We wish all of our readers a happy, healthy, and prosperous 2024. In the last US Economics Analyst of the year, we discuss what we believe are the most important questions for 2024.

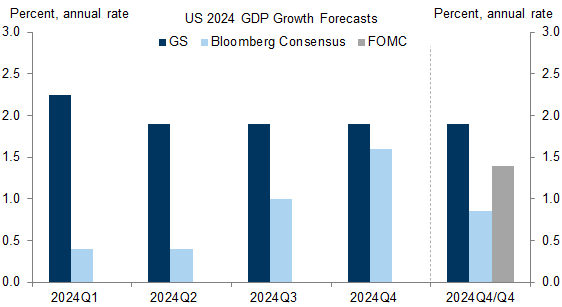

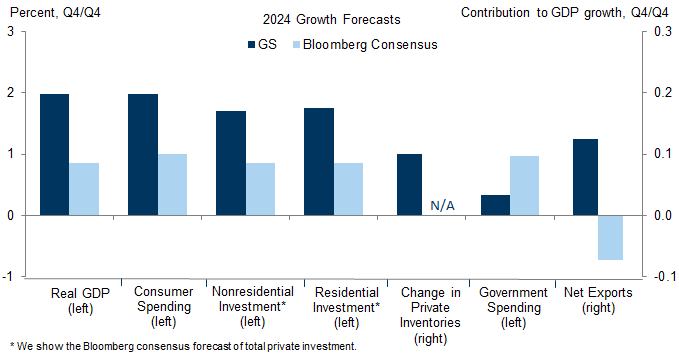

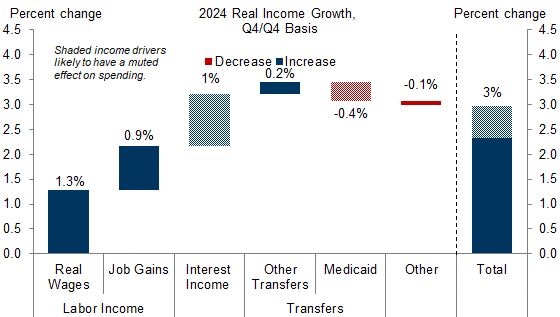

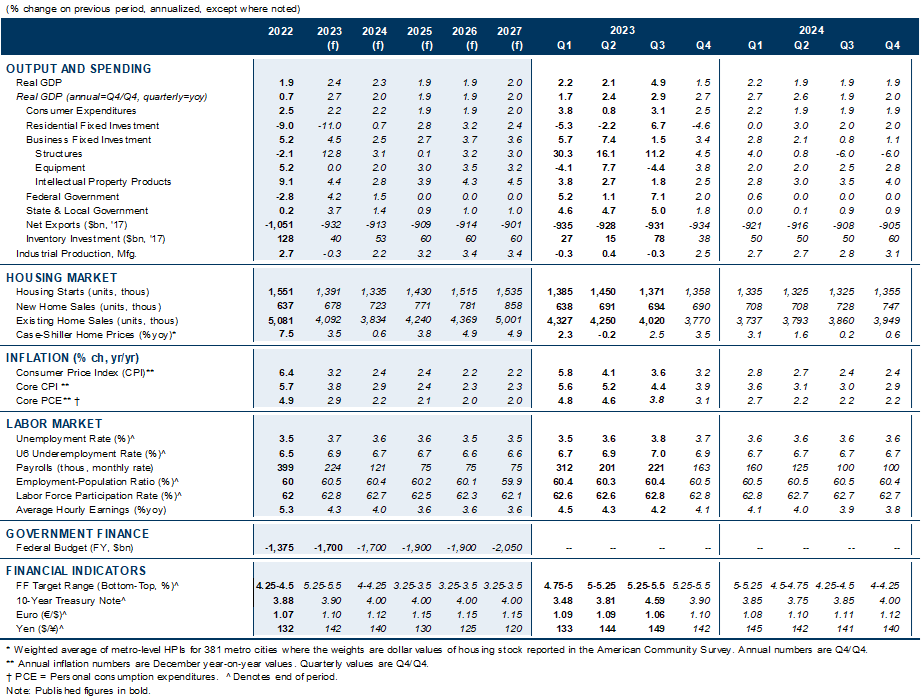

Our most out-of-consensus call for 2024 is our growth forecast. Our 2% forecast for 2024 Q4/Q4 GDP growth is well above consensus of 0.9% and the FOMC’s 1.4% forecast. This reflects our view that the growth impulses from changes in financial conditions and changes in fiscal policy should be modest and roughly neutral on net next year. It