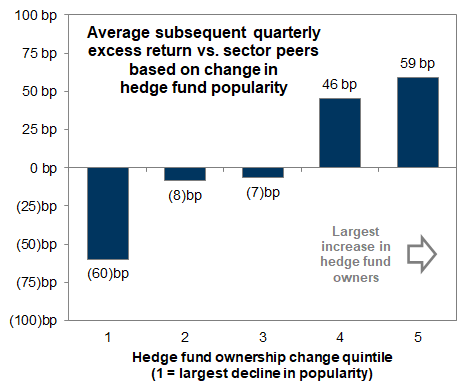

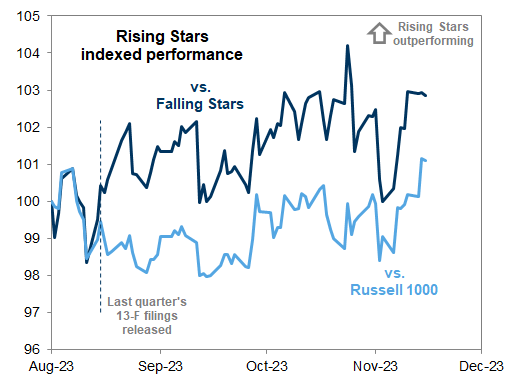

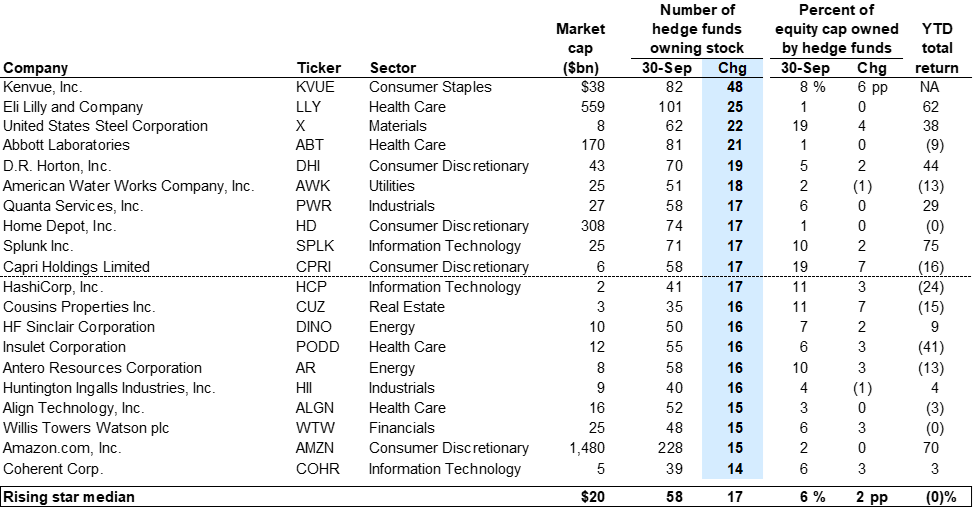

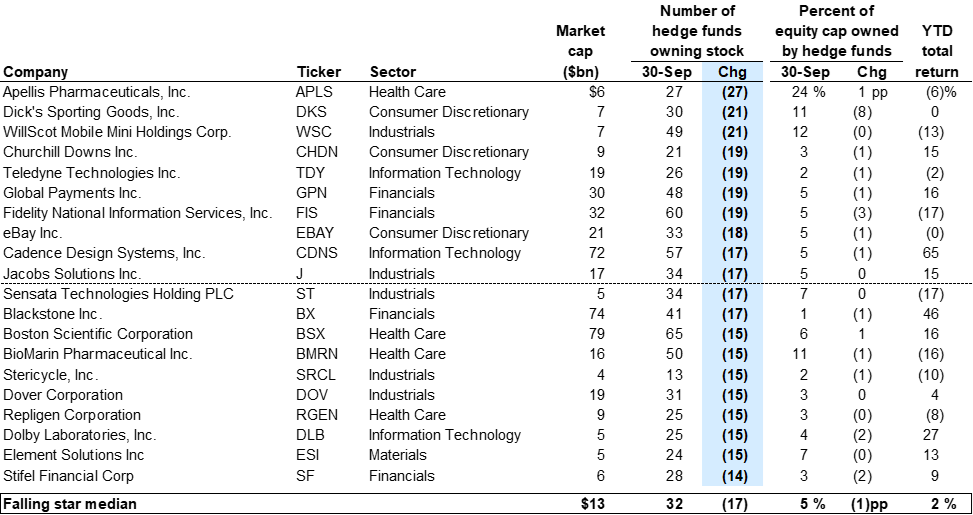

Rising and falling stars

Exhibit 41: Change in popularity has been a signal for forward returns

Exhibit 42: Last quarter's Rising Stars have outperformed Falling Stars and the Russell 1000

Exhibit 43: Rising stars: Russell 1000 stocks with the largest increase in number of hedge fund owners during 3Q 2023

