A sharp rise in long-term interest rates combined with widening deficits and heightened fiscal discord in Congress have renewed questions about the sustainability of rising government interest costs.

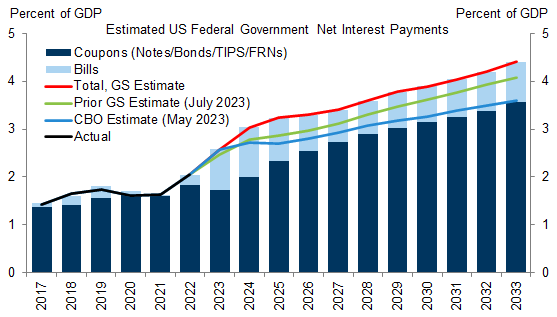

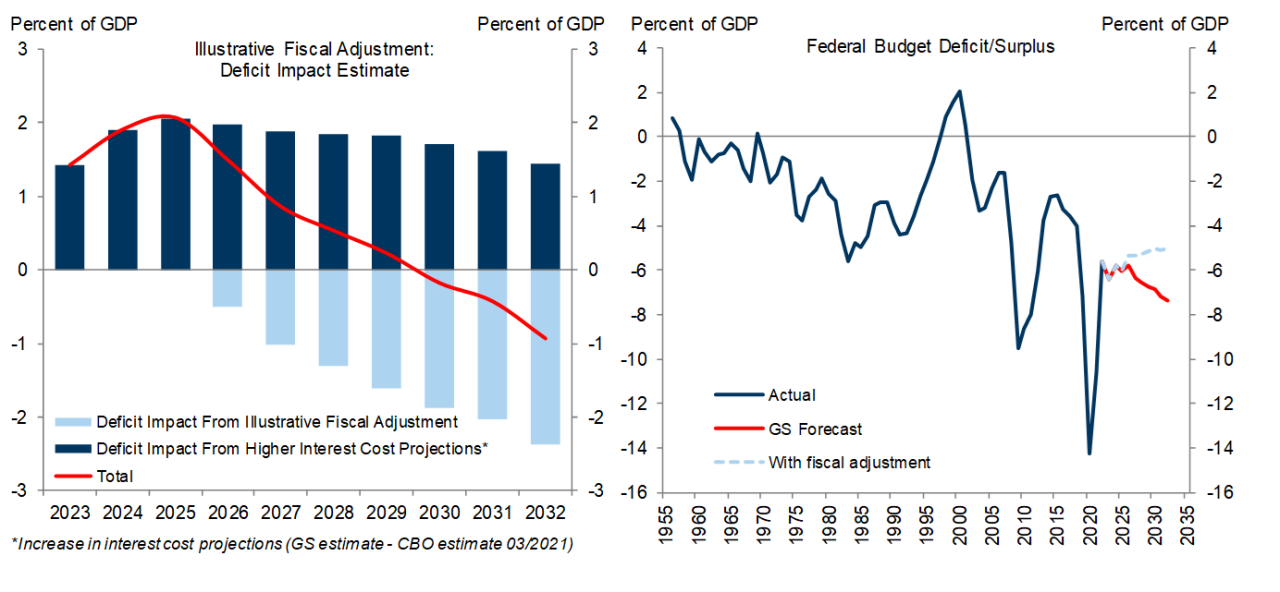

We project federal interest expense will rise from 2% of GDP in 2022 to 3% in 2024 and 4% by 2030, surpassing the early 1990s peak by 2025. On average over the next decade, higher interest expense is likely to add an additional 0.3% of GDP to the annual deficit compared to our July projections. In the near term, we have raised our deficit estimates for FY2024 by $50bn to $1.7tn (6.0% of GDP) and FY2025 by $100bn to $1.9tn (6.5% of GDP).

When interest expense rose sharply in the 1980s, fiscal policymakers reacted by shrinking the primary (ex-interest) deficit. The largest fiscal adjustment from that period, enacted in 1993, would be sufficient if enacted now to offset the additional interest expense we project (relative to 2021) after 5 years. However, this looks unlikely anytime soon given congressional gridlock, a lack of political attention to deficit reduction, and the upcoming 2024 election.

