Several central banks—including the BoC, RBNZ, Riksbank, and the Fed—have started cutting sequentially, and we expect several others (including the ECB and BoE) to do so soon. In this comment we review the data dashboards that led central banks to pivot to sequential cuts so far and discuss the implications for central banks that have not.

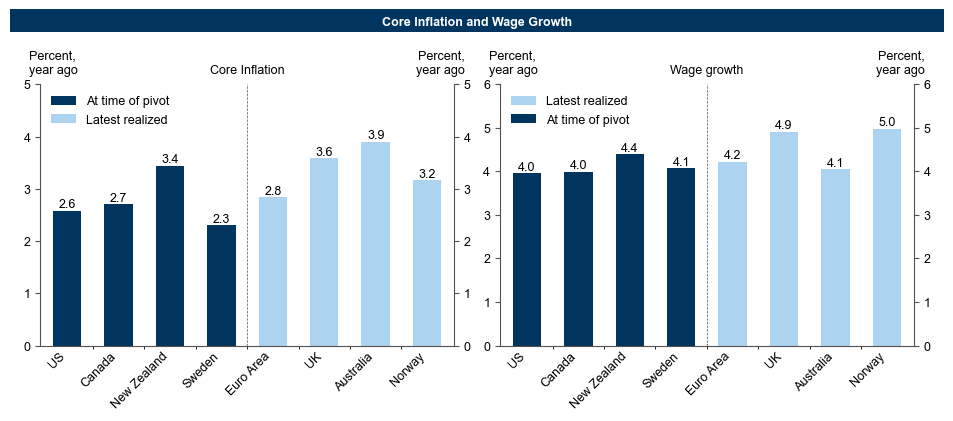

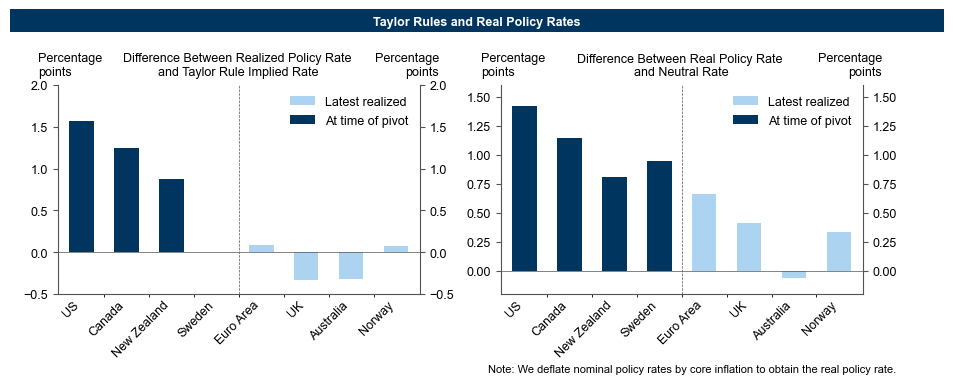

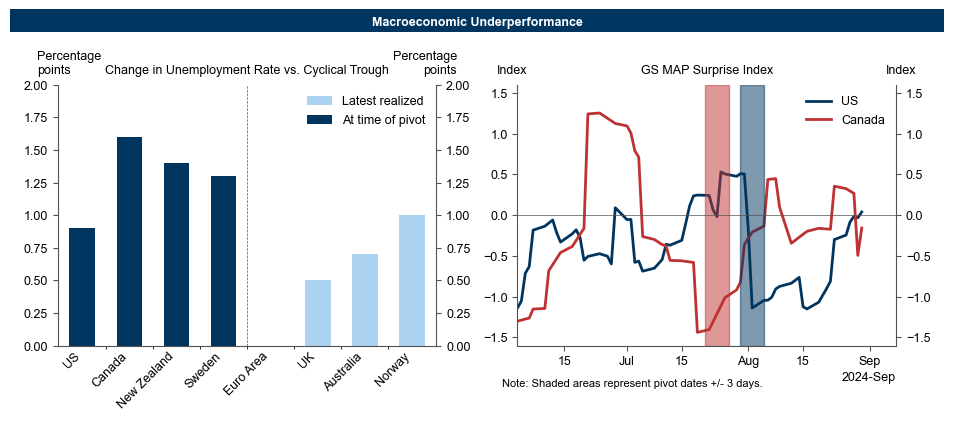

Data dashboards around pivots toward sequential cuts show three patterns. First, countries so far have only pivoted following substantial progress on core inflation and wage growth. Second, countries that have pivoted generally had larger policy rate overshoots relative to Taylor rule implied levels and higher real interest rates. Third, countries that have pivoted experienced a marked rise in unemployment and/or a downside growth surprise that raised concerns around the GDP outlook.

