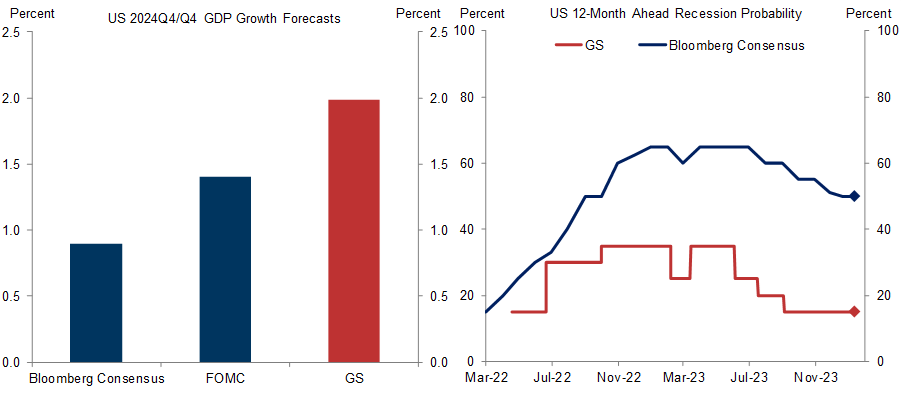

We expect much stronger GDP growth in 2024 than consensus and see a much lower risk of recession. What are other forecasters worried about that we aren’t? This Analyst looks at 10 risks for 2024 that are often highlighted by other forecasters and explains why we worry less.

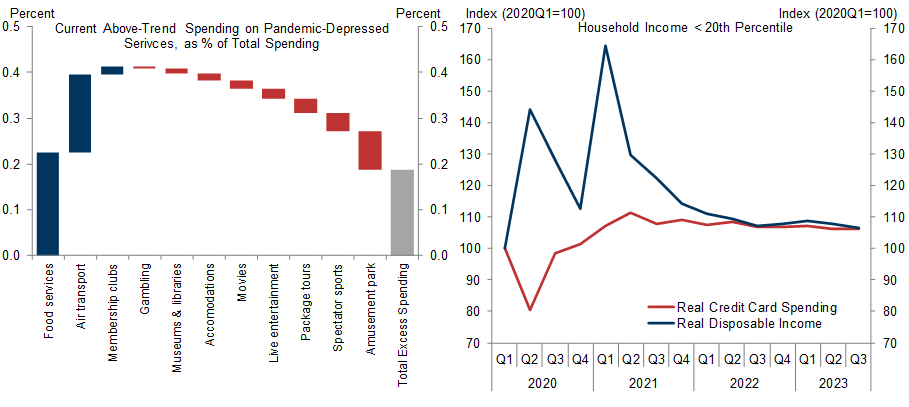

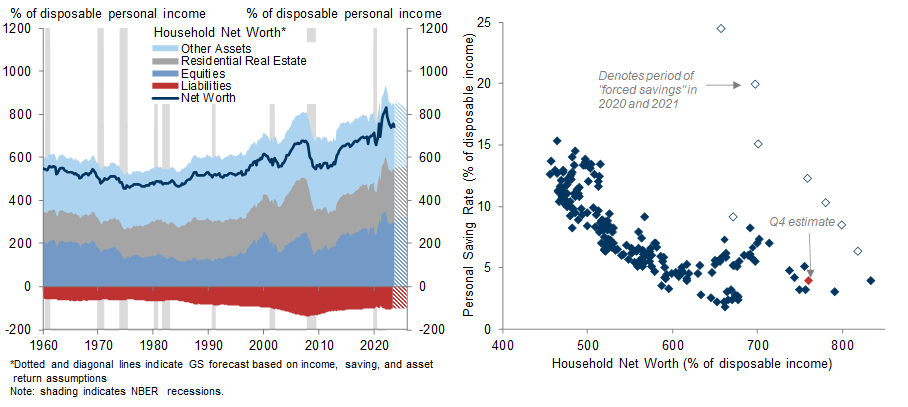

Risk 1: A consumer slowdown looks unlikely because real income should grow about 3% and household balance sheets are strong. Current spending patterns do not appear unsustainable and the saving rate does not look puzzlingly low at a time when household wealth is very high.