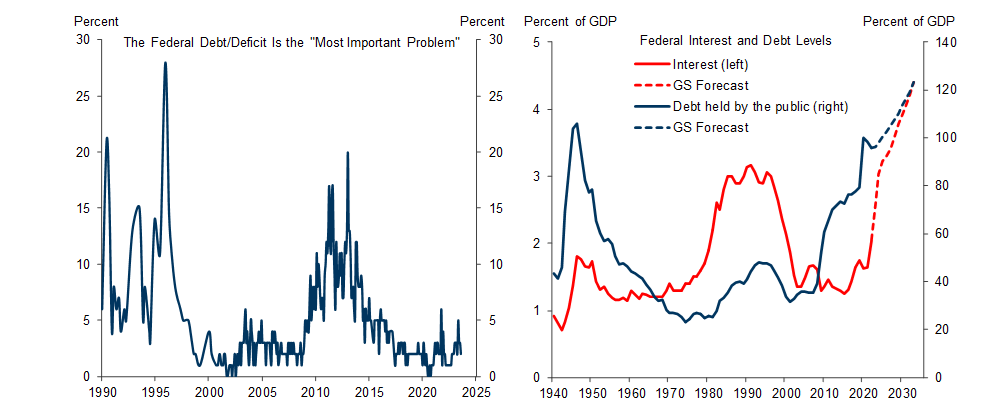

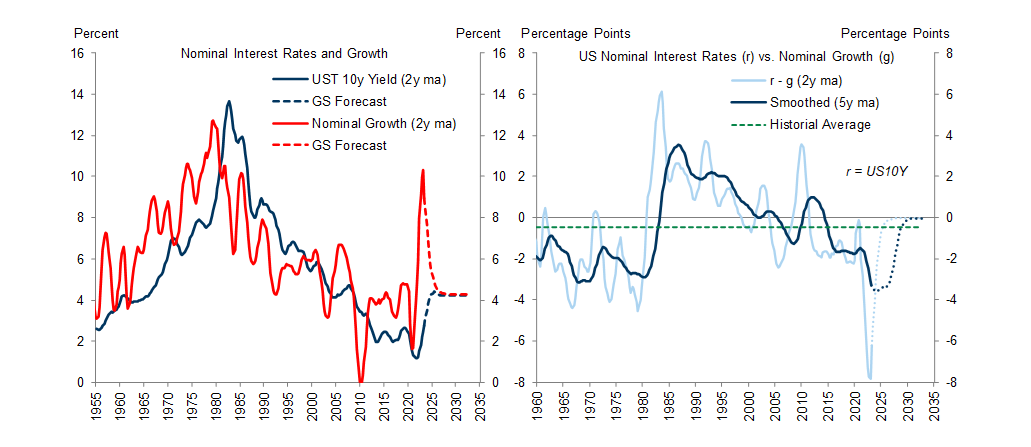

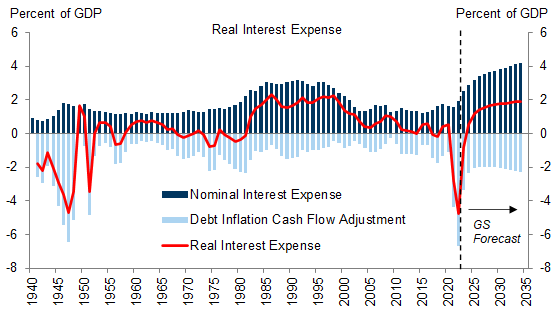

While higher interest expense will add to the deficit, the impact on the debt-to-GDP ratio should be much smaller. The average interest rate on federal debt is likely to remain at or below the rate of nominal GDP growth for the next decade, and this relationship is likely to be more benign than the historical average over the next five years. A larger debt stock but a lower interest rate-growth differential implies that real interest expense as a percent of GDP—the cost of stabilizing the debt-to-GDP ratio—will be comparable to the level in the late 1980s and 1990s.

Ultimately, the main challenge facing fiscal policy remains the large structural primary deficit, not interest expense. We estimate that debt as a share of GDP will rise from 96% to 123% over the next decade, driven primarily by a chronic primary deficit of around 3%. Although nominal GDP growth is likely to mostly offset the effect of higher interest costs on the debt-to-GDP ratio, the structural deficit will continue to add to public debt for the foreseeable future.

