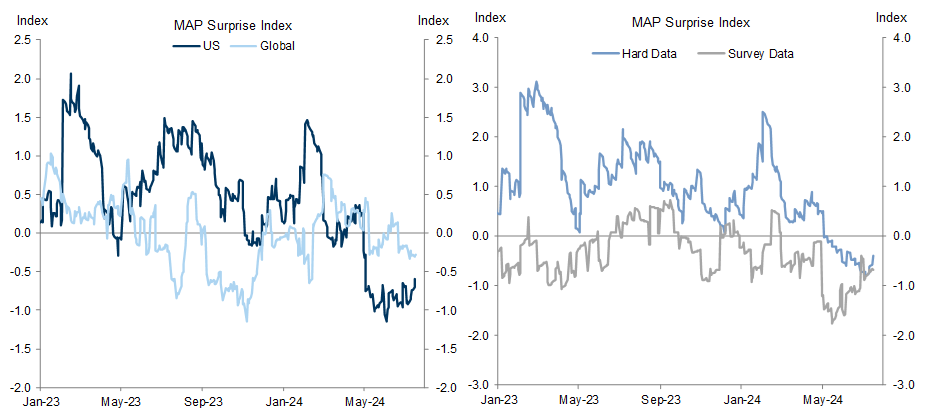

Until last week, US activity data had surprised mainly to the downside in recent months, fueling concern that the economy was slowing too quickly. But last week’s retail sales and industrial production reports brought welcome relief, and we are now tracking Q2 GDP growth at 2.3%. Our estimate implies that GDP grew at a 1.9% annualized pace in 2024H1 and domestic final sales grew at a 2.3% pace, easily beating gloomy consensus expectations at the start of the year and falling only a touch short of our own initial forecast.

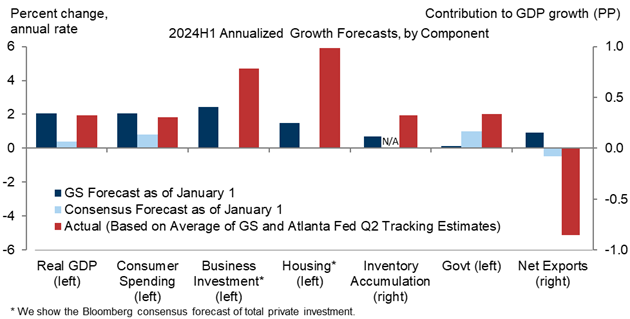

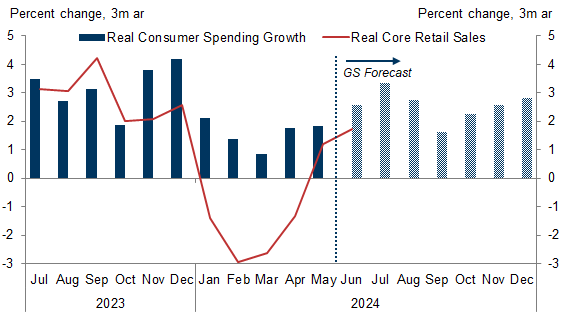

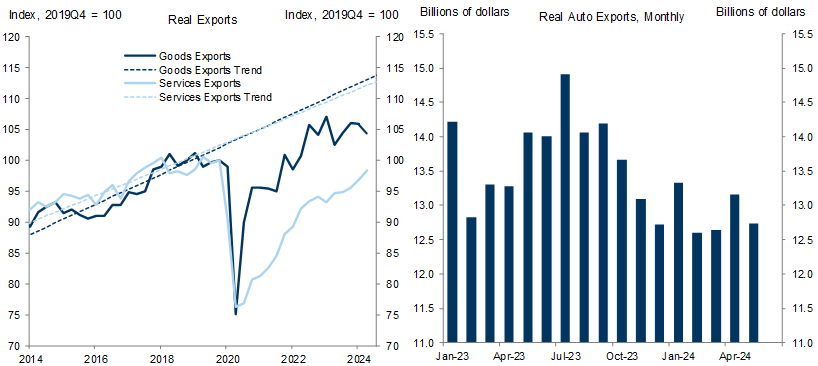

What surprised in the first half of 2024? Consumer spending has been on a rollercoaster, due in part to fluctuations in disposable income and seasonal adjustment challenges, but is now on track to grow about 1.8% in 2024H1, just a few tenths below our forecast at the start of the year. Investment—including residential, business, and inventory investment—surprised to the upside, though housing slowed in Q2 after a Q1 spike driven by a dip in mortgage rates. Net exports surprised to the downside, due in part to continued weakness in goods exports, which have stagnated at levels well below the pre-pandemic trend even as imports have recovered.