Exhibit 44: Falling stars: Russell 1000 stocks with the largest decrease in number of hedge fund owners during 3Q 2023

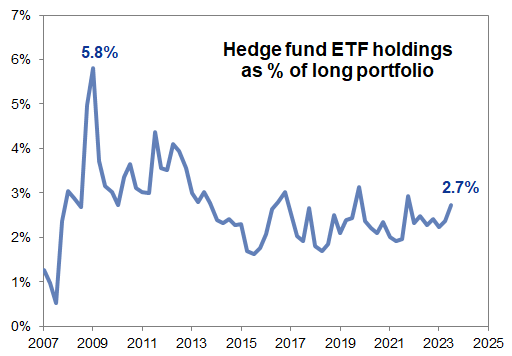

ETF ownership

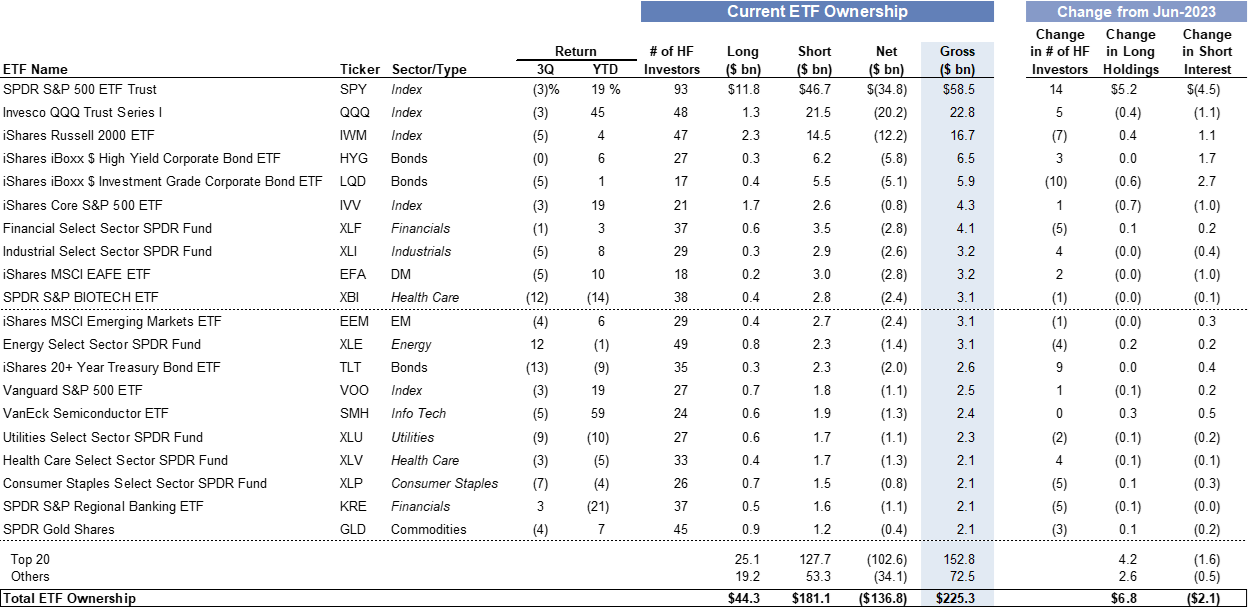

Exhibit 45: Hedge fund ETF long exposure

Exhibit 46: Hedge fund positions in sector ETFs

Exhibit 47: Top 20 ETFs by hedge fund ownership (long and short)