Interest Expense: A Bigger Impact on Deficits than Debt

Rising Interest Costs

Exhibit 1: We Are Raising Our Interest Cost Projections on The Back of Higher Rates

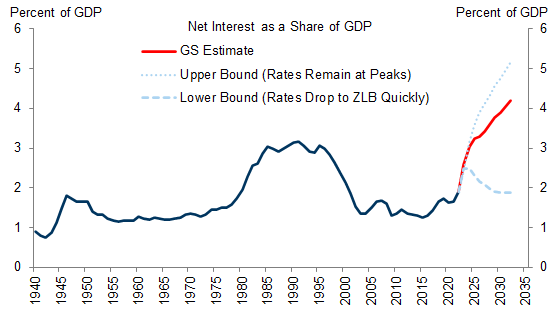

Exhibit 2: We Estimate Interest Costs as a Share of GDP Will Reach a New Peak by 2025

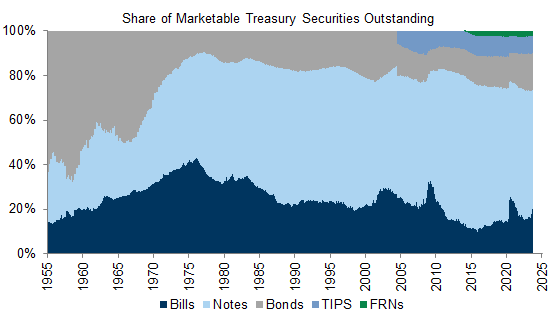

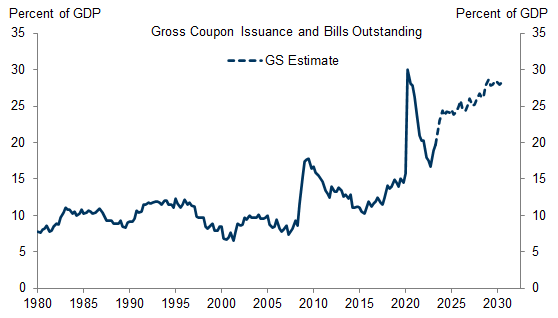

Exhibit 3: The Share of Bills Outstanding Has Risen 5pp This Year to Around 20%, Approaching the Upper Bound of Treasury’s “Recommended Range” of 15-20%

Higher Interest Costs Could Eventually Lead to Fiscal Tightening

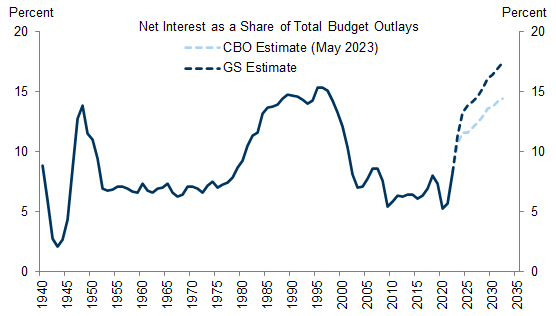

Exhibit 4: We Estimate Interest Costs as a Share of Total Spending Will Reach a New Peak by 2029

Exhibit 5: A Repeat of the Largest Fiscal Adjustment in US History Would Take Around Five Years to Make Up for Changes in Interest Projections Relative to 2021

Exhibit 6: The Public Does Not See the Deficit as a Major Concern Right Now, but Interest Costs and Debt Levels Should Soon Peak Together for the First Time

A Strong Nominal Growth Cushion

Exhibit 7: The Interest Rate-Growth Differential Remains Relatively Benign

Exhibit 8: A Larger Debt Stock but a Lower r-g Implies That Real Interest Expense as a Percent of GDP—the Cost of Stabilizing the Debt-to-GDP Ratio—Will Be Comparable to the Level in the Late 1980s and 1990s

Exhibit 9: Treasury Will Have an Unusually High Amount of Gross Issuance, Which Increases Rollover Risk and Sensitivity to Future Interest Rate Changes