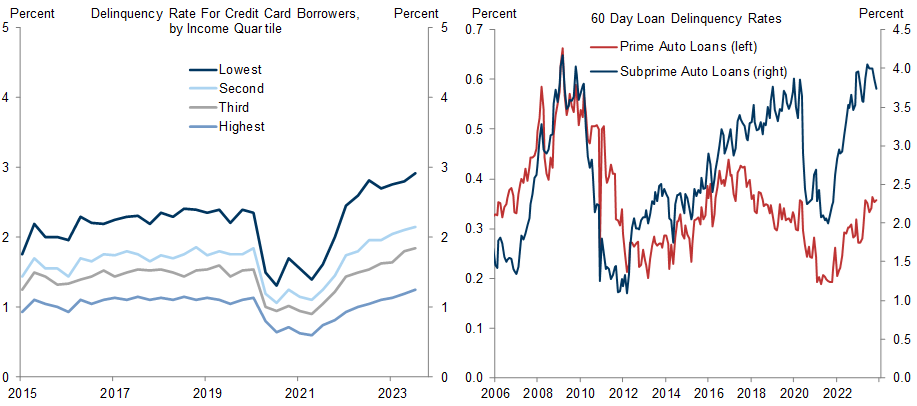

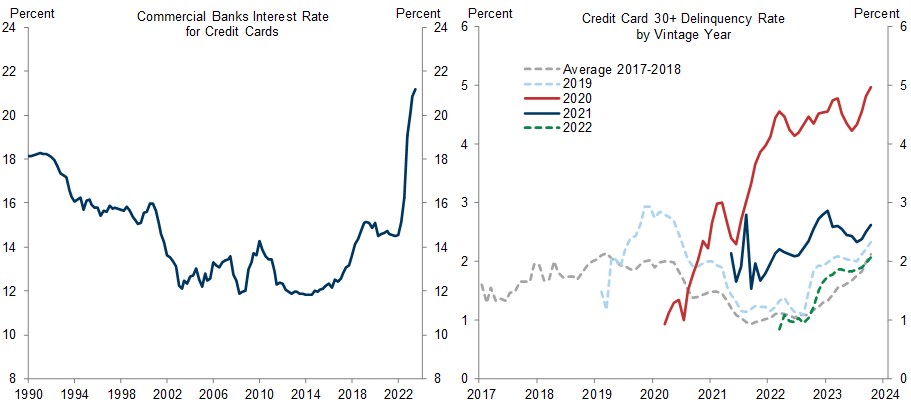

Risk 2: Rising consumer delinquency and default rates mostly reflect normalization from very low levels in recent years, higher interest rates, and riskier lending, not poor household finances.

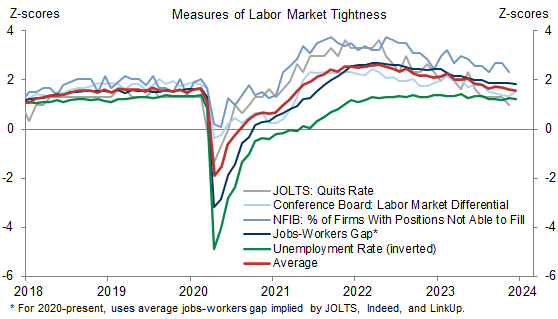

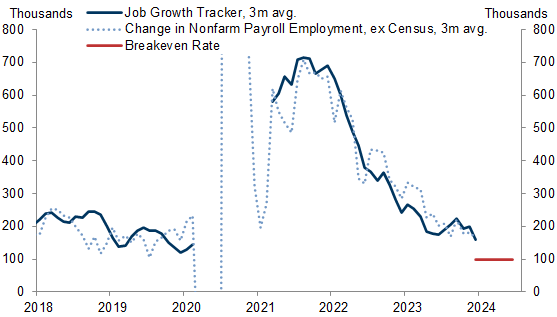

Risk 3: A sharper deterioration in the labor market is unlikely with job openings still high and the layoff rate still very low. While a few recent data points have been weaker, more statistically reliable signals such as trend payroll growth and our composite job growth tracker remain strong.

