We are entering a more benign part of the cycle with a continuation of economic growth alongside lower policy rates – a combination that has historically been positive for equities.

Longer-term rates are unlikely to fall given a rebuild of term premia and higher government deficits. This, together with high US equity valuations, moderates the upside in equities at the index level.

This means that alpha should become a more important driver of returns with a broadening opportunity set within and across equity markets.

There is a growing symbiotic relationship between the potential for the Technology sector and growth in some parts of the ‘old economy’ as the needs for capex rollout and electrification increase.

The prospects for equity returns are no longer a function of whether the sector is classified as Growth or Value; it can be a bit of both.

We look for opportunities to improve risk-adjusted returns through more regional diversification. We expect broadening market participation with Mid caps in the US, ETCs (ex Tech compounders) and selective Value compounders.

Where are we headed?

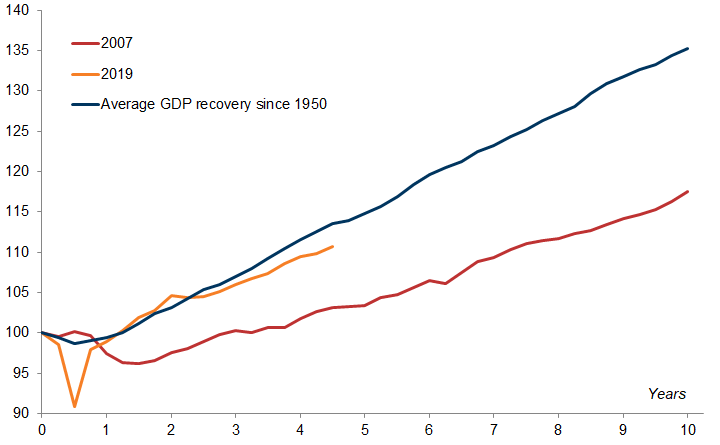

Exhibit 1: This cycle is evolving in a more ‘typical’ way relative to the post fiscal crisis cycle

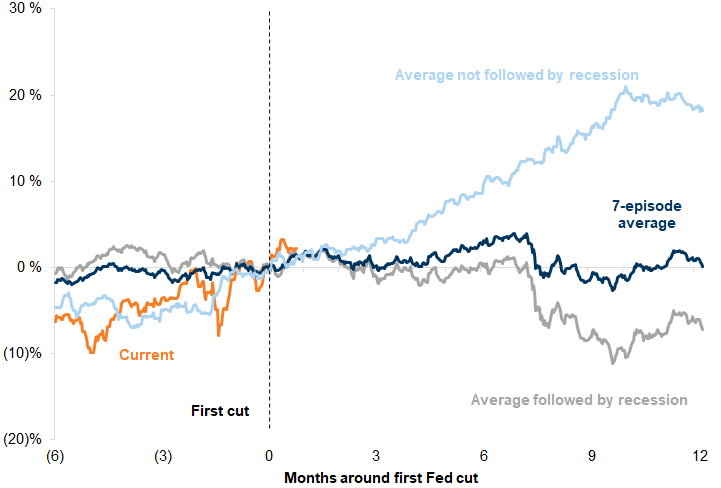

Exhibit 2: A combination of continued economic growth with a rate-cutting cycle tends to be positive for global equities

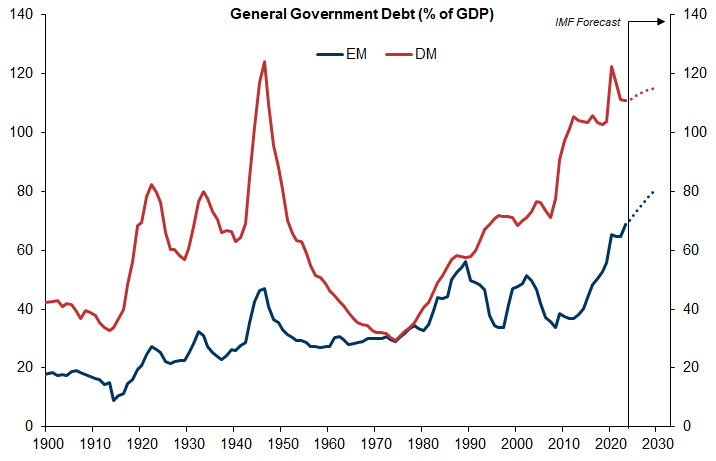

Exhibit 3: One of the structural dynamics at play is that government debt levels are high and often rising