also reflects our forecast that consumer spending will easily beat expectations—we expect 2% growth vs. consensus of 1%—because real income should grow about 3% and household net worth is close to an all-time high.

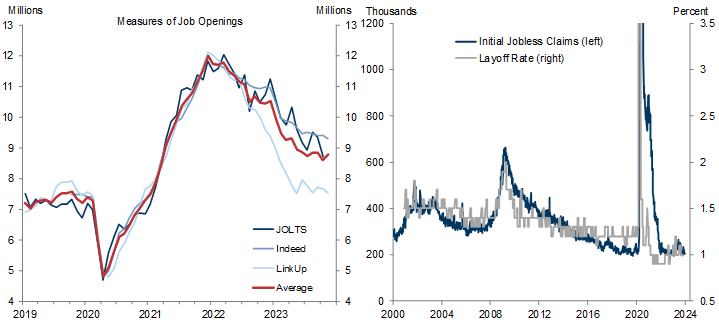

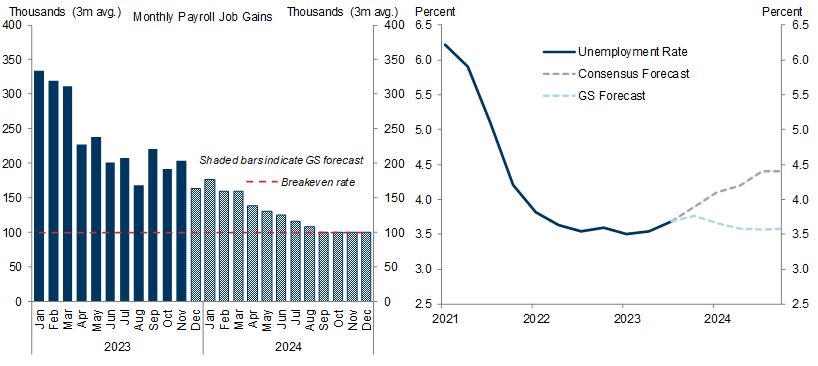

Consistent with our growth view, we expect the labor market to remain strong. The healthy starting point of still-high job openings and a low layoff rate coupled with fading recession fears should support steady job gains in 2024 at a rate that gradually converges over the year to the current breakeven pace of about 100k. This should keep the unemployment rate low at around 3.6%.

