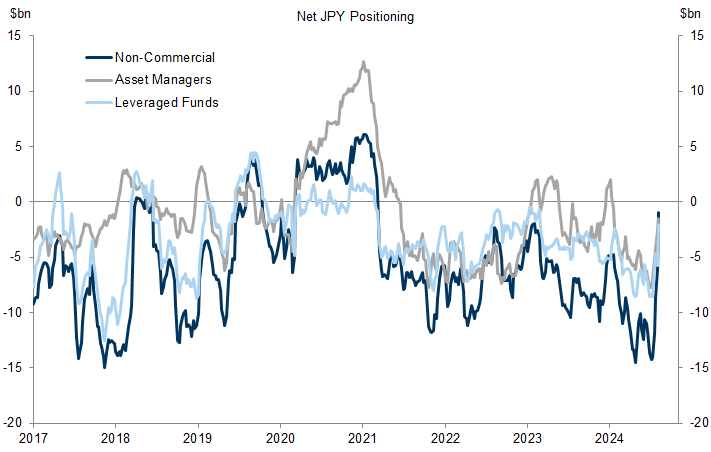

The recent sharp appreciation of the Yen coinciding with a spike in cross-asset volatility has heightened the focus on the “Yen carry trade” and the broader financial market implications from further unwinds. Limited data availability presents a challenge to confidently assessing “how much is left,” but substantial holdings among longer-term investors leave room to run. That said, subsequent unwinds should be broadly slower-moving as, based on futures positioning alone, roughly 90% of speculative shorts appears already undone.

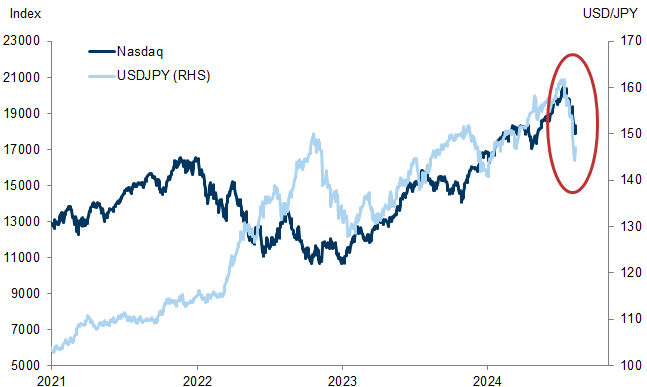

Despite the sharp unwinds, we believe that coincidental timing of disappointing earnings and a “perfect storm” of JPY-positive factors—including softer macro data, Yen supportive intervention, and a surprise BoJ hike—best explains the unusually tight correlation between the sell-offs in USD/JPY and the Nasdaq over the past few weeks, rather than deep leverage from the carry trade.

Regardless, if Japan sees a renewed sharp tightening in financial conditions, it could complicate the domestic inflation outlook and thus the BoJ’s plan to continue hiking rates—but not the Fed’s readiness to cut. Deputy Governor Uchida’s remarks last week demonstrate the BoJ is willing to adjust policy in response to market volatility to avoid rapid and significant Yen appreciation that would jeopardize progress towards their inflation goal.

Though we have not flipped to being Yen bulls, the carry unwinds “still left” will probably reinforce any periods of Yen appreciation. Moreover, the marginally higher probability of a US recession (our economists now have it at 25%) increases the attractiveness of the Yen as a portfolio hedge. For that reason, we prefer looking for tactical opportunities in other crosses, including short EUR/USD.

The Yen Carry Trade—A Roadblock to BoJ Hikes, Not Fed Cuts

Why the Yen Carry Seems Scary

Exhibit 1: The sell-offs in the Nasdaq and USD/JPY exhibited an unusually tight correlation last month

Estimating the Carry Trade

Shorter-term positioning

Exhibit 2: The CFTC speculative futures positioning data suggest that roughly 90% of the carry trade unwind has already occurred

Longer-term positioning

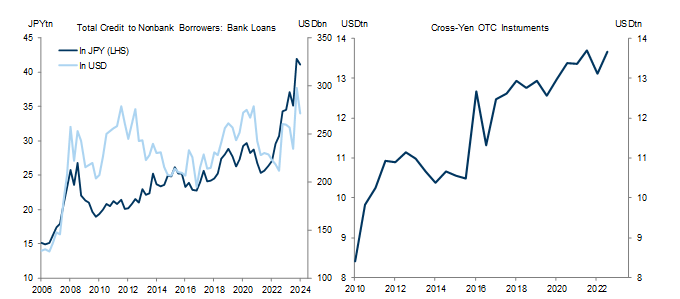

Exhibit 3: On-balance sheet credit to borrowers of Yen outside of Japan increased over 60% from Q4 2015 (pre-NIRP) to Q1 2024, reaching ¥41tn (or $270bn), and that reflects only a small share of off-balance sheet activities