The Very Important Short Position List

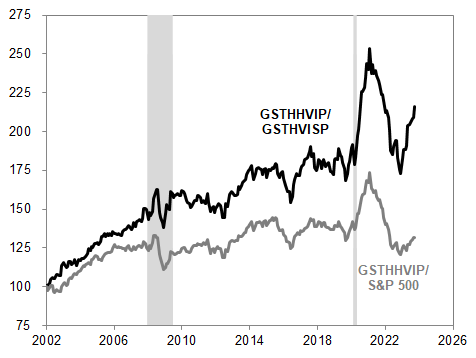

Exhibit 48: Hedge fund VIP basket pairs

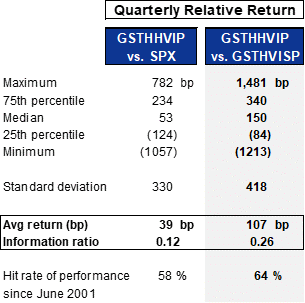

Exhibit 49: Information ratio of VIP vs. VISP is 0.26

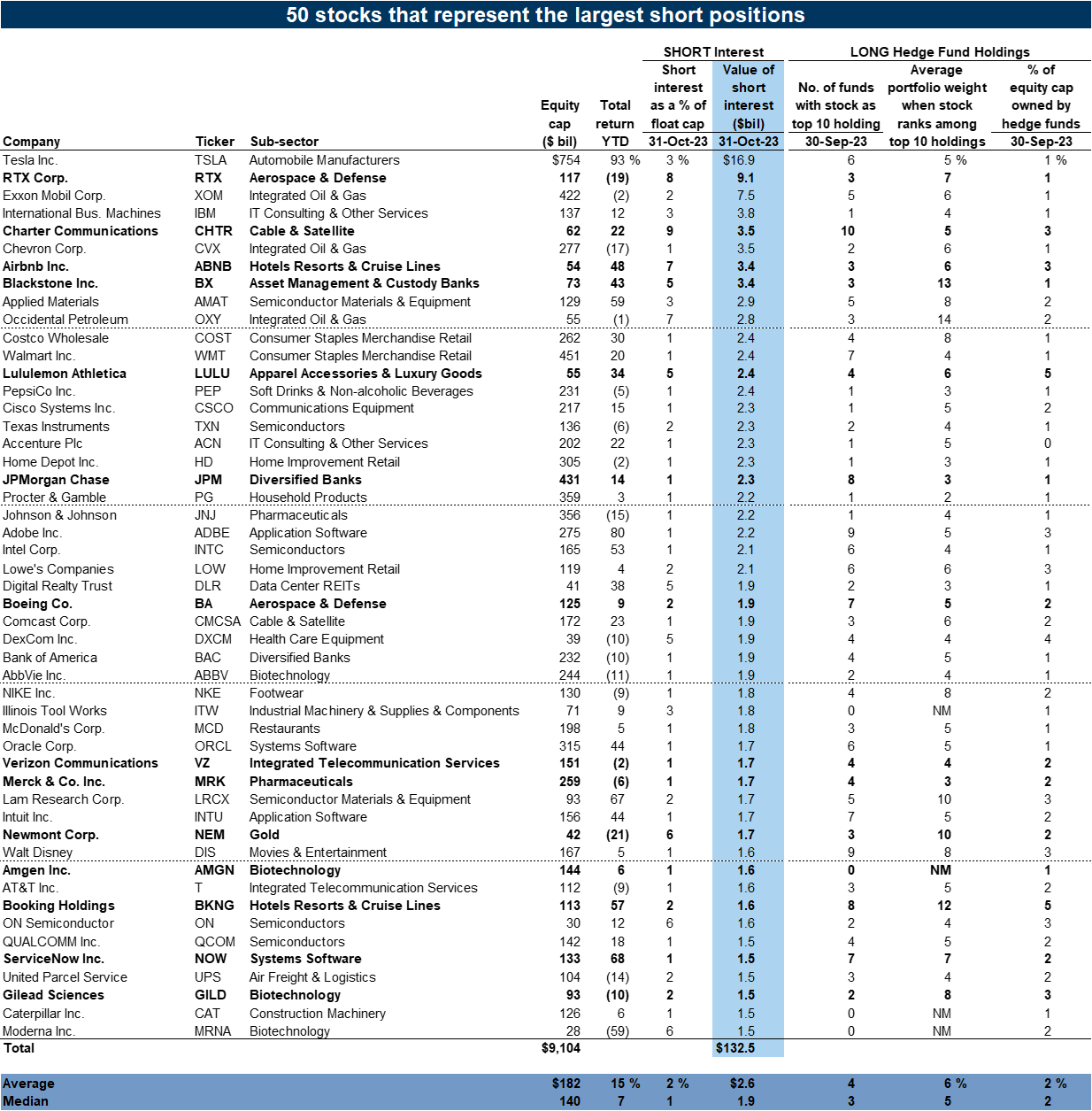

