We wish all of our readers a healthy, happy, and prosperous 2024. In our last Global Economics Analyst of 2023, we use 10 of our favorite charts to illustrate the key global themes that stood out this year and are likely to shape the year ahead.

The big surprises of 2023 were the sharp outperformance of global growth—which exceeded expectations by 1pp—and the rapid normalization of inflation in the second half of the year. The upside growth surprise reflected a fading drag from monetary policy tightening (as the lag from changes in financial conditions to growth is much shorter than commonly appreciated), as well as a recovery in income growth that kept consumer spending growth solid.

The progress on inflation despite firm growth underscored the unique nature of this cycle. Labor market rebalancing progressed smoothly as excess job openings unwound—despite unemployment rates remaining low—while labor supply beat expectations (both due to favorable hiring prospects and an immigration rebound). Combined with improving global supply conditions (which lowered core goods and headline inflation), this softened the upward pressure on wage growth, which should settle at a sustainable level in the year ahead.

As inflation nears the finish line, the bar to cut rates has fallen, and central banks should begin to normalize policy next year. As the “soft landing” plays out and economic conditions return to something resembling normal, we remain focused on longer-term drivers of the economic outlook, including the upside growth potential from generative AI.

Top 10 Charts of 2023

Exhibit 1: Global Growth Surprised Sharply to the Upside in 2023…

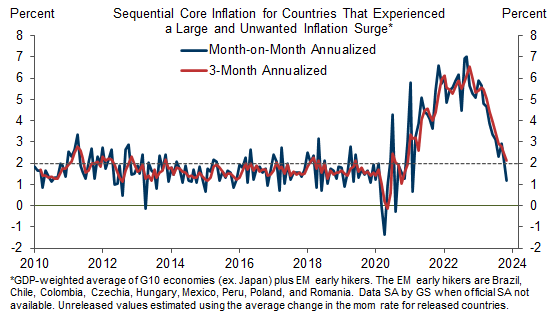

Exhibit 2: …Despite Which, Inflation Plummeted Across Countries That Experienced an Unwanted Surge.

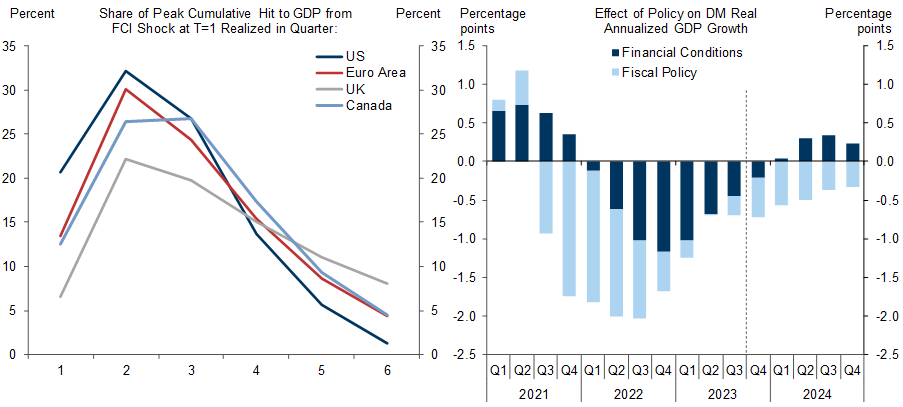

Exhibit 3: The Growth Drag From DM Monetary Policy Faded Faster Than Most Forecasters Expected (Although a Modest Fiscal Drag Remains in the Pipeline)…

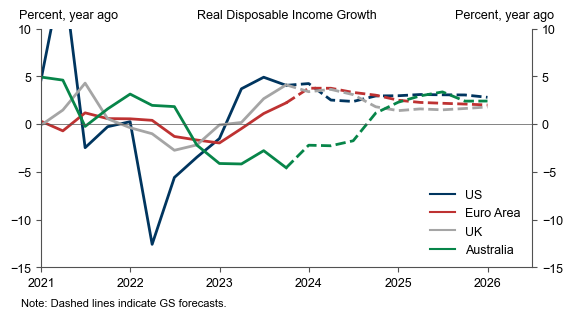

Exhibit 4: …While Real Incomes Improved Due to Solid Wage Gains and Cooling Inflation, a Trend Which Should Continue to Support Spending Next Year.