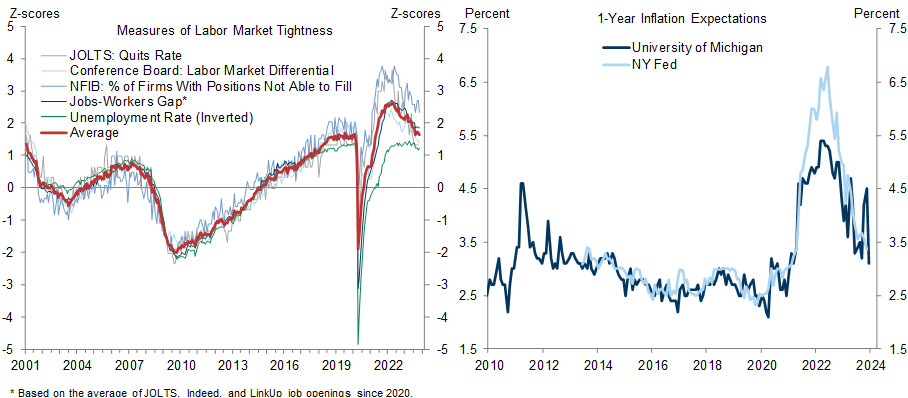

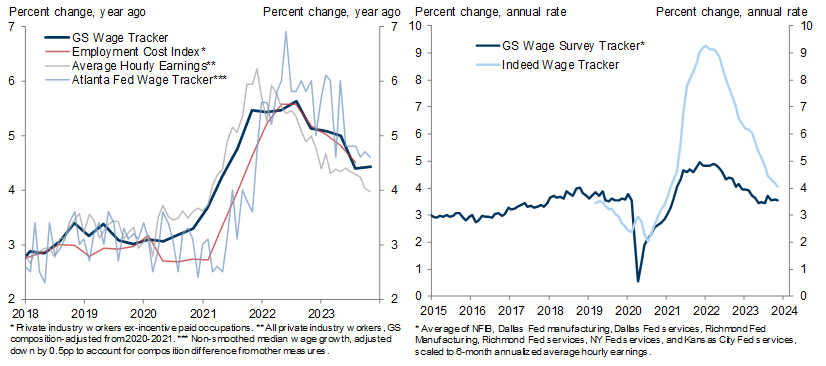

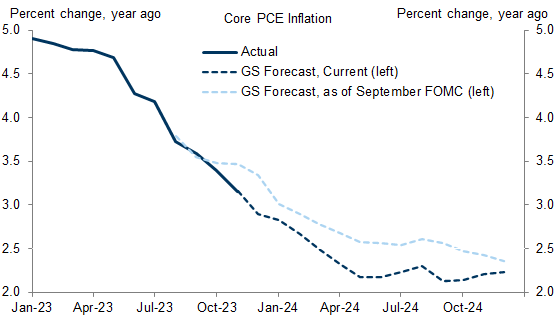

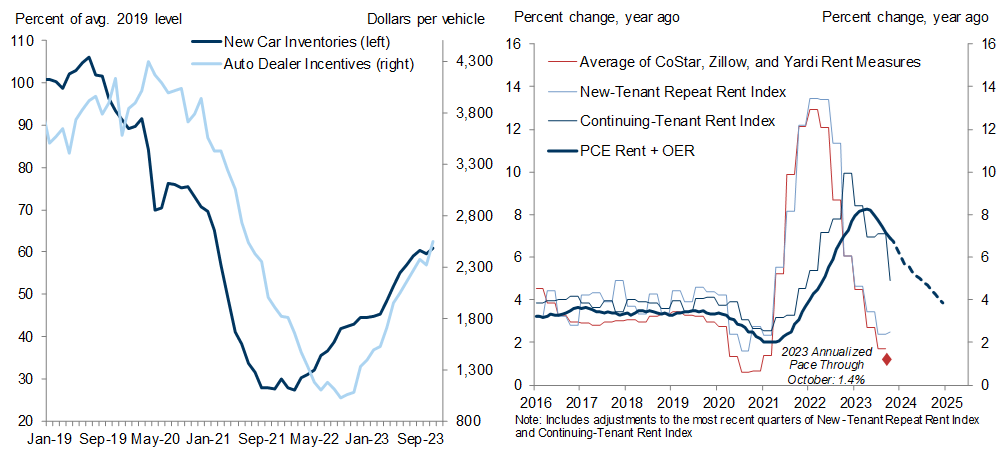

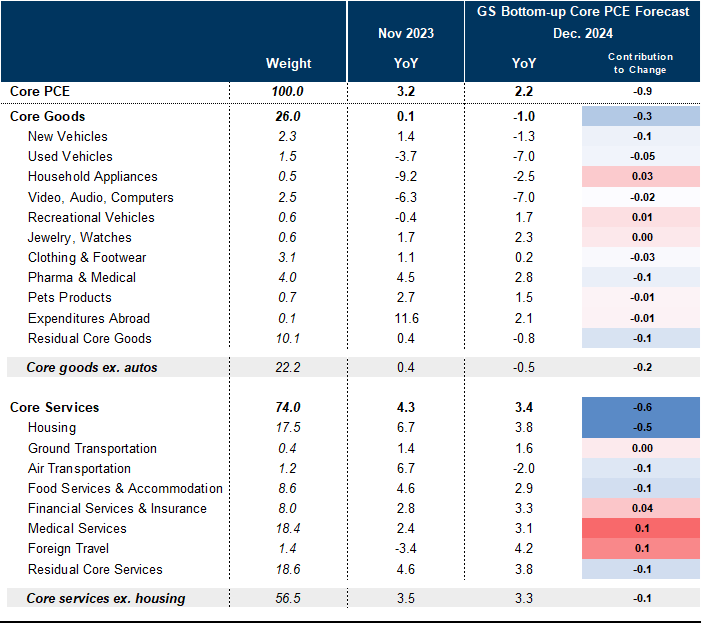

Wage growth and inflation should fall to roughly target-compatible levels in 2024. The main drivers of high wage growth over the last two years—extreme labor market overheating and big inflation shocks that sparked demands for larger cost-of-living adjustments—are now behind us. As a result, wage growth should keep falling toward the 3.5% pace we estimate is compatible with 2% inflation. Core PCE inflation slowed sharply in 2023H2 and appears on track to fall into the low 2s on a year-on-year basis by spring. We expect further rebalancing in the auto and housing rental markets to leave the year-on-year rate at 2.2% at the end of 2024, undershooting the FOMC’s 2.4% forecast, and we see a reasonable chance that it could fall below 2%.