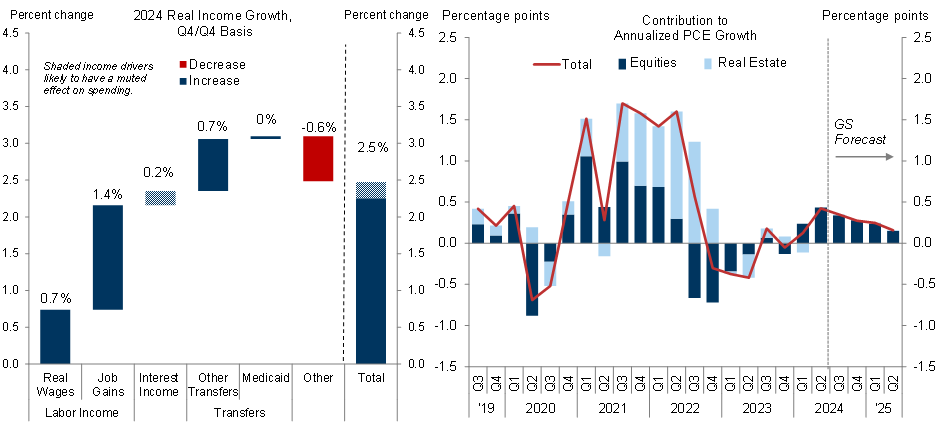

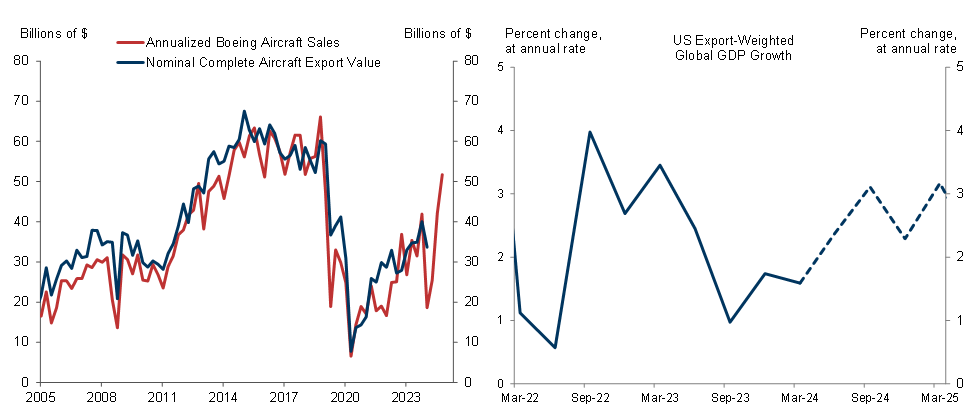

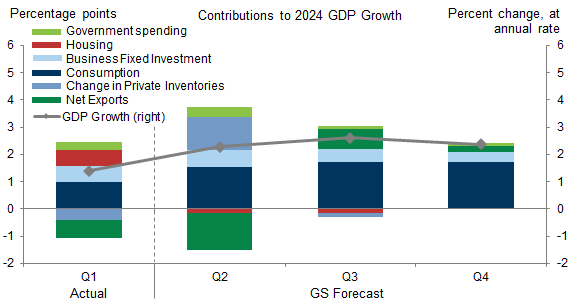

What is likely to change in the second half of 2024? We forecast 2.6% GDP growth in 2024Q3 and 2.4% in 2024Q4, for an average pace of 2.5% in 2024H2. Underpinning this is our expectation that consumer spending will continue to grow at a robust pace, supported by solid real income growth powered by a strong labor market as well as a positive wealth effect from recent increases in stock prices. Our slightly stronger growth forecast for Q3 reflects a rebound in the net trade contribution driven by softer imports and higher aircraft and other exports.