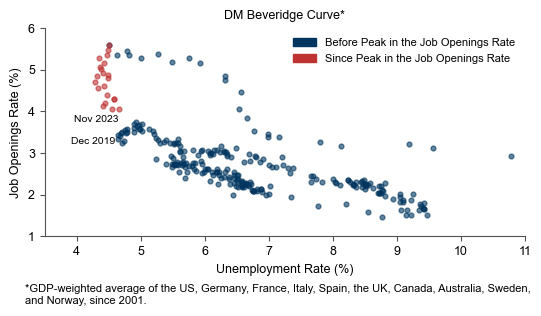

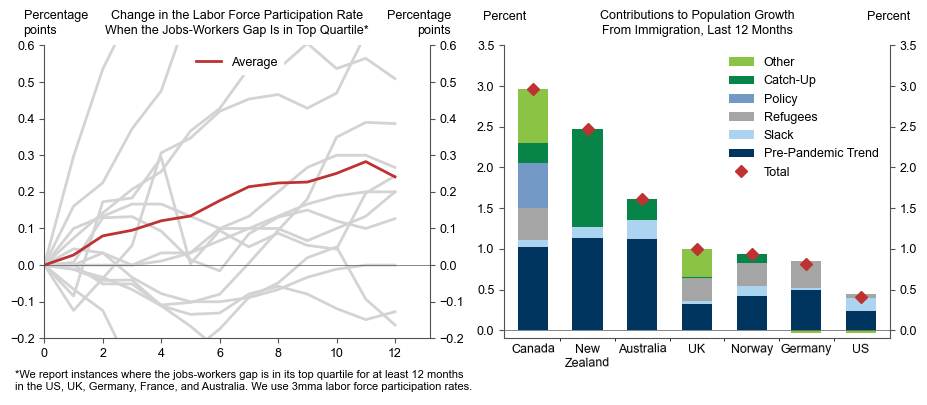

Exhibit 5: Despite Firmer-Than-Expected Growth, Labor Markets Continued to Rebalance Gently as Excess Job Openings Normalized While Unemployment Remained Low…

Exhibit 6: ...And Labor Supply Surprised to the Upside, Both Because Hiring Conditions Remained Favorable and Because Immigration Was Unusually Strong.

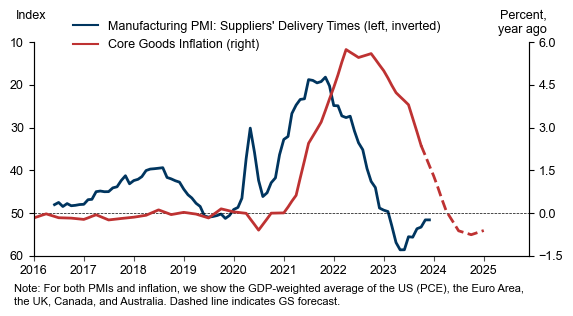

Exhibit 7: Meanwhile, Healing Supply Chains Played an Unusually Large Role in Disinflation…

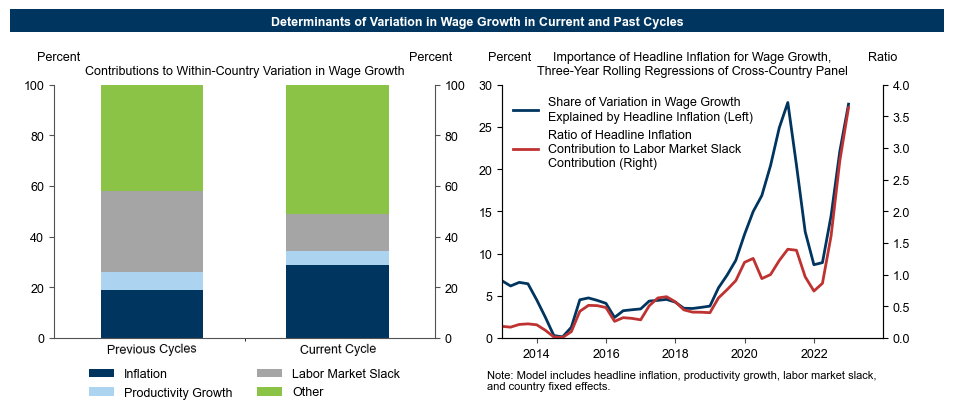

Exhibit 8: ...Especially Because Headline Inflation Disproportionately Drove the Wage Growth Overshoot.