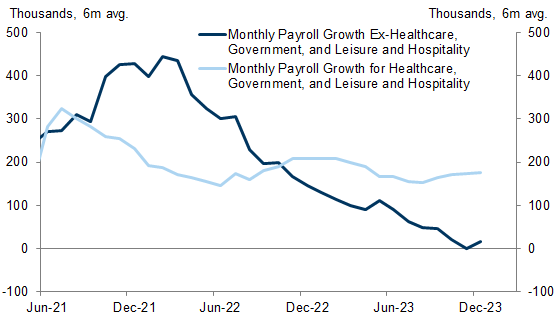

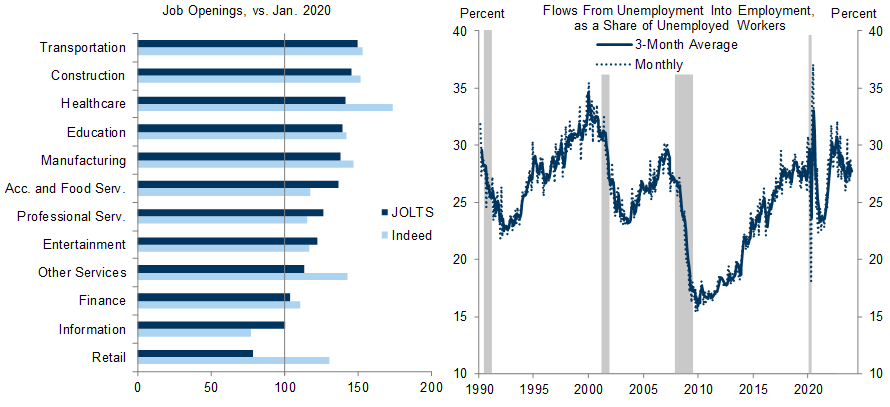

Risk 4: The narrow breadth of job growth is not indicative of either a mismatch problem or weak labor demand in most sectors—job openings are high in nearly all sectors—and it should normalize as hiring rebounds in industries that are particularly sensitive to financial conditions.

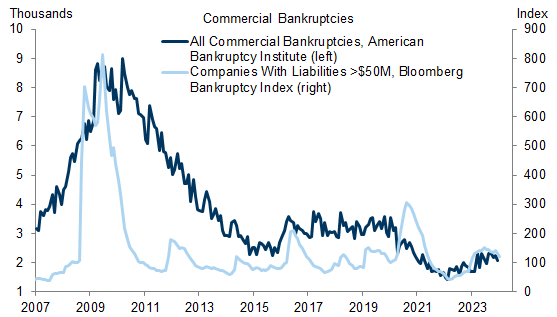

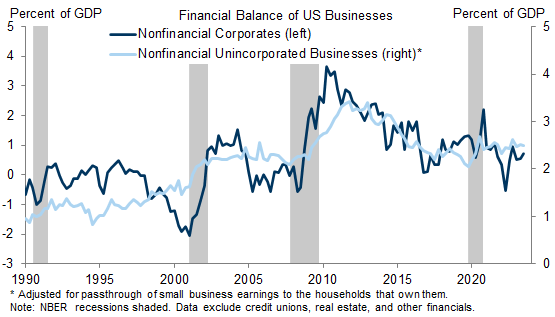

Risk 5: Rising corporate bankruptcies look less ominous and indeed quite low when compared to pre-pandemic levels. More broadly, the business sector remains on a solid financial footing.

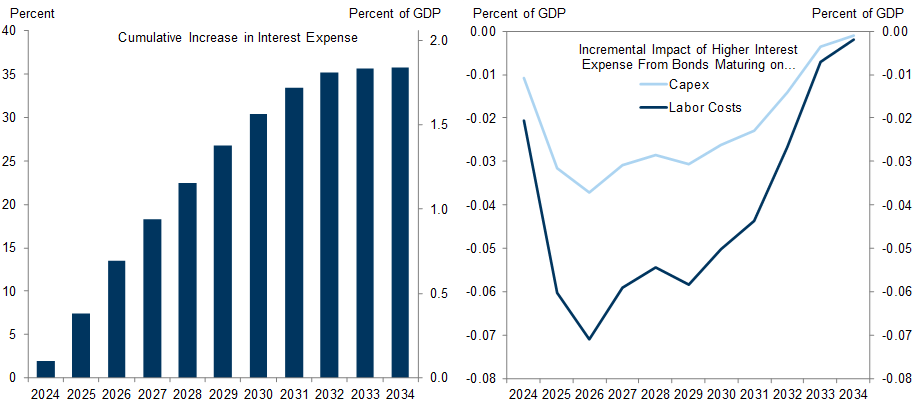

Risk 6: The corporate debt maturity wall will raise corporate interest expense with a longer delay than usual, but the resulting hit to capital spending and hiring is likely to be quite modest.