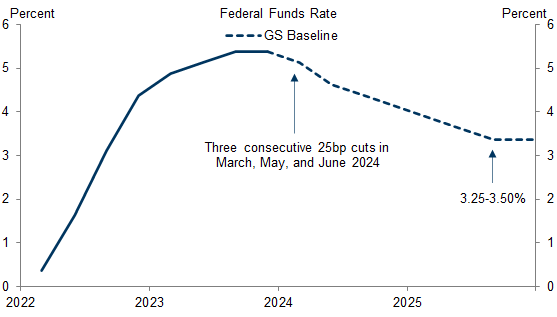

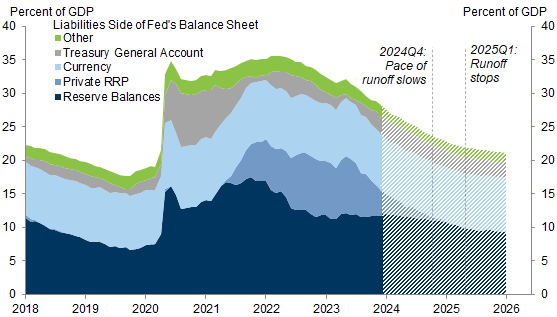

The rapid decline in inflation is likely to lead the FOMC to cut early and fast to reset the policy rate from a level that most participants will likely soon see as far offside. We expect three consecutive 25bp cuts in March, May, and June, followed by one cut per quarter until the funds rate reaches 3.25-3.5% in 2025Q3. Our forecast implies 5 cuts in 2024 and 3 more cuts in 2025. We also expect the Fed to slow balance sheet runoff in 2024Q4 and to end it fully in 2025Q1.

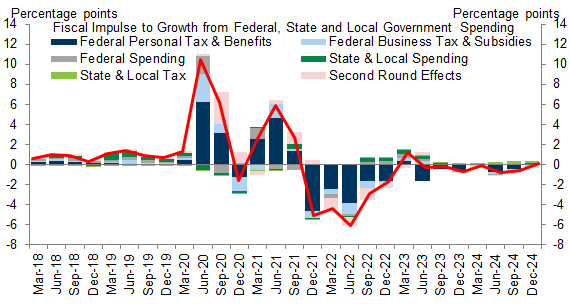

Fiscal policy is very unlikely to become more stimulative ahead of the election. In fact, we see downside risk to government spending from automatic spending cuts that will take effect in May if Congress continues to avoid government shutdowns by passing temporary extensions instead of full-year spending bills. The cuts would reduce funding by around 2% (0.4% of GDP).