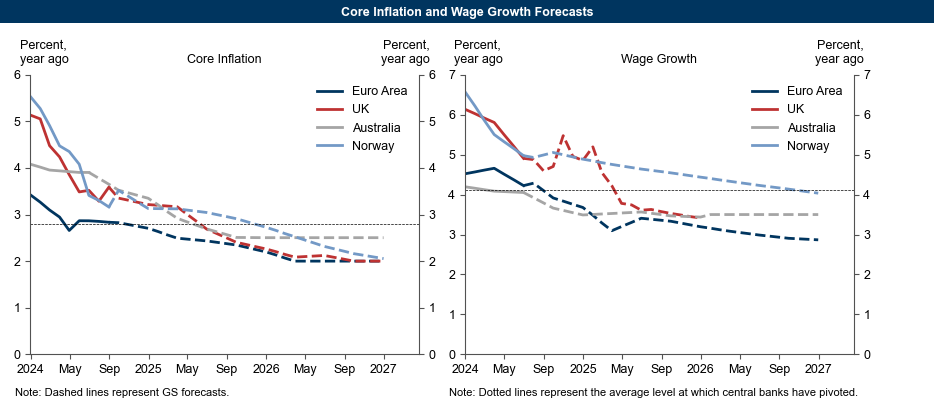

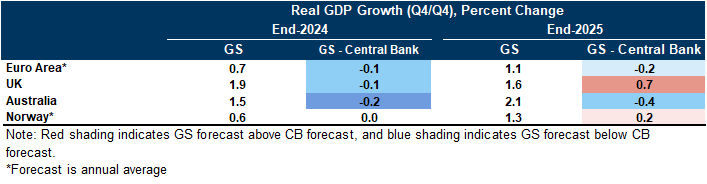

Under our forecasts, the Euro area will reach the average levels of core inflation and wage growth that permitted pivots in 2024Q4, followed by the UK and Australia in 2025H1. Moreover, our GDP forecasts are bearish relative to central bank expectations across all three economies. These patterns support our forecasts for a shift to sequential cuts for both the ECB (starting in December) and BoE (November). And while we continue to expect quarterly cuts in Australia and Norway, we expect that progress on inflation will keep the door open to an acceleration in rate cuts in the event of even moderate downside growth surprises.

What Prompts DM Pivots to Sequential Cuts?

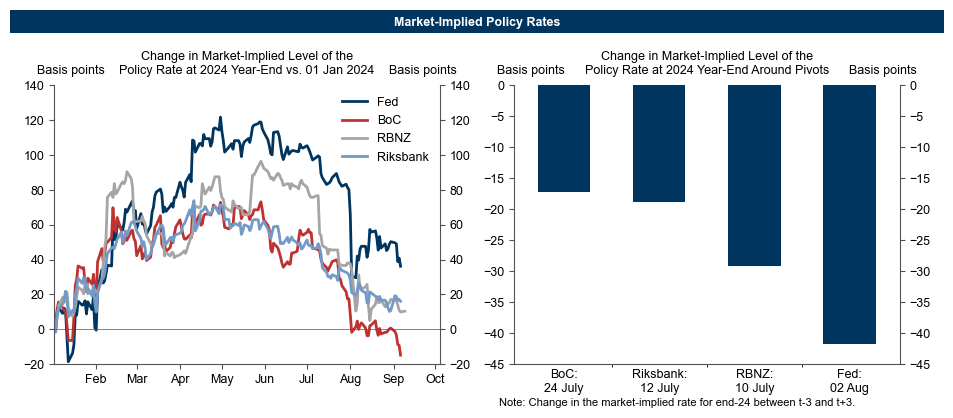

Exhibit 1: End-2024 Market Pricing Shifted Down by 27bp Around Central Bank Pivots to Accelerated Cuts

Exhibit 2: Pivots Toward Sequential Cuts Occurred Following Significant Inflation and Wage Growth Progress

Exhibit 3: Pivots Toward Sequential Cuts Occurred When Taylor Rule Implied and Real Rates Were Very Elevated

Exhibit 4: Deterioration in Unemployment and Activity Indicators Prompted Pivots Toward Sequential Cuts

Exhibit 5: We Expect Core Inflation and Wage Growth to Reach the Levels Consistent with Observed Pivots in 2024Q4 in the Euro Area and 2025H1 in the UK and Australia

Exhibit 6: Our GDP Forecasts in Economies that Have Not Shifted Toward Sequential Cuts Are Somewhat Bearish Relative to Central Bank Expectations

Joseph Briggs

Megan Peters

- 1 ^ Since the RBNZ targets inflation of 1-3%, it may have a slightly greater tolerance for inflation above 3% than central banks that target inflation of 2% without an explicit range.

Investors should consider this report as only a single factor in making their investment decision. For Reg AC certification and other important disclosures, see the Disclosure Appendix, or go to www.gs.com/research/hedge.html.