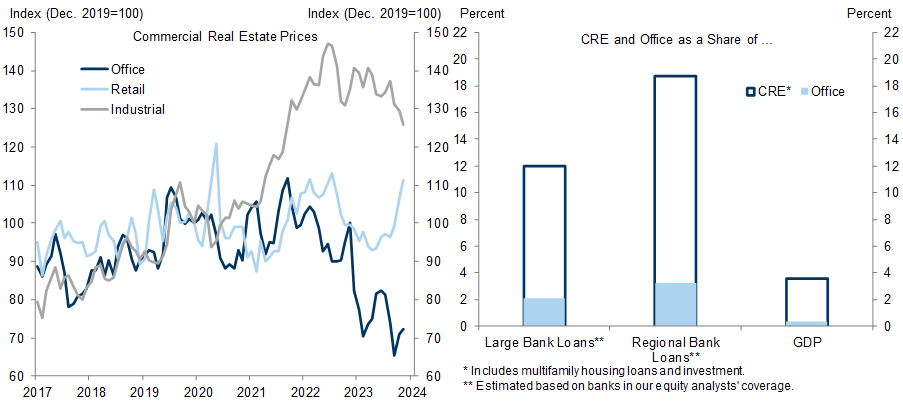

Risk 7: Commercial real estate broadly is not a problem, office specifically is. But office loans account for only 2-3% of banks’ loan portfolios, small enough for banks to manage the hit.

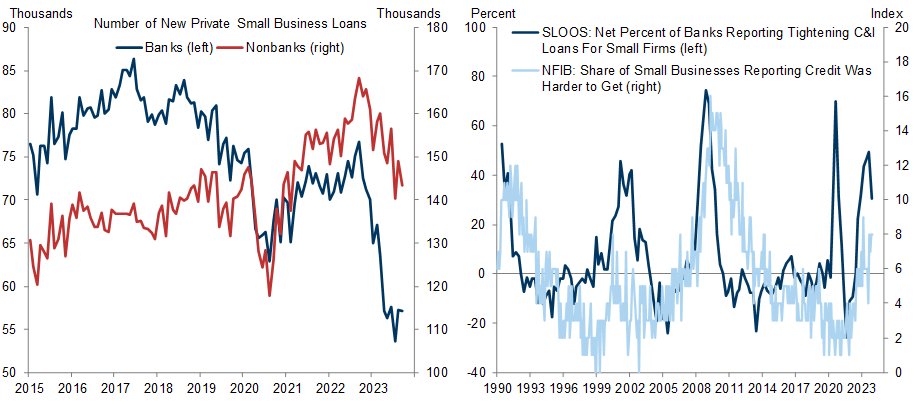

Risk 8: A bank credit crunch was a valid concern last spring, but the banking stress has not been as serious as feared, non-bank lenders cut back on lending by less, small businesses have not reported a severe lack of access to credit, and financial conditions have now eased meaningfully.