10 Questions for 2024

Exhibit 1: Our 2% Forecast for 2024 Q4/Q4 GDP Growth Is Well Above Consensus of 0.9% and the FOMC’s Forecast of 1.4%

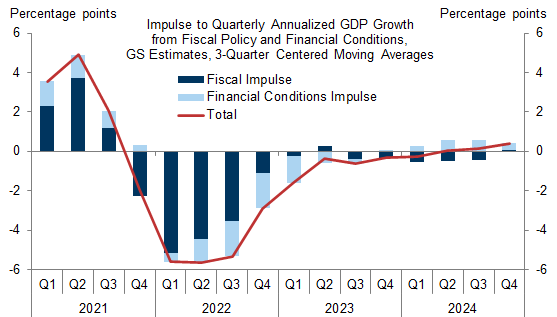

Exhibit 2: The Growth Hit from Fiscal and Monetary Policy Tightening Is Largely Behind Us, and the Net Impact of the Two on GDP Growth Should Be Roughly Neutral in 2024

Exhibit 3: We Are More Optimistic Than Consensus on Consumption, Business and Residential Investment, and Trade

Exhibit 4: We Expect Positive Real Wage Gains, Solid Job Gains, and Higher Interest Income to Fuel Real Disposable Income Growth of Around 3% and Consumption Growth of Around 2% in 2024

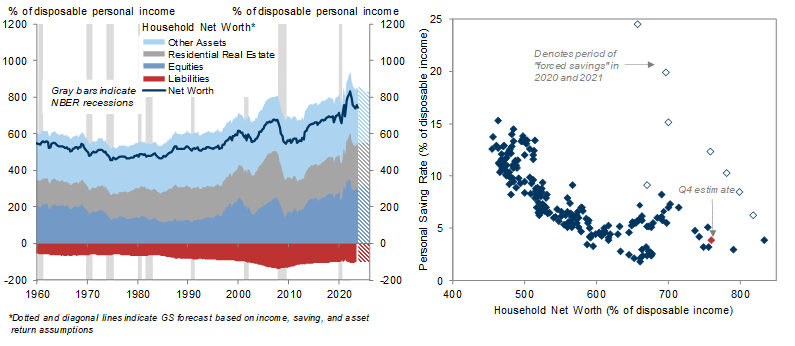

Exhibit 5: The Near-Record Level of Household Net Worth Should Continue to Support Spending and Implies That the Saving Rate Should Remain Low by Historical Standards

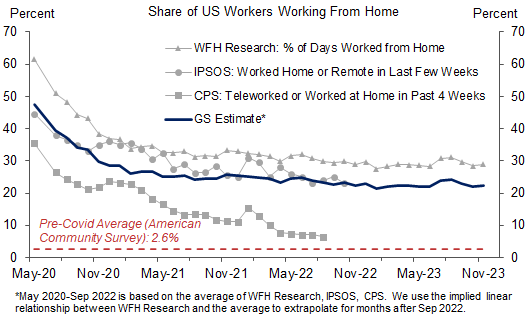

Exhibit 6: Remote Work Is Likely to Be the Most Enduring Economic Legacy of the Pandemic Years

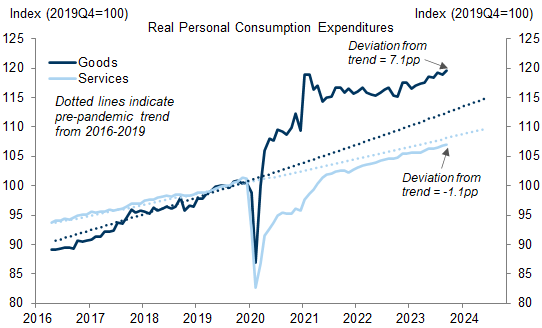

Exhibit 7: Remote Work Is Likely the Main Driver of the Large and Persistent Gap Between Real Goods Spending and Real Services Spending, Which Appears Likely to Last