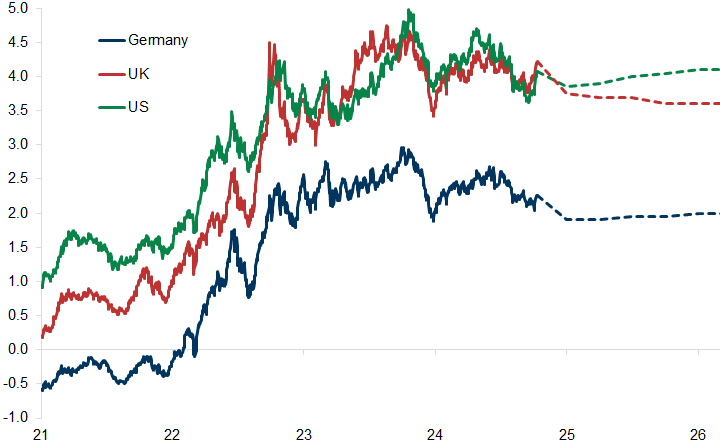

Exhibit 4: Longer-term interest rates are unlikely to come down

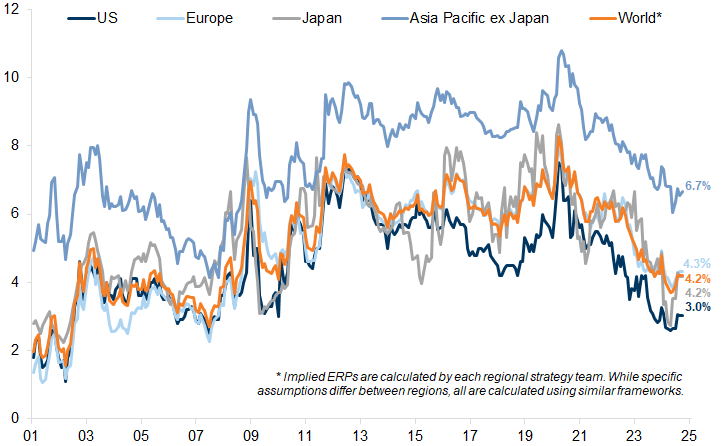

Exhibit 5: Equity Risk Premium has fallen back to the low levels seen in the early part of this century

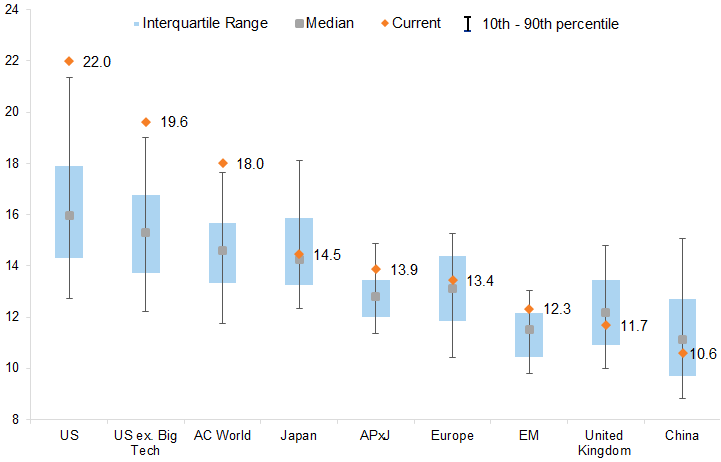

Exhibit 6: At the same time, equity index valuations in the US market are at the top of their longer-term range on other valuation metrics