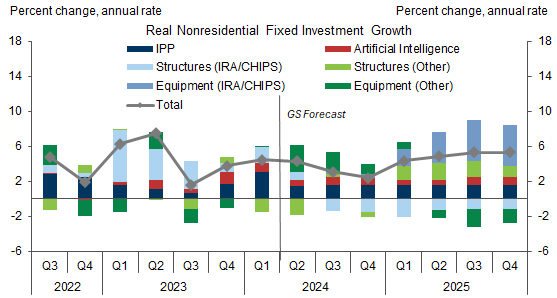

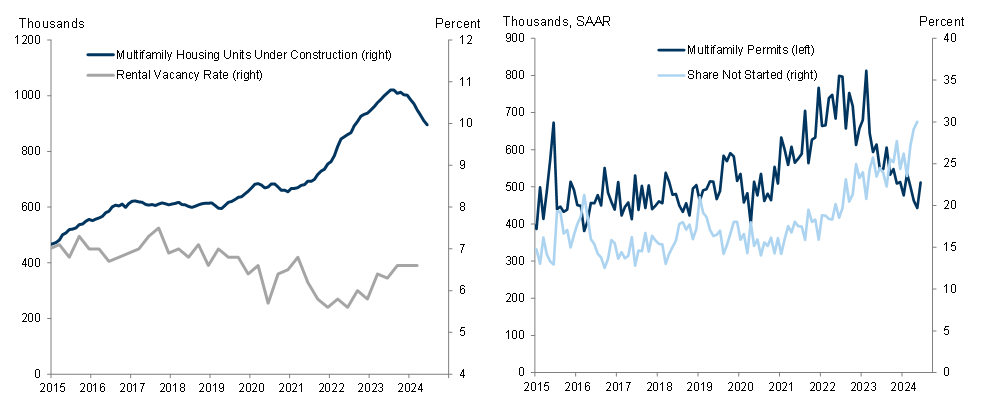

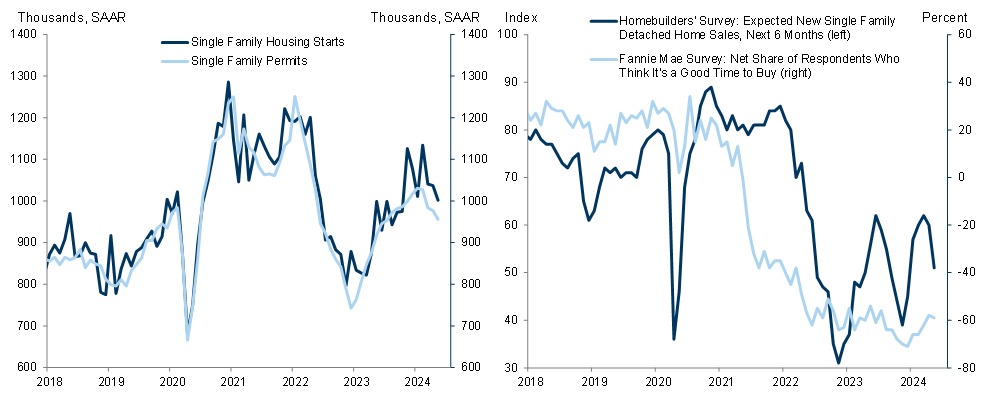

We see a more mixed picture and more uncertainty on the investment side in the second half. We expect business investment growth to slow to a 3% pace in 2024H2 because the factory-building boom catalyzed by CHIPS Act and Inflation Reduction Act subsidies has peaked, though investment in equipment for those factories and for AI should pick up. We expect residential investment to tick down slightly in 2024H2 because the surge in apartment construction in recent years has led builders to hit the brakes on multifamily construction, and while more single-family supply is still badly needed, building permits have dipped and recent survey data point to modest further weakness in the near term as potential buyers wait for rates to fall.

Our forecast of a growth pick-up from 1.9% in 2024H1 to 2.5% in 2024H2 would put 2024 Q4/Q4 GDP growth at 2.2%. While our forecast remains more optimistic than the consensus forecast of 1.6%, it is roughly in line with our estimate of short-term potential GDP growth, which is currently being boosted by additional labor supply from above-trend immigration.

A Mid-Year Temperature Check on Growth

Exhibit 1: Until Last Week, US Growth Data Had Surprised Primarily to the Downside in Recent Months, Fueling Concern That the Economy Might Be Slowing Too Quickly

What surprised in the first half of 2024?

Exhibit 2: Overall GDP Growth Appears to Have Been Close to Our Expectations in 2024H1, with Upside Surprises on Investment Offsetting a Downside Surprise on Net Exports

Exhibit 3: Consumer Spending Was Volatile in 2024H1, Possibly Due to Fluctuations in Disposable Income and Seasonal Adjustment Challenges, But It Picked Back Up in June

Exhibit 4: Foreign Trade Was the Weak Spot in the First Half of 2024, in Part Because Exports Continued to Stagnate at a Level Well Below the Pre-Pandemic Trend and Auto Exports in Particular Disappointed

A Slightly Stronger Second Half

Exhibit 5: Solid Real Income Growth and a Positive Wealth Effect Should Continue to Support Consumption Growth

Exhibit 6: We Expect Investment Growth to Slow a Bit in 2024H2 Because the Factory-Building Boom Has Likely Peaked, but Investment in Equipment for Those Factories and in AI Should Eventually Take Its Place

Exhibit 7: The Surge in Apartment Construction in Recent Years Has Rebalanced the Rental Market and Softened Rent Growth, Leading Builders to Hit the Brakes on Multifamily Construction