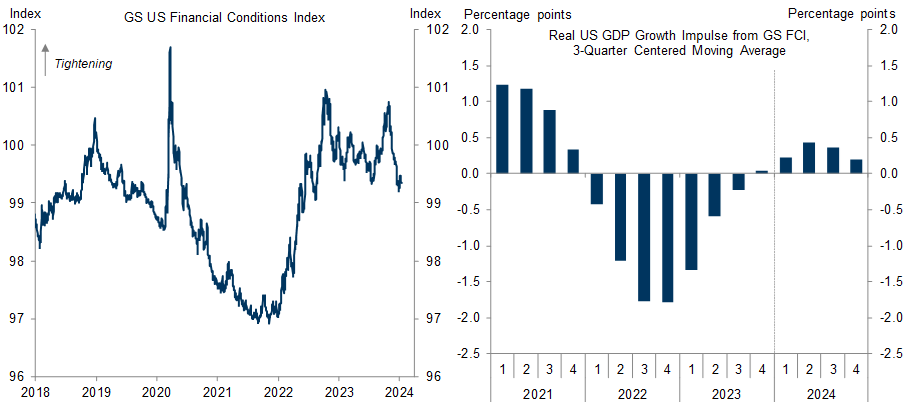

Risk 9: Something finally “breaking” due to higher interest rates is unlikely at this point because the peak growth hit from higher rates and tighter financial conditions is well behind us. Moreover, with inflation lower, the FOMC is at liberty to cut the funds rate more aggressively if necessary.

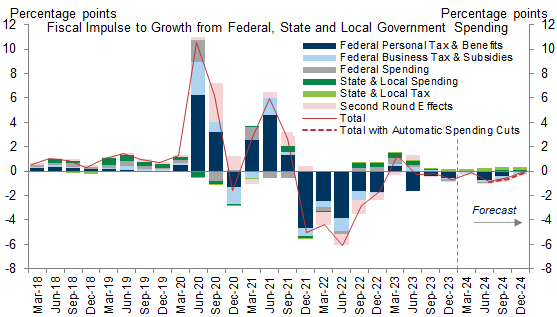

Risk 10: Fading fiscal support is less real than it appears—the federal deficit widened last year for reasons that were not very stimulative, and the fiscal impulse to GDP is likely to remain roughly steady this year, with a bit of downside risk from potential automatic spending cuts.

10 Growth Risks for 2024 and Why We Worry Less

Exhibit 1: We Are Well Above Consensus on 2024 GDP Growth and Well Below on Recession Risk

Risk 1: A consumer slowdown if unsustainable spending ends, the saving rate rises from a low level, or households run out of excess savings

Exhibit 2: We See Few Remaining Signs of Unsustainable Spending, Either on Services for Which There Was Pent-up Pandemic Demand or by Low-Income Families That Benefitted from Pandemic Stimulus

Exhibit 3: With Household Wealth Near an All-Time High, It Is Unsurprising That the Saving Rate Is Low

Risk 2: Rising consumer delinquency and default rates

Exhibit 4: Delinquency and Default Rates Have Risen, Though the Increase Is Largely a Normalization from Very Low Rates Early in the Pandemic When Income Was Elevated and Spending Needs Were Low

Exhibit 5: Factors Other Than Household Financial Weakness, Such as Higher Interest Rates or Riskier Lending, Also Account for Some of the Increase in Consumer Delinquency and Default Rates

Risk 3: A sharper deterioration in the labor market

Exhibit 6: Labor Market Tightness Appears to Be Stabilizing After a Successful Reversal of Overheating

Exhibit 7: Despite Scattered Signs of Weakness in Some Labor Market Indicators, Our Composite Job Growth Tracker Is Running at Double the Breakeven Rate Needed to Stabilize the Unemployment Rate

Risk 4: The narrow breadth of job growth

Exhibit 8: Job Growth Has Been Dominated by a Few Industries Recently, Raising Concerns About Excessive Cooling of Labor Demand or a Jobs-Workers Mismatch Problem

Exhibit 9: Job Openings Are High in Nearly Every Industry, and Unemployed Workers Have Found Jobs at an Elevated Rate

Risk 5: Rising corporate bankruptcies

Exhibit 10: Commercial Bankruptcies Haver Risen but Remain Below Pre-Pandemic Levels

Exhibit 11: Businesses Are on Solid Financial Footing

Risk 6: The corporate debt maturity wall

Exhibit 12: Business Interest Expense Will Increase in Coming Years as Companies Refinance at Higher Rates, But We Estimate That This Will Generate Only a Modest Drag on Capex and Hiring

Risk 7: Commercial real estate

Exhibit 13: Stress in the Commercial Real Estate Sector Has Been Limited to Offices, Which Make Up a Small Share of Bank Loans and Economic Activity

Risk 8: A bank credit crunch

Exhibit 14: Nonbanks Cut Back on Lending By Only Half As Much as Banks, Which Helps to Explain Why Small Businesses Have Not Reported a Lack of Access to Credit Despite Tighter Bank Lending Standards