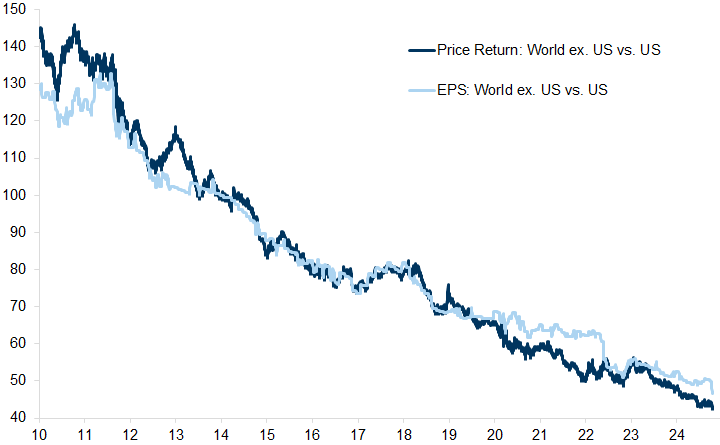

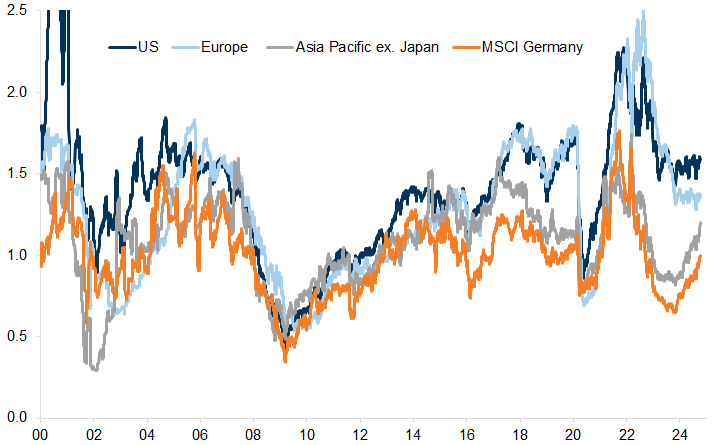

Exhibit 7: While the US has consistently outperformed, this has been broadly explained by relative profit growth

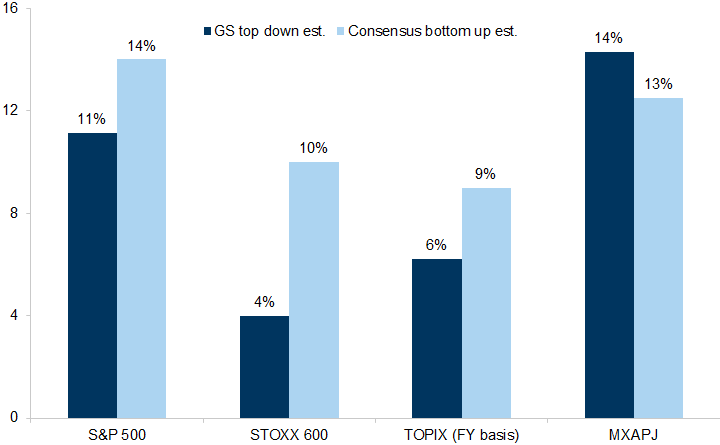

Exhibit 8: Only Europe continues to lag in terms of profit growth prospects

Exhibit 9: Big discounts in Europe might suggest hidden value in some places

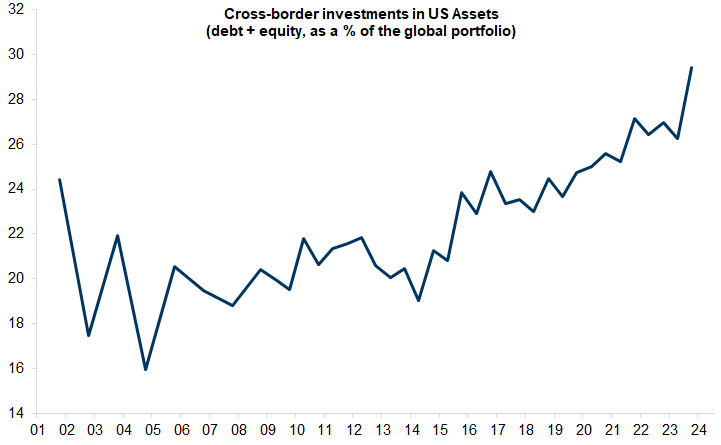

Exhibit 10: Portfolio investments held in US assets (equity and debt securities) are at a peak

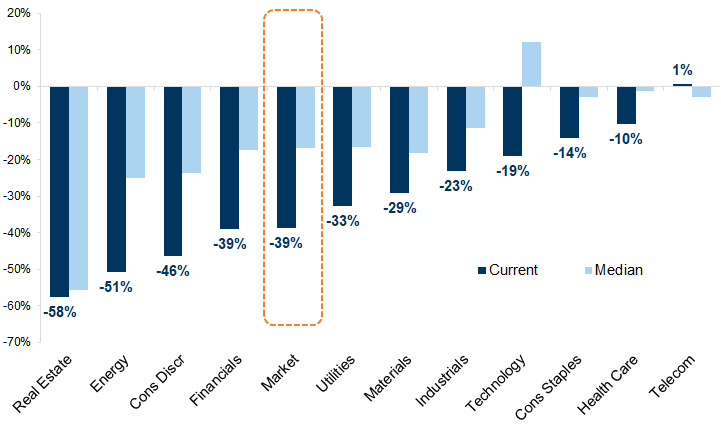

Exhibit 11: On a sector comparison, stocks in Europe trade on much bigger discounts than they have typically done in the past