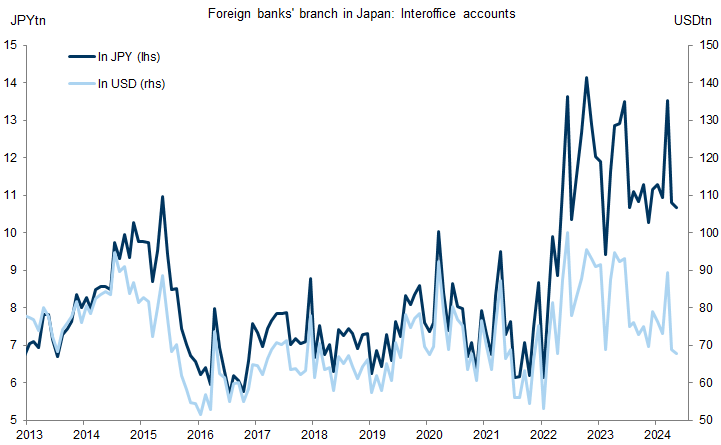

Exhibit 4: Transfers from foreign bank branches in Japan have generally picked up in recent years

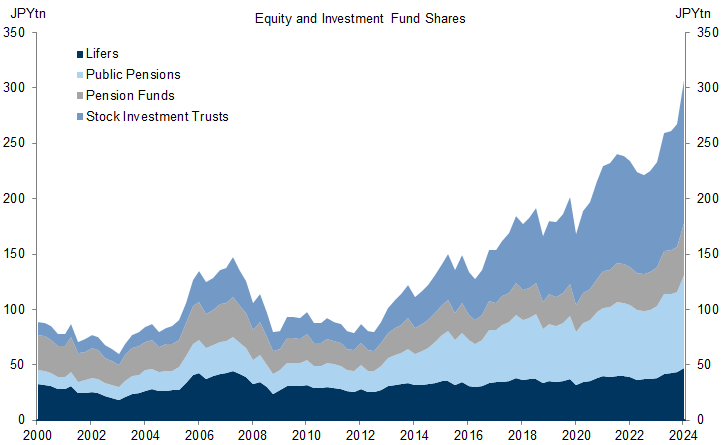

Exhibit 5: Holdings among key Japanese investors who typically leave at least some foreign assets unhedged stood at roughly ¥300tn (or nearly $2tn) as of Q1 2024

Our Outlook for the Yen

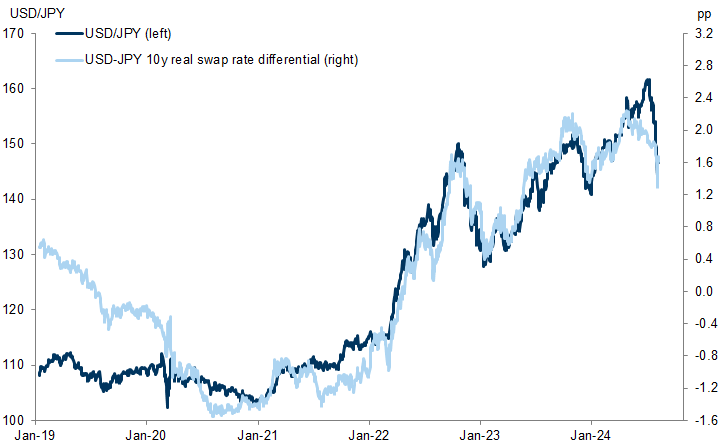

Exhibit 6: USD/JPY is once again trading more closely with fundamentals

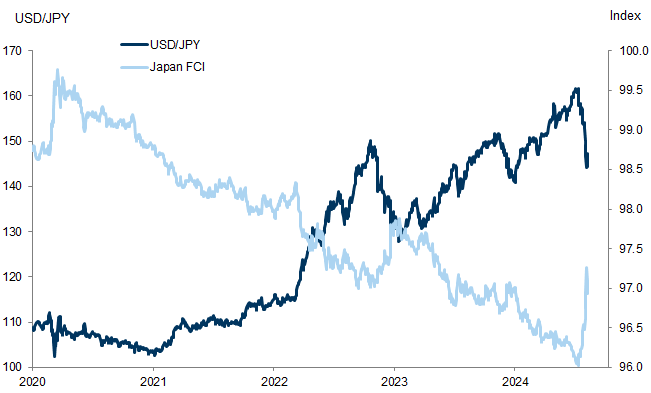

Exhibit 7: A renewed sharp tightening in Japan’s financial conditions could complicate the the BoJ’s plan to continue hiking rates

- 1 ^ We focus on equities since unhedged bond holdings should be less of a concern as the gains from lower US yields offset the FX-related losses.

Investors should consider this report as only a single factor in making their investment decision. For Reg AC certification and other important disclosures, see the Disclosure Appendix, or go to www.gs.com/research/hedge.html.