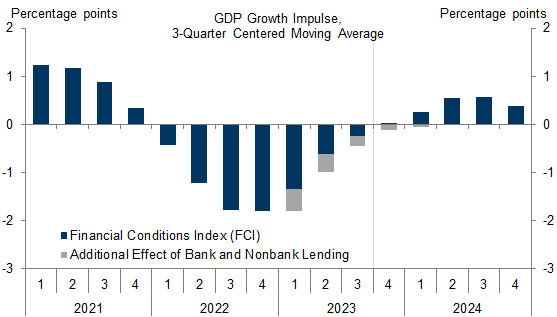

Exhibit 8: Financial and Credit Conditions Are Likely to Turn From a Drag on Growth in 2023 to a Boost in 2024, Supporting Our Above-Consensus Growth Forecast

Exhibit 9: Job Openings Remain High and Layoffs Remain Low

Exhibit 10: We Expect Job Gains to Gradually Slow to Roughly Their Breakeven Pace of About 100k per Month and the Unemployment Rate to Remain Stable at 3.6% in 2024

Exhibit 11: The Main Drivers of Strong Wage Growth, a Very Tight Labor Market and High Inflation Expectations, Have Now Normalized

Exhibit 12: Wage Growth Has Slowed from 5.5-6% to 4-4.5%, and Business Surveys Point to Further Deceleration Next Year Toward the 3.5% Rate Compatible with 2% Inflation

Exhibit 13: Core PCE Inflation Has Already Slowed Abruptly to a 2% Trend Pace and Now Appears Likely to Fall to the Low 2s on a Year-on-Year Basis Much Earlier Than We Previously Expected

Exhibit 14: We Are Confident That Further Disinflation Is in the Pipeline as Auto Inventories Recover and the Official Shelter Inflation Data Gradually Catch Down to Leading Indicators of Market Rent Inflation

Exhibit 15: We Expect Further Deceleration Across Most Categories to Bring Core PCE Inflation Down to 2.2% Year-on-Year by December 2024 and We See a Meaningful Risk That It Falls Below 2%

Exhibit 16: We Expect the FOMC to Deliver Three Consecutive Cuts in March, May, and June, Before Slowing to a Quarterly Pace in Q3 and Q4, for a Total of 5 Cuts in 2024

Exhibit 17: We Expect the FOMC to Slow the Pace of Balance Sheet Runoff in 2024Q4 and Stop Runoff in 2025Q1

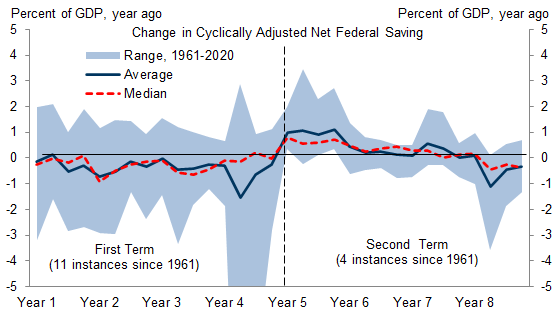

Exhibit 18: Fiscal Policy Has Become Somewhat More Expansionary in Presidential Election Years, on Average

Exhibit 19: We Do Not Expect Any Major New Fiscal Policy Changes Next Year, Though We See Some Downside Risk from Potential Automatic Spending Cuts If Congress Cannot Pass Full-Year Spending Bills

David Mericle

Alec Phillips

The US Economic and Financial Outlook

Investors should consider this report as only a single factor in making their investment decision. For Reg AC certification and other important disclosures, see the Disclosure Appendix, or go to www.gs.com/research/hedge.html.