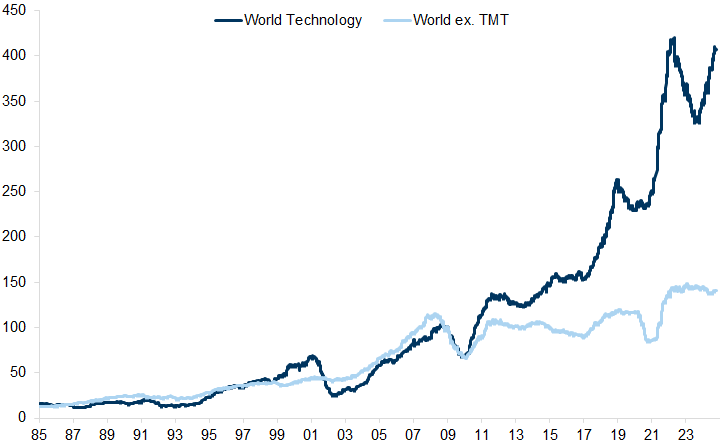

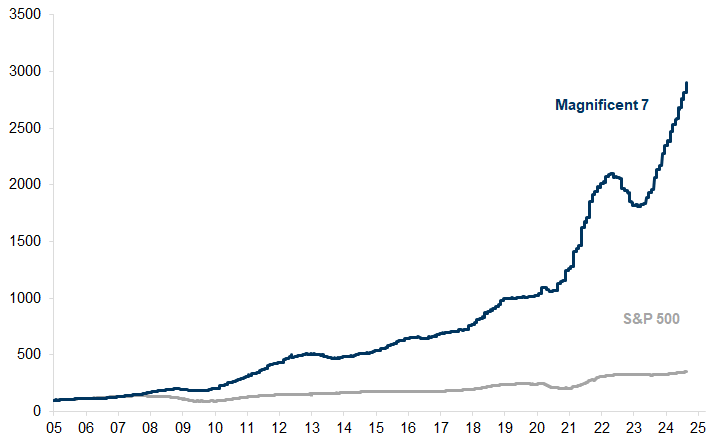

Exhibit 12: Just as the US equity market outperformance has reflected stronger fundamentals, so too has the Technology sector

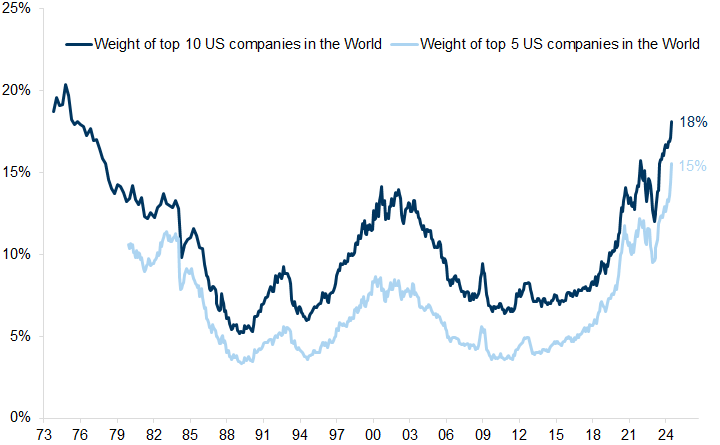

Exhibit 13: In the US the biggest 10 companies account for around 18% of the value of the global equity market

Exhibit 14: This increased concentration has reflected extraordinary profit growth rather than speculative exuberance

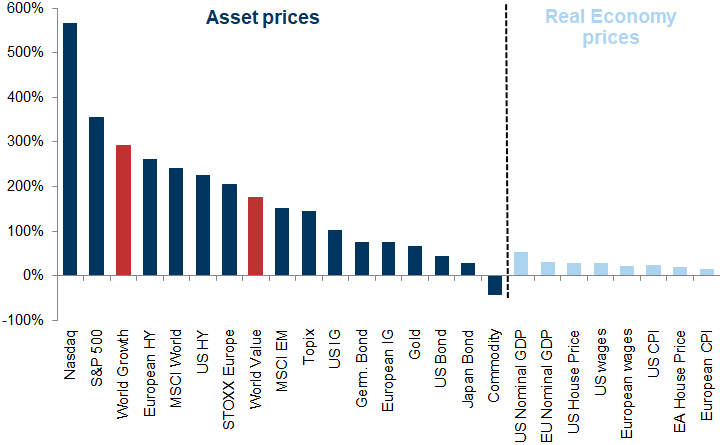

Exhibit 15: In the post financial crisis decade, up until the start of the pandemic, financial assets sharply outperformed real assets