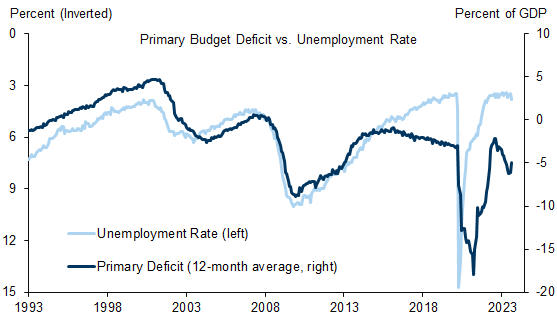

Exhibit 10: The Federal Government Is Running a Large Primary Deficit Despite Very Low Unemployment

Tim Krupa

Alec Phillips

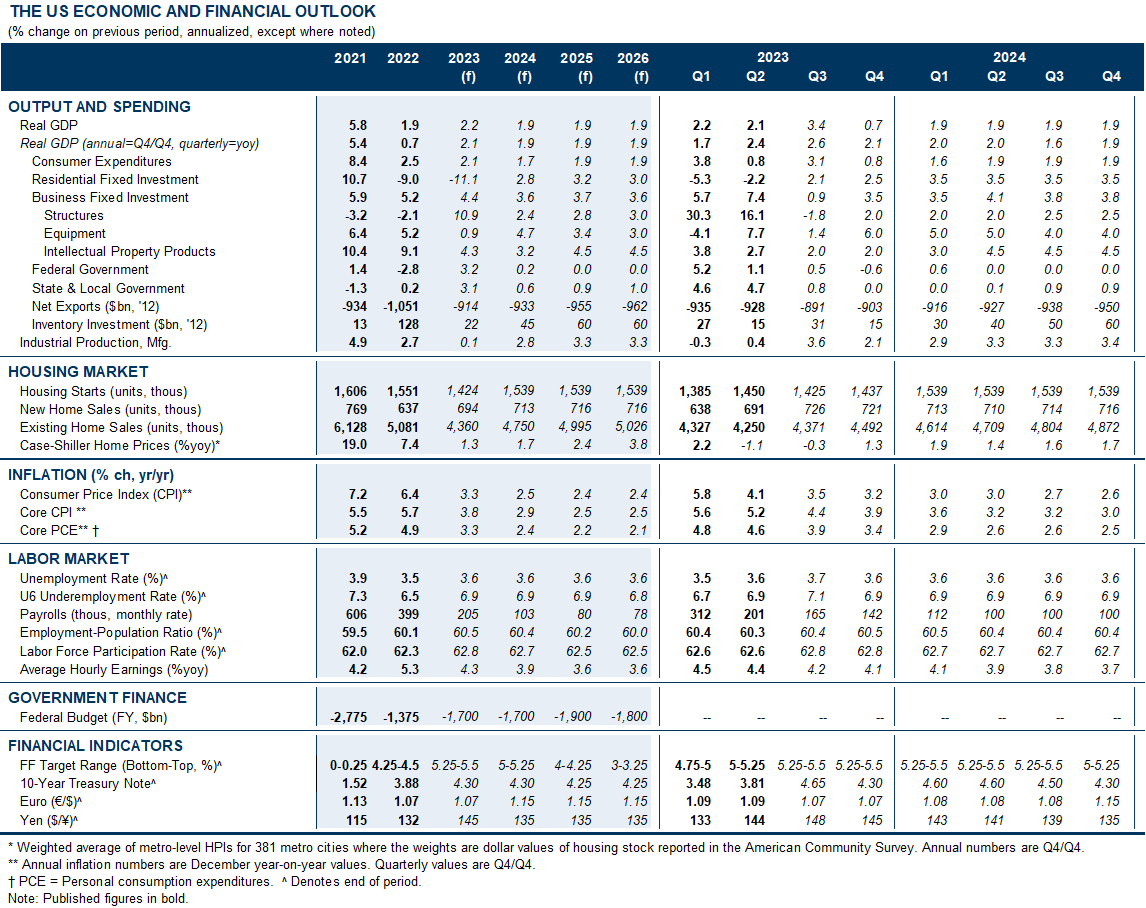

The US Economic and Financial Outlook

- 1 ^ For more details, see “Select Portfolio Metrics” of the Treasury Presentation to TBAC here.

Investors should consider this report as only a single factor in making their investment decision. For Reg AC certification and other important disclosures, see the Disclosure Appendix, or go to www.gs.com/research/hedge.html.