Exhibit 8: The Single-Family Part of the Housing Market Remains Historically Tight and Demand for New Construction Remains Strong, Though Recent Data Point to Some Softening as Buyers Await Lower Rates

Exhibit 9: Net Exports Should Pick up in 2024H2 as Aircraft Exports Rebound and Demand Growth Picks Up in Key US Export Markets

Above Consensus, but in Line with Short-Term Potential Growth

Exhibit 10: We Expect GDP Growth to Pick Up from 1.9% in 2024H1 to 2.5% in 2024H2, Implying a 2.2% Q4/Q4 Pace That Is Above Consensus but in Line with Short-Term Potential Growth Boosted by Immigration

David Mericle

Jessica Rindels

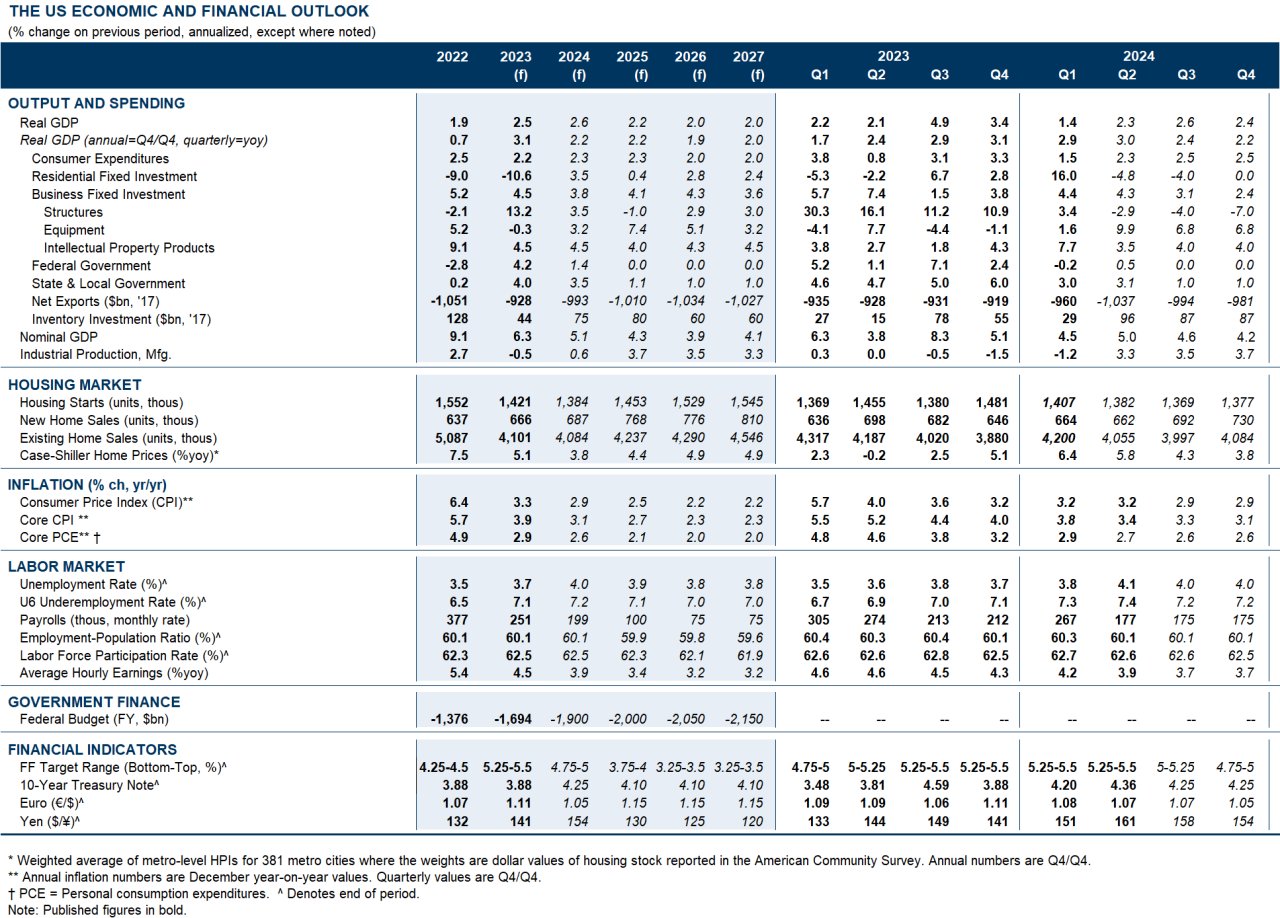

The US Economic and Financial Outlook

Investors should consider this report as only a single factor in making their investment decision. For Reg AC certification and other important disclosures, see the Disclosure Appendix, or go to www.gs.com/research/hedge.html.