GSTHVISP: 50 stocks representing the largest short positions

Exhibit 50: Very Important Short Positions (VISP) for hedge funds

Appendix A: Hedge fund data tables

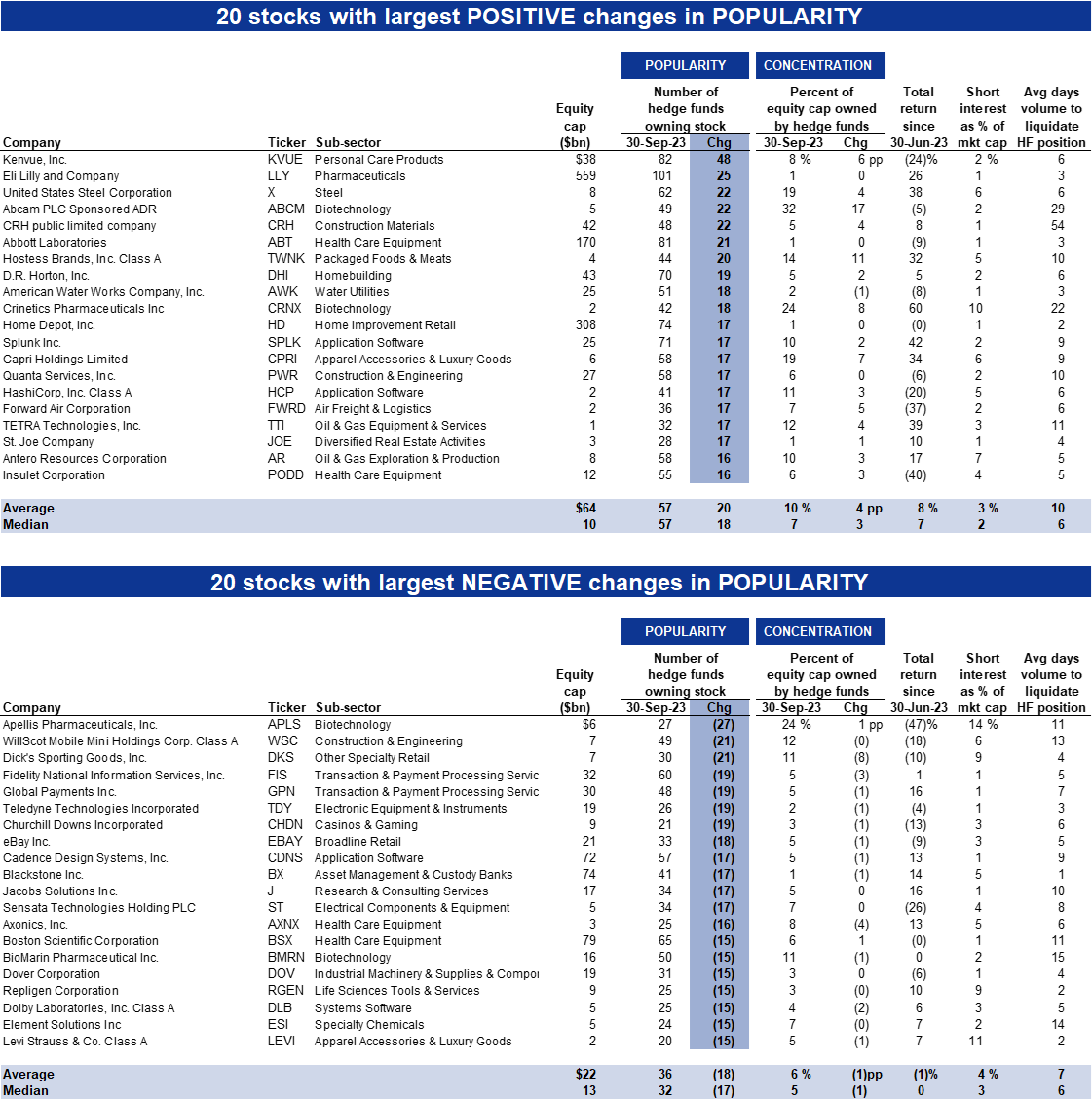

Change in popularity: Largest increase and decrease in number of hedge fund owners