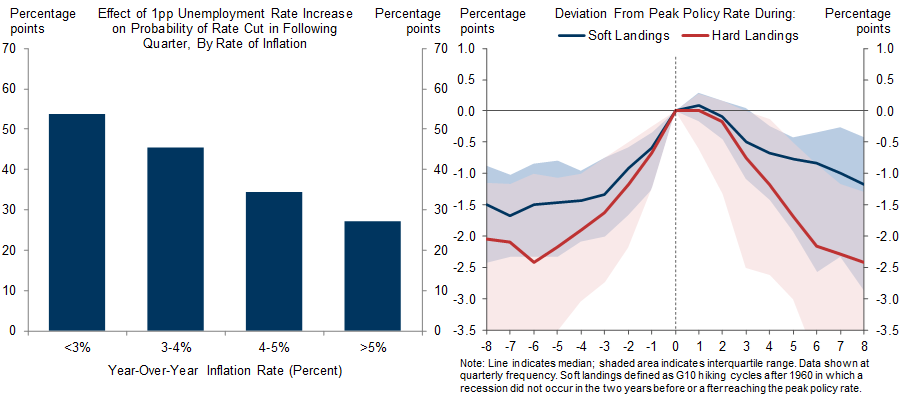

Exhibit 9: Next Year, Falling Inflation Should Greatly Lower the Bar for Central Banks to Cut Rates (Albeit to Higher Levels Than in Prior Cycles That Ended in Recession), Providing a Tailwind to Growth…

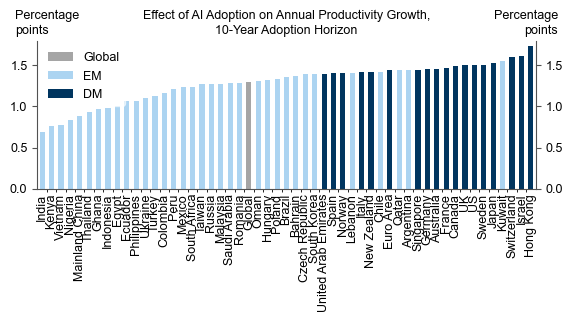

Exhibit 10: …While Over the Longer-Run, We Are Especially Optimistic About the Potential Growth Boost From Generative AI.

Global Economics Team

Bonus Charts

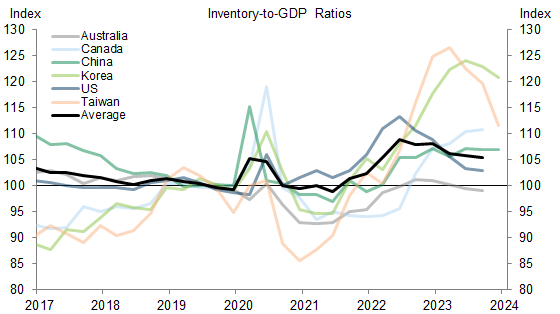

Exhibit 11: Next Year, We Expect a Rebound in DM Manufacturing, Partly Due to a Normalization in the Global Inventory Cycle.

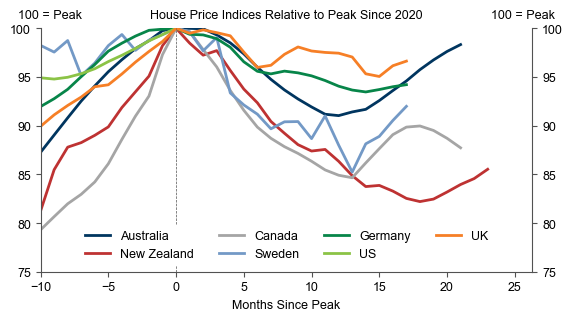

Exhibit 12: The Housing Market Should Also be a Source of Growth as Rates Fall, Especially After the Surprising Stabilization in Home Prices Earlier This Year.

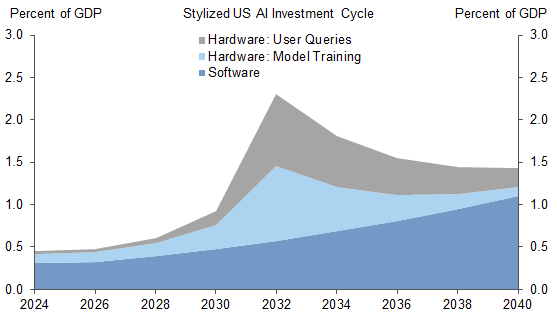

Exhibit 13: Even Before AI Starts to Impact Long-Term Growth, It Could Drive a Large Capital Investment Cycle, Particularly in the US.

Investors should consider this report as only a single factor in making their investment decision. For Reg AC certification and other important disclosures, see the Disclosure Appendix, or go to www.gs.com/research/hedge.html.