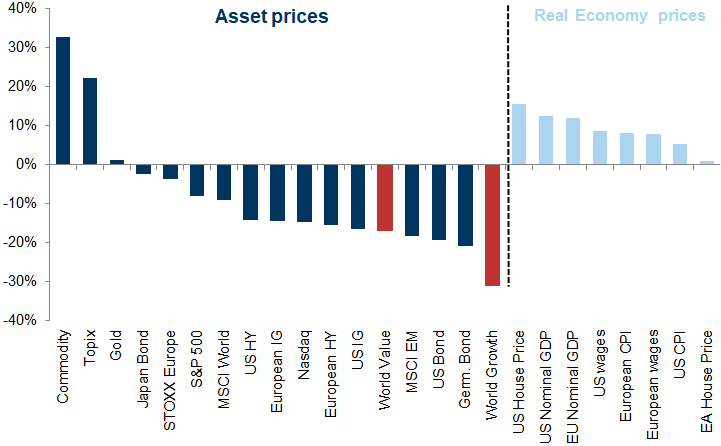

Exhibit 16: The pattern reversed in 2022 as global inflation and rising rates upended the relationships

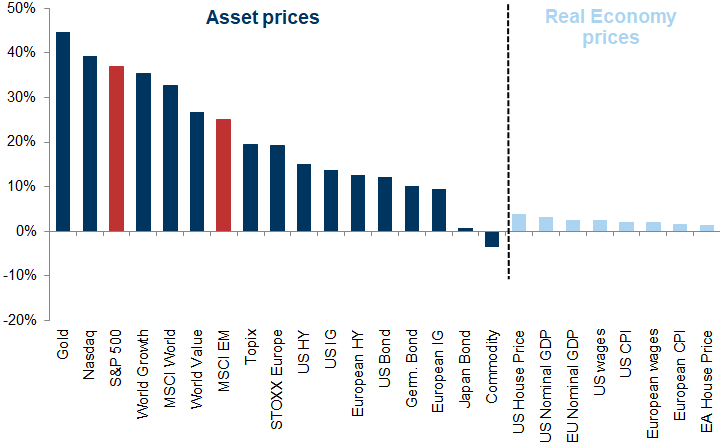

Exhibit 17: This year, the 'winners' have been a more eclectic mix

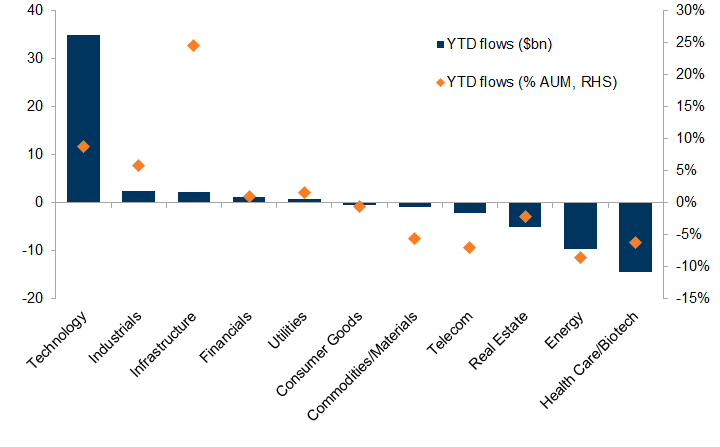

Exhibit 18: The largest inflows have been into US Tech funds with large outflows from Healthcare and Energy

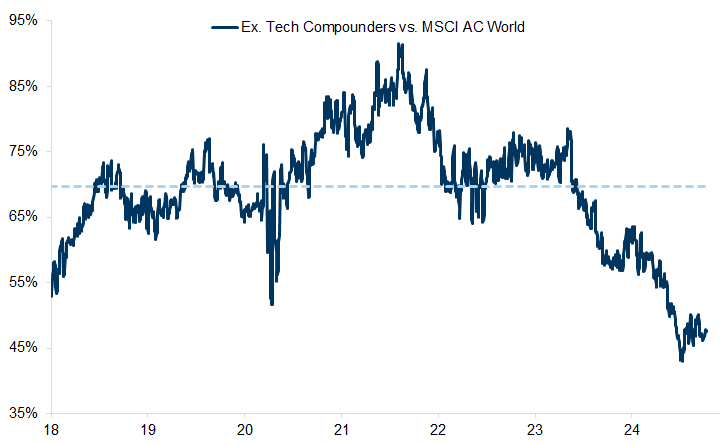

Exhibit 19: Our ETCs list trades at the lowest premium to the world stock market since 2019

Investors should consider this report as only a single factor in making their investment decision. For Reg AC certification and other important disclosures, see the Disclosure Appendix, or go to www.gs.com/research/hedge.html.