Exhibit 51: Change in popularity during 3Q 2023

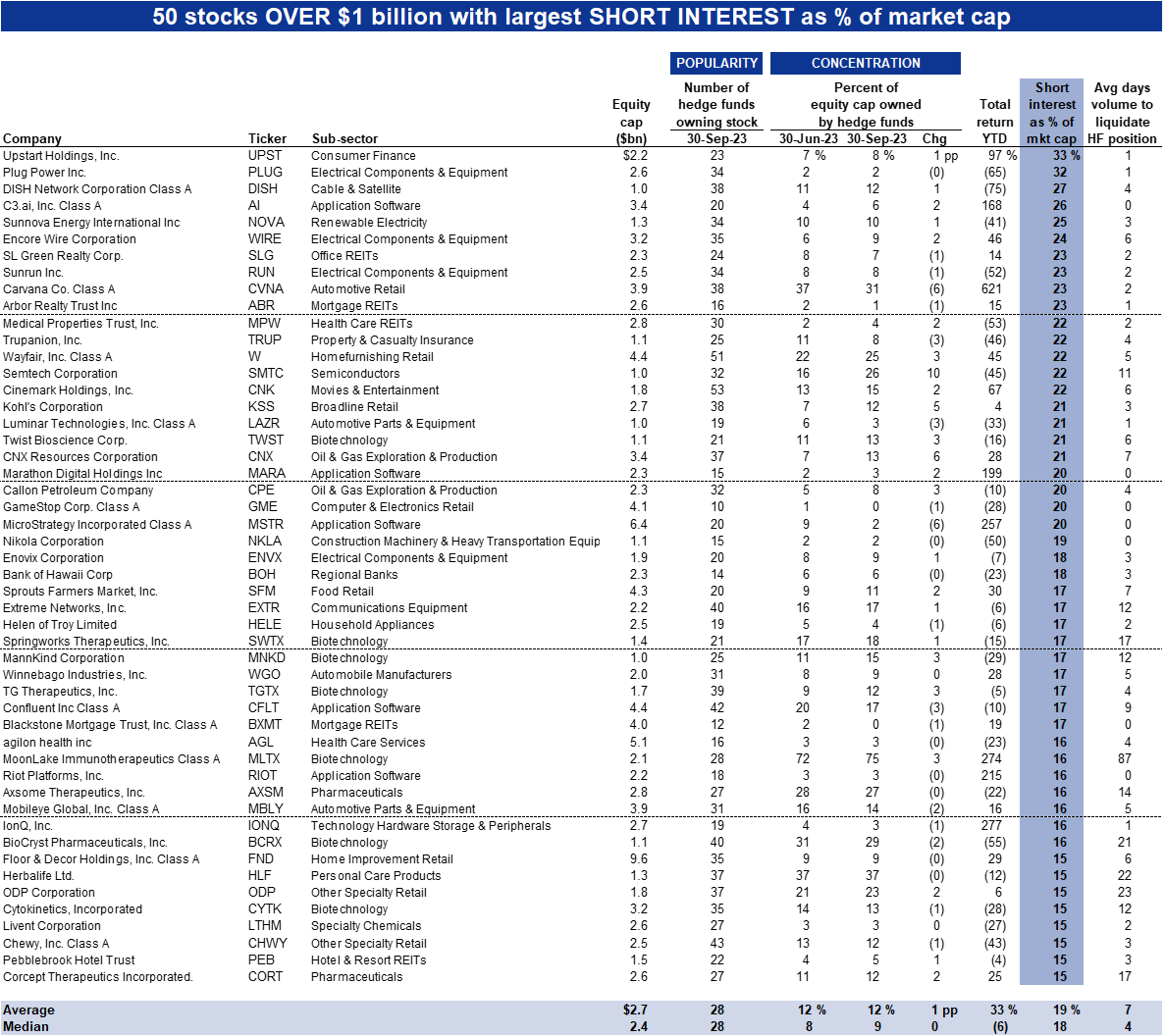

Concentrated shorts: Highest short interest outstanding as a percentage of market cap

Exhibit 52: Highest short interest: Stocks over $1 billion in market cap

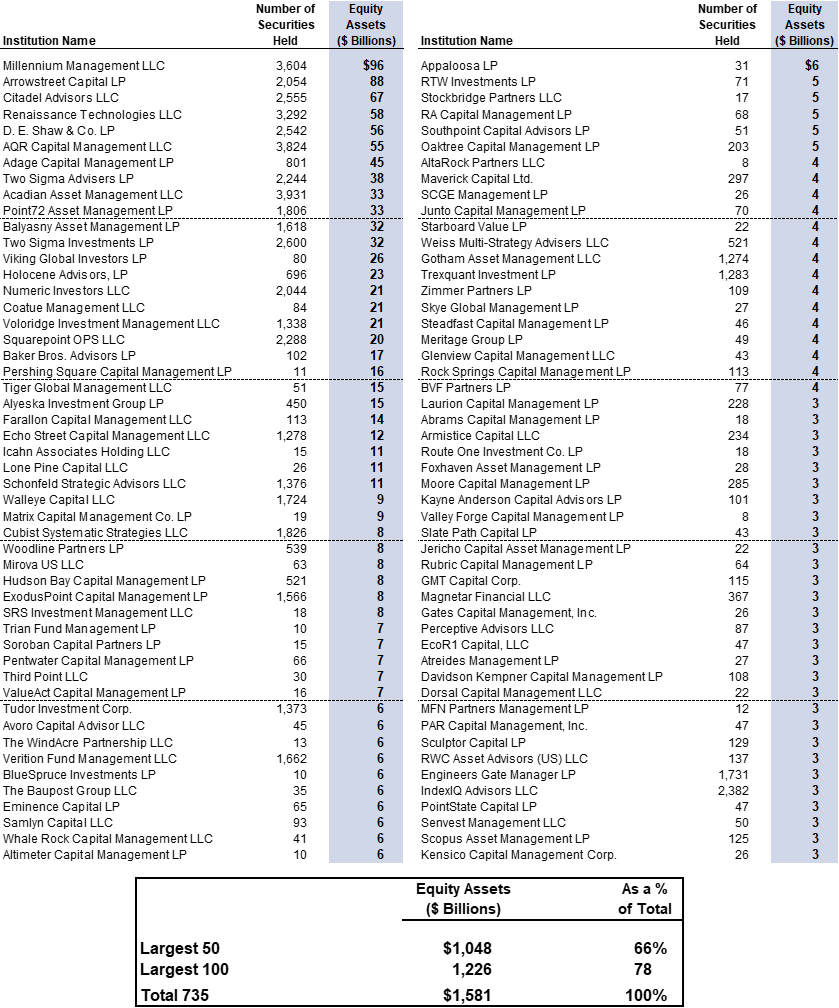

Appendix B: 100 largest hedge funds in our analysis ranked by equity assets

Appendix C: Drawbacks of our hedge fund holding analysis

Data limitations

Lack of international holdings

Incomplete reporting of short positions

Timeliness

- 1 ^ Hedge Fund Crowding Index is measured as the effective N (calculated as 1/Σ[weight2]) divided by the number of distinct equities in the aggregate portfolio of hedge funds with between 10 and 200 individual equity positions.

Investors should consider this report as only a single factor in making their investment decision. For Reg AC certification and other important disclosures, see the Disclosure Appendix, or go to www.gs.com/research/hedge.html.