Risk 9: Something finally “breaking” under higher interest rates if the Fed cuts too late

Exhibit 15: Our Estimate of the Impulse to GDP Growth from Changes in Financial Conditions Turns Modestly Positive in 2024

Risk 10: Fading fiscal support after a large widening of the federal deficit in 2023

Exhibit 16: We Estimate That the Fiscal Impulse to GDP Growth Was Modestly Negative in 2023, Despite the Large Increase in the Deficit, and Should Remain Roughly Steady in 2024

David Mericle

Manuel Abecasis

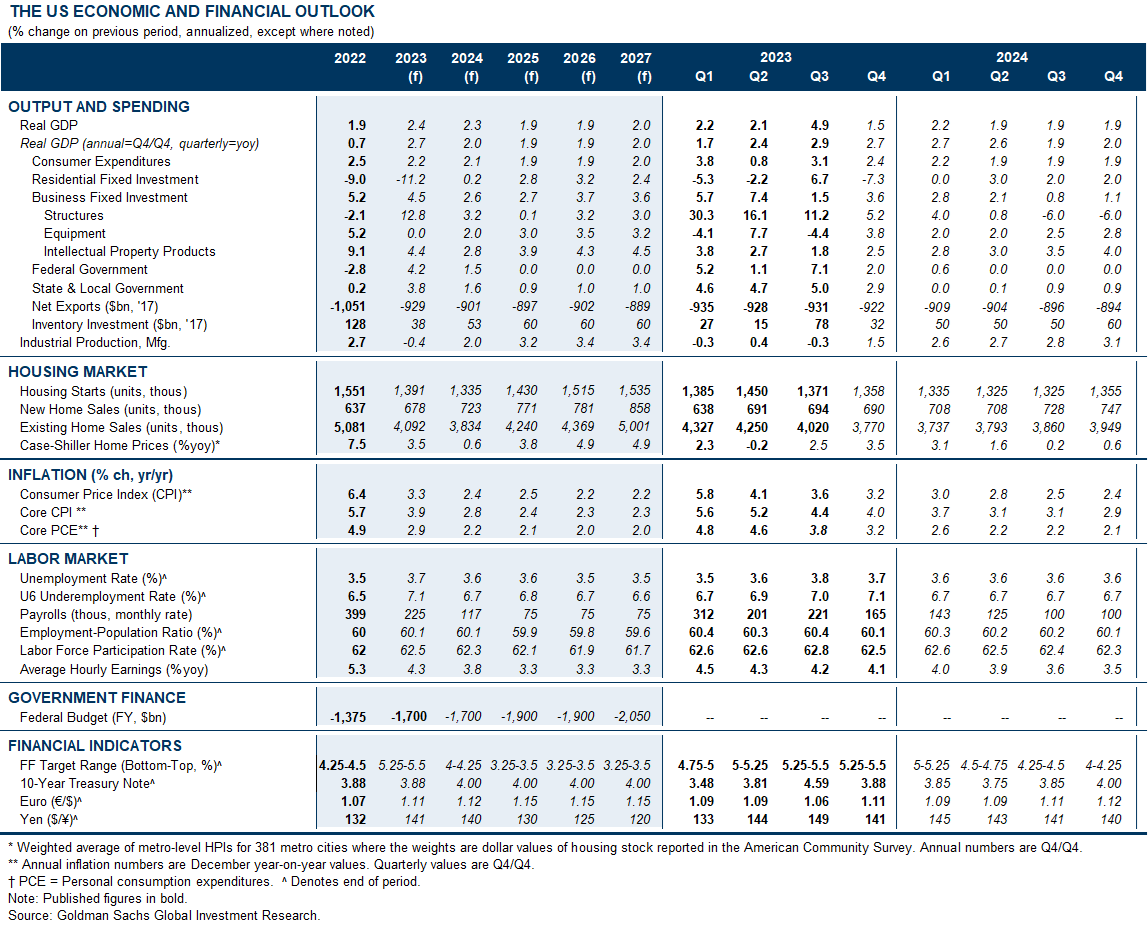

The US Economic and Financial Outlook

Investors should consider this report as only a single factor in making their investment decision. For Reg AC certification and other important disclosures, see the Disclosure Appendix, or go to www.gs.com/